Issue 19 Contents

Spotlight—Intangible resources and financial reporting—an evolving debate

The information that companies provide about intangible resources—or intangibles reporting—has been a hot topic for many years. The subject has long interested people directly involved in financial reporting and analysis, such as investors, accountants and corporates; the increasing significance of intangibles in many modern economies has also prompted a growing and broader interest in intangibles reporting among policymakers and academics. Given this trend, IFRS Foundation Staff discussed intangibles reporting at the IFRS Foundation Conference, held in London in June 2019, with a panel comprised of investors, a regulator, an academic and a member of the International Accounting Standards Board (Board).

The complexities of intangibles reporting are beyond the scope of this brief article. Instead, our modest aim is to examine some concepts discussed in the workshop, and to share some notable comments and insights by the panellists.

How do we define intangibles?

Broadly, ‘intangibles’ lack physical substance and help a company to create value, whether or not they are secured by legal means, and whether or not they meet the definition of assets in the current accounting framework. Intangible assets as defined in IAS 38 Intangible Assets form a subset of the broader set of intangible resources (or, more simply, ‘intangibles’).

Investors generally want to know about all items that may potentially produce future cash flows and growth. In other words, investors may want to use both information about intangible assets that must be formally recognised and measured in a company’s financial statements and information about unrecognised intangibles.

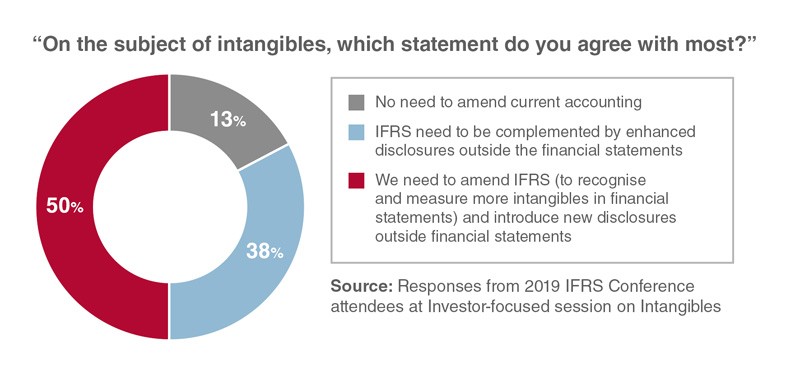

The rising role of intangibles

Overwhelming evidence suggests that companies today derive significantly greater value from intangibles than was the case, say, 20–30 years ago. We asked the workshop’s participants whether the rising importance of intangibles suggested that the Board should amend any IFRS Standards. As shown in the following chart, an overwhelming majority of workshop participants indicated that some change would be beneficial, while about half said that IFRS Standards should be amended to recognise and measure more intangibles, as well as to introduce new disclosure requirements outside a company’s financial statements for intangibles.

Defining and measuring intangibles

Participants discussed the recognition and measurement of intangibles in the current accounting framework. We compared the narrow definition and system of classification for intangibles in IFRS Standards to other more wide-ranging approaches. The preparer on the panel argued that the Standards provide insufficient clarity on how different intangibles may be classified, particularly in relation to business combinations—a view echoed by many conference participants.

In our discussion of these intangibles:

- a majority, 75%, of participants reported that measuring human capital would be of limited use to investors; and

- just 45% of participants said that knowledge should not be reported in a company’s financial statements.

The intangibles information gap

Panellists also discussed the usefulness of information that investors receive on intangibles in a company’s financial statements and in other parts of its annual reporting package. Many global economic policymakers, regulators and academics have expressed concerns about the perceived information gap on intangibles. For instance, Gu and Lev (2016) view the current accounting treatment of intangibles to be linked to the declining relevance of earnings to company value. Others assert that the failure to recognise many internally generated intangibles in a company’s financial statements has adverse consequences for investment analysis and governance. Evidence suggests that earnings have become less important in explaining share-price movements: cash flows have taken their place, in the opinion of Barth and others. To forecast cash flows more accurately, however, investors may still require better information on intangibles. Indeed, a majority of participants (54%) agreed that to close the perceived gap on information about intangibles, companies should provide more information outside of the financial statements on ‘value drivers’ and their associated intangibles; on the management of and strategy behind intangibles; and on the value of intangibles.

Using intangibles in investment analysis

Our workshop covered some analytical approaches for intangibles used in investment analysis. We discussed an approach proposed by Damodaran that capitalises certain expenses and amortises the resulting assets using reasonable amortisable life assumptions. These are expenses such as R&D of pharma companies, advertising of consumer goods companies, and training of consulting companies. Using this approach is believed to produce more consistency between the inputs in discounted cash flow models (such as growth rates, and reinvestment rates and return ratios).

We also discussed a qualitative approach that incorporates information on intangibles into a relative valuation framework. The fundamental idea here is that investors can develop scorecards to help them assess the performance of a company’s intangibles. A company achieving a higher score in such a framework may warrant being valued using a higher price multiple when its intrinsic value is estimated.

An investor on the panel said that many investors already use sophisticated approaches to incorporate information on intangibles into their analysis and valuation of companies.

A majority of workshop participants—63%— said investors can best analyse intangibles using capitalisation techniques and non-financial information on the risks and return potential of intangibles.

Inconsistency in accounting for intangible assets

Participants also discussed inconsistent accounting treatment for internally generated intangibles as opposed to those identified in a business combination. Investors have repeatedly raised this issue in recent years. The investors on the panel found this inconsistency unhelpful, because it diminishes comparability between companies that acquire companies with those that grow organically. However, the discussion did not attempt to explore, in-depth, the alternative approaches that could provide investors with more useful information. The preparer on the panel also criticised the inconsistency and thought that the need to identify acquired intangibles (as required by IFRS 3 Business Combinations) was costly and largely unhelpful. Furthermore, 86% of the participants in the workshop agreed the Board should require more consistency in accounting for intangibles.

Narrative reporting on intangibles

In principle, investors and other stakeholders broadly accept that the perceived information gap on intangibles can be addressed in narrative reporting. The panel discussed, related reporting frameworks, including the work of national and international standard-setters. We provided evidence of limited adoption of the national frameworks on intangibles by listed companies.

Although many of the standard-setting initiatives—such as GRI and IIRC—focus on non-financial reporting, they make no specific mention of intangibles, nor is there evidence of coherent progress towards narrative reporting on them. Of the workshop participants, 65% agreed that an absence of harmony in current requirements was the greatest obstacle hindering progress towards the global adoption of intangibles reporting frameworks.

We highlighted the Board’s Management Commentary Practice Statement project, which will, in part look to develop guidance on narrative reporting on intangibles. In this regard, a majority—55%—of workshop participants said rather than to require specification, the Board should take a ‘principles driven’ approach to intangibles for narrative reporting.

Key performance indicators (KPIs) also featured in the workshop; investors report that KPIs are useful for analysing companies. The World Intellectual Capital has developed a framework emphasising innovation and value creation through explicit links to KPIs. We examined how different ‘value drivers’, such as customers, competitive position and employees, are linked to respective intangibles such as loyalty, market share and skills. For each of these value drivers, KPIs can be ascribed to track the performance of the associated intangibles—for example, the repeat customer ratio can be used to assess customer loyalty. Of workshop participants, 51% said the Board should allow market forces to determine the development of KPIs (compared to 49% who would prefer the Board to support the development of KPIs either at a high level or at a sectoral level).

Conclusion

Intangibles represent complex investments for which single measures of value are unlikely to provide all relevant information. Instead, a narrative discussion on ‘value drivers’ and associated KPIs could be a useful way for companies to communicate with investors. In relation to intangibles, the Board is currently addressing the information needs of investors via its Management Commentary project. We will welcome your feedback on the project’s exposure draft which the Board expects to publish in the first half of 2020. In addition, we will also welcome investors’ response to the Board’s 2020 Agenda Consultation, which, in the next five years, will help determine the Board’s areas of focus in relation to financial reporting. We will be writing more about the Agenda Consultation in the coming months; if you’d like the Board to address intangibles in more detail, please watch this space.

In profile—Jacques De Greling, Scope Ratings

IASB Investor team: You recently switched from being an equity analyst to specialising as a credit analyst. How has this affected your approach to financial analysis and views on financial reporting?

There is a balance to switching from equity analyst to credit analyst. Most of the mechanics of analysis are unchanged (for example, assessing profitability), but the focus of the analysis is different. As an equity analyst, the focus and perspective are oriented towards assessing potential upside, while on the credit side it is oriented towards the downside. This is a significant difference.

The perspective on timing or time horizon is also different. For example, in an equity story, 80% of the valuation (like in a discounted cash flow analysis) might come from the terminal value, which relies on a long-term view. On the credit side, the time horizon tends to be shorter since you are assessing the prospects for debt repayment.

There are also differences in focus of attention when reviewing company disclosures. When I was an equity analyst, there were some disclosures that I almost ignored, but which I must confess I now review in more depth on the credit side—for example, disclosures about operating lease payments. This work has allowed me to discover new insights in the disclosures that I was not previously using, which is an exciting learning curve. When I joined Scope Ratings, this learning opportunity was part of what excited me about joining the European alternative rating agency in what is a fairly concentrated industry.

IASB Investor team: Several new IFRS Standards have been introduced in recent years (for example, IFRS 15 Revenue from Contracts with Customers). What has been your experience with adapting to the changes?

I see the adaptation process for an analyst as a ‘business as usual’ issue, since, in my experience, dealing with change has historically been a common feature of the job.

For IFRS 15, a significant amount of interest on my part stems from my years of telecoms sector coverage. I recall being invited to discuss IFRS 15 with the CFOs of some telecom companies before implementation, and there was very little information for me to use since they had produced almost no information six months prior to the implementation date. It was frustrating not to have any information about the real effects of the transition.

Now that we have had the switch, my first impression of IFRS 15 for the telecoms sector is that it has proven to be a positive change. The former approach was not realistic, and the popular example of mobile handset sales recording zero revenue illustrates this. There was a need for a better way to think about revenue. But, as in the case of all change, it took some time to see the real benefits.

Broadly speaking, there has been improvement in disclosures with better detail or disaggregation of revenue. However, some telecoms companies now present revenue from ‘converged offers’ (bundles of fixed line, mobile and broadband), which appears to go against the spirit of improving disaggregation. Unfortunately, there also are cases where the boilerplate approach doesn’t deliver value at all.

IASB Investor Team: In your view, what are the areas of financial reporting in which standard-setting can help resolve investors’ most significant concerns?

I see three key areas where I believe the IASB’s work can produce important benefits.

Firstly, the project on Primary Financial Statements, which began over 15 years ago under the name of ‘performance reporting’, is important to me. The effort to develop requirements that give investors better sub-totals, which you can compare from one company to another, and improve disaggregation in the P&L are the key objectives on which the IASB will be judged when we finally see the project’s outcome.

I am encouraged by the project’s proposals to address these two areas (sub-totals and disaggregation), though I must admit I am reluctant about the approach of presenting results from equity-consolidated activities (for example, joint ventures and associates) within two separate sub-totals of performance. The relevance of such an approach concerns me since the sub-totals are on a pre-tax basis while the equity consolidated results are after-tax. Also, I question the workability of this solution—in particular, I fear that companies may choose to be opportunistic by presenting profitable equity-consolidated activities in the ‘core activities’ section of the P&L while presenting the loss-making equity consolidated activities in the ‘non-core’ activities section.

One area of the Primary Financial Statements project that I believe the Board should consider, before progressing to the project’s Exposure Draft, relates to the requirements around the ‘by nature’ presentation format in the income statement. This presentation format is the one that is favoured by users: first, because this approach to P&L presentation can produce better disaggregation, more independent from the company than the by function presentation, which derives from internal cost allocation; second, it makes the full P&L consistent with how the items are presented in the other comprehensive income (OCI)—where the ‘by nature’ approach is always used. Another key point, which is very important for users, is that having a ‘by nature presentation’ best enables an analyst to efficiently use the cash flow statement with the indirect method since it allows you to easily compare the information provided by the two statements. Having a ‘by function’ presentation (for P&L) does not allow you to make the same links with the information in the cash flow statement, a major source of frustration for investors.

The second most important Standard for investors is the one on segment reporting (that is, IFRS 8 Operating Segments). I truly believe that the management approach used in this Standard is completely at the opposite end of what adopting IFRS Standards intended to provide—which is comparability. IFRS Standards should deliver comparability, rather than being individual financial reporting standards. If you allow management to prepare financial reporting of performance that is not understandable by those outside of the company, it could be completely misleading or completely useless. Having a basic reconciliation between a management's measure of profit at segment level with a GAAP measure of profit is key from the user's perspective.

One aspect of segment reporting and its importance to users that I would like to stress is that this information helps users understand a business, which is different from reviewing other aspects of the financial statements where the information helps you achieve an understanding of the accounting. Investors invest in businesses not in accounts, so to make investment decisions it is vital to have segment reporting that properly provides us with an understanding of the businesses.

The third area relates to IFRS 3 Business Combinations, where we have endured problems with goodwill impairment for many years. I think there are two major flaws that help explain why impairment does not work in the current Standard. The first flaw emanates from the fact that goodwill is difficult to allocate in terms of expected life, which led to the decision to stop amortising it. But you could use the same reasoning in thinking about the useful life of a piece of machinery or a plant being built. It is not because it is difficult to amortise, in terms of timing, that you should stop amortisation as a financial reporting practice.

The second flaw emanates from the inconsistency between what the test is trying to measure or assess, that the acquired goodwill is not overvalued, with how the test is performed in a cash generating unit, where there is a combination of the acquired goodwill with the internally generated (organic) goodwill that has not been recognised, and the goodwill created since the business combination. EFRAG and the IASB have attempted to resolve this headroom problem, and others, in goodwill, but I don’t believe these solutions will work. After many years of attempting to resolve it, my simple conclusion is that returning to goodwill amortisation would be the best way to fix a problem with something that is reasonable and workable. From my perspective, goodwill amortisation allows you to present a cost in P&L that was in fact a cash cost, this is an issue on which we should have consistency between the P&L and cash flow statement.

Lastly, I would conclude from my experience in the European telecoms sector that the goodwill impairment test story had no credibility in the eyes of investors, who knew that the test was completely gamed to deliver the results (cash flow projections) that management wanted. This reminds me of one of my favourite expressions in French, which asks what does ‘DCF’ stand for and the response is ‘dis moi combien il te faut’ (tell me how much you need) instead of ‘discounted cash flow’.

IASB Investor Team: The IASB hears from investor groups and associations around the world. Can you share with us your experiences with the Société Française des Analystes Financiers (SFAF) and European Federation of Financial Analysts Societies (EFFAS) on advocating for improving financial reporting quality and transparency?

I’ve had a very positive experience with investor groups advocating for improvements in financial reporting over the years. I joined the SFAF’s accounting commission in 1992 and have served as its co-chair for 15 years alongside Bertrand Allard, a member of the IASB’s Capital Markets Advisory Committee (CMAC). It has been very enriching for us to continue the commission’s 60-year tradition of holding monthly meetings to discuss company accounting practices, standard-setting proposals and even academic research. I have also enjoyed participating on a similar commission at EFFAS (since 2000), where I have benefited from the international mix of members explaining accounting practices across different countries.

I think we have succeeded in reflecting the views of users and representing them because of the input we obtain from our members, who mostly work in the investment community. A significant part of my involvement in these groups has been to debate with analysts the information they use on the job every day, which has helped make me very comfortable in discussing accounting standards and in pushing for certain changes. Our input into the standard-setting process is not only conceptually driven but also driven by practicality—I like concepts that work. Nevertheless, like many other groups representing users, such as SAAJ, CRUF or the CFA Institute, we sometimes miss out. First, we have a limited voice or share of voice in the standard-setting process. For example, among the hundreds of comment letters that the IASB may receive on any consultation only a few typically come from investors.

IASB Investor team: In recent years, we have seen a few developments on the topic of non-GAAP or alternative performance measures (APMs). What is your perspective on the trends and developments in this area?

One of my fundamental views, which I shared a few years ago at an IASB conference to discuss APMs, is that the weakness in IAS 1 Presentation of Financial Statements has been one of the sources for the proliferation of APMs over the years. Because IAS 1 is not prescriptive enough, in the end companies have too much flexibility to present what they want.

I also believe another driver for the proliferation of APMs was the decision by standard-setters to remove the income statement’s section about exceptional or non-recurring items and instead present these items in the operating section. I agree this was more reasonable because there were abuses in what was reported as ‘non-recurring’. One of the consequences of the change is that companies could disclose explanations about abnormal or non-recurring items, which is fine, but what we find in practice is that almost 85% of the APMs are higher than the nearest GAAP measure. So, perhaps we have ended up in a situation with too much self-promotion in the APMs.

This has become too much of a ‘game’, which explains why ESMA decided to require proper disclosures on APMs including reconciliations and explanations about the relevance of the APMs. We at EFFAS took part in ESMA’s consultation and working group, and believe that it has succeeded in improving transparency on APMs and helping to fix one of the consequences of the existing IFRS Standard.

I would caution that when new accounting standards are introduced, investors should be mindful of the effects on APMs. For some of the European telecoms groups, the application of IFRS 16 Leases has led them to introduce new KPIs (APMs) that adjust the figures to present what management wants. Not all of the companies have decided which KPIs to use or adjust, while others chose to stick to the previous indicators, so it is too early to determine which will be retained.

Looking forward, I hope that the Primary Financial Statements project will solve some of the issues that remain, in particular in the case of IFRS 8 which permits companies to include non-GAAP measures without reconciliation in the segment results.

IASB Investor team: Looking to the future—how do you see the work of fundamental research and financial analysis evolving in the light of trends around technology and data usage?

If the question relates to the application of big data and artificial intelligence then I am a bit reluctant to speculate on what may happen but speaking from years of experience doing financial modelling and company valuations, I would emphasise that understanding the importance of making reasonable and consistent assumptions is more important than simply the data entered into a spreadsheet. Because of this, I am not sure that artificial intelligence will completely revolutionise financial analysis though I can see how it could help evolve some of the scoring aspects of financial analysis.

It would be like arguing 30 years ago that the introduction of Excel software would lead to everyone being able to do perfect financial modelling. It was a convenient tool but for investors the key challenge remains the same: making reasonable and consistent assumptions. My experience has taught me that to make sound investment decisions supported by research, it is more important to understand a business and how its performance relates to the reported figures than it is to use Excel to manipulate the figures and make potentially misleading correlations.