Thank you so much, Neera, for that very kind introduction. I've long admired all that you and everyone here at the Center for American Progress do to promote a progressive economic agenda. And I share your commitment to making sure our markets are safe and efficient—and fair for all Americans. So it's a real honor to be with you here today.[1]

I also want to thank my friend Andy Green, who in addition to being Managing Director of Economic Policy here at CAP, has been a critical source of wisdom for me since my swearing in at the Commission back in January.

Before I begin, let me start with the standard disclaimer that the views I'm about to express are my own and do not reflect the views of the Commission, my fellow Commissioners, or the SEC's Staff. And let me add my own standard caveat, which is that I fully expect someday to convince my colleagues that I am, as usual, completely correct in everything I say and do.

Today, I'd like to share a few thoughts about corporate stock buybacks—and some research produced by my staff that raises significant new questions about this activity. As Neera mentioned, I'm a recovering researcher. Before I was appointed to the SEC, I was a law professor who spent most of my time thinking about how to give corporate managers incentives to create sustainable long-term value. I'd often ask my students: are we making sure that executive pay gives managers reason to invest in the long-term development of their workforce and their communities? Or are we paying executives to pursue short-term stock-price spikes rather than long-term growth?

Little did I know that, so soon into my tenure, I'd have a sobering case study to put these questions to the test. That's because the Trump tax bill, promising to bring overseas corporate cash home, became law last December.

Now, we all know what happened the last time a Republican-controlled government pushed through a corporate tax holiday in 2004. As that bill's sponsors hoped, American companies repatriated billions of dollars of overseas cash.[2] But corporations didn't invest most of that money in innovation. They didn't invest it in retraining their workforce or raising wages. Instead, executives largely used the influx of fresh funds for massive stock buybacks.[3]

So when I first took this job, I worried that 14 years later history would repeat itself, and the tax bill would cause managers to focus on financial engineering rather than long-term value creation. Sure enough, in the first quarter of 2018 alone American corporations bought back a record $178 billion in stock.[4] On too many occasions, companies doing buybacks have failed to make the long-term investments in innovation or their workforce that our economy so badly needs.[5] And, because we at the SEC have not reviewed our rules governing stock buybacks in over a decade, I worry whether these rules can protect investors, workers, and communities from the torrent of corporate trading dominating today's markets.[6]

Even more disturbing, there is clear evidence that a substantial number of corporate executives today use buybacks as a chance to cash out the shares of the company they received as executive pay.[7] We give stock to corporate managers to convince them to create the kind of long-term value that benefits American companies and the workers and communities they serve. Instead, what we are seeing is that executives are using buybacks as a chance to cash out their compensation at investor expense.

Executives often claim that a buyback is the right long-term strategy for the company, and they're not always wrong. But if that's the case, they should want to hold the stock over the long run, not cash it out once a buyback is announced. If corporate managers believe that buybacks are best for the company, its workers, and its community, they should put their money where their mouth is. That's why I'm here today to call on my colleagues at the Commission to update our rules to limit executives from using stock buybacks to cash out from America's companies.

And I am also calling for an open comment period to reexamine our rules in this area to make sure they protect employees, investors, and communities given today's unprecedented volume of buybacks.

Stock Buybacks and Executive Pay

Basic corporate-finance theory tells us that, when a company announces a stock buyback, it is announcing to the world that it thinks the stock is cheap.[8] That announcement, and the firm's open-market purchasing activity, often causes the company's stock price to jump, so the SEC has adopted special rules to govern buybacks.

Those rules, first adopted in 1982, provide companies with a safe harbor[9] from securities-fraud liability if the pricing and timing of buyback-related repurchases meet certain conditions.[10] After experience proved that buybacks could be used to take advantage of less-informed investors,[11] the SEC updated its rules in 2003, though researchers noted that several gaps remained.[12]

In the meantime, the use of stock-based pay at American public companies has exploded.[13] Although these pay programs present many challenges, the one that I've spent much of my career thinking about is how to make sure that corporate management has skin in the game—that is, how to keep top executives from cashing out stock they receive as compensation.[14]

You see, the theory behind paying executives in stock is to give them incentives to create long-term, sustainable value.[15] Because executives who receive shares rather than cash demand higher levels of pay, the use of stock-based compensation has led to eye-opening pay packages for top executives. In the trade, investors—and the economy as a whole—tie executives' fortunes to the growth of the company.

But that only works when executives are required to hold the stock over the long term. Researchers have long worried that executives, who always prefer cash to stock, will try to sell rather than hold their shares, eliminating the incentives they were meant to produce.[16] So it's no surprise that, in the years leading up to the financial crisis, top executives at Bear Stearns and Lehman Brothers personally cashed out $2.4 billion in stock before the firms collapsed.[17] And it's no wonder that sophisticated investors have for decades strictly limited executives' freedom to cash out their shares.[18]

In the wake of the financial crisis, Congress realized the importance of keeping executives' skin in the game, so the Dodd-Frank Act included several provisions designed to give investors more information about whether and how managers cash out.[19] Unfortunately, as you all know too well, those rules have still not yet been completed, keeping investors in the dark about executives' incentives.

Nearly eight years since that landmark legislation, it is completely unacceptable that the SEC has still not promulgated these and other rules required by law. But it's not just that the regulations haven't been finalized. It's that the problem itself keeps getting worse. You see, the Trump tax bill has unleashed an unprecedented wave of buybacks, and I worry that lax SEC rules and corporate oversight are giving executives yet another chance to cash out at investor expense.

How Executives Use Buybacks to Cash out

That's why, when I was sworn in a few weeks after the Trump tax bill took effect, I asked my staff to take a look at how buybacks affect how much skin executives keep in the game. I was worried that lax corporate practices and SEC rules might lead to buybacks that give executives yet another chance to cash out at investor expense.

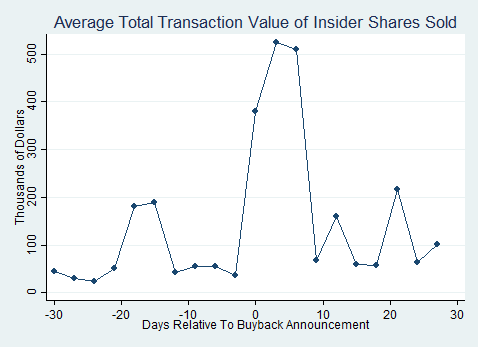

So we dove into the data, studying 385 buybacks over the last fifteen months.[20] We matched those buybacks by hand to information on executive stock sales available in SEC filings.[21] First, we found that a buyback announcement leads to a big jump in stock price: in the 30 days after the announcements we studied, firms enjoy abnormal returns of more than 2.5%.[22] That's unsurprising: when a public company in the United States announces that it thinks the stock is cheap, investors bid up its price.

What did surprise us, however, was how commonplace it is for executives to use buybacks as a chance to cash out. In half of the buybacks we studied, at least one executive sold shares in the month following the buyback announcement. In fact, twice as many companies have insiders selling in the eight days after a buyback announcement as sell on an ordinary day.[23] So right after the company tells the market that the stock is cheap, executives overwhelmingly decide to sell.[24]

And, in the process, executives take a lot of cash off the table. On average, in the days before a buyback announcement, executives trade in relatively small amounts—less than $100,000 worth. But during the eight days following a buyback announcement, executives on average sell more than $500,000 worth of stock each day—a fivefold increase. Thus, executives personally capture the benefit of the short-term stock-price pop created by the buyback announcement:

Now, let's be clear: this trading is not necessarily illegal. But it is troubling, because it is yet another piece of evidence that executives are spending more time on short-term stock trading than long-term value creation. It's one thing for a corporate board and top executives to decide that a buyback is the right thing to do with the company's capital. It's another for them to use that decision as an opportunity to pocket some cash at the expense of the shareholders they have a duty to protect, the workers they employ, or the communities they serve.

More importantly, policymakers, advocates, investors and corporate boards have spent decades, and billions of dollars of shareholder money, trying to tie executive pay to long-term corporate performance. But the evidence shows that buybacks give executives an opportunity to take significant cash off the table, breaking the pay-performance link. SEC rules do nothing to discourage executives from using buybacks in this way. It's time for that to change.

The Path Forward

There are two steps we can and should take right away to address the practice of executives using buybacks as a chance to sell their shares. First, as I mentioned earlier, the SEC last revised its rules governing buybacks in 2003. Those rules give companies a so-called "safe harbor" from liability when pursuing buybacks. But there are no limits on boards and executives using the buyback—and the safe harbor—as an opportunity to cash out.

I cannot see why a safe harbor to the securities laws should subsidize this behavior. Instead, SEC rules should encourage executives to keep their skin in the game for the long term. That's why our rules should be updated, at a minimum, to deny the safe harbor to companies that choose to allow executives to cash out during a buyback.[25]

And that's why today I'm also calling for an open comment period to reexamine our rules in this area to make sure they protect American companies, employees, and investors given today's unprecedented volume of buybacks.[26]

Second, corporate boards and their counsel should pay closer attention to the implications of a buyback for the link between pay and performance. In particular, the company's compensation committee should be required to carefully review the degree to which the buyback will be used as a chance for executives to turn long-term performance incentives into cash. If executives will use the buyback to cash out, the committee should be required to approve that decision and disclose to investors the reasons why it is in the company's long-term interests. It is hard to see why a company's buyback announcement shouldn't be accompanied by this kind of disclosure.[27]

Executives who can't sell their holdings in the short term—but instead have to create real value over time—have far fewer incentives to manage to quarterly earnings and pursue the kind of short-term thinking that dominates our economy today. The esteemed experts on our next panel will, I'm sure, offer broader policy proposals that can help us address those problems. But at the SEC, it's time for our rules to require corporate managers who say they want to manage for the long term to put their money where their mouth is. At the very least, our rules should stop giving executives incentives to use buybacks to cash out.

* * * *

The increasingly rapid cycling of capital at American public companies has had real costs for American workers and families. We need our corporations to create the kind of long-term, sustainable value that leads to the stable jobs American families count on to build their futures. Corporate boards and executives should be working on those investments, not cashing in on short-term financial engineering.

Each day when I arrive at work, I'm reminded that the SEC's mission is to protect investors, ensure a level playing field in our financial markets, and encourage capital formation. Updating our rules to reflect the effects of buybacks on executives' incentives to create long-term value would serve all three of those goals.

Investors deserve to know when corporate insiders who are claiming to be creating value with a buyback are, in fact, cashing in.[28] A level playing field requires that shareholders selling into a buyback know what managers are doing with their own money. And investors who feel assured that buybacks won't be used as a chance for insiders to cash in will be more willing to fund the kinds of long-term investments our economy needs.

All of you here at CAP have provided essential leadership in developing policies that produce growth for all Americans—and favor long-term value creation over financial engineering. That's why I'm so proud to be here today. I'm very much looking forward to your questions. And I so look forward to working with you to ensure that the SEC's policies create the kinds of markets that American families need—and deserve.

[1] Commissioner, United States Securities and Exchange Commission. I am, as always, grateful to my SEC colleagues Bobby Bishop, Caroline Crenshaw, Marc Francis, Satyam Khanna, Prashant Yerramalli, and Jon Zytnick for their invaluable counsel. Professor Jesse Fried of the Harvard Law School also provided insights that significantly deepened my thinking about these matters. The views expressed here are solely my own, and do not necessarily reflect those of the Staff or my colleagues on the Commission, though I hope someday they will.

[2] See American Jobs Creation Act, Pub. L. No. 108-357, 118 Stat. 1418-1660 (2004).

[3] Although the degree to which corporations used the proceeds of the 2004 holiday for buybacks is debatable, whether they did so—even though the statute prohibited such uses—is not. Compare Dhammika Dharmapala, C. Fritz Foley, and Kristin J. Forbes, Watch What I Do, Not What I Say: The Unintended Consequences of the Homeland Investment Act, 66 J. Fin. 753 (2011) with Thomas J. Brennan, Where the Money Really Went: A New Understanding of the AJCA Tax Holiday (Northwestern Law and Economics Working Paper) (2014). What's worse, "the temporary holiday conditioned firms to anticipate future holidays and to change their behavior by placing more earnings overseas than ever before." Thomas J. Brennan, What Happens After a Holiday? Long-Term Effects of the Repatriation Provisions of the AJCA, 5 Nw. J. L. & Soc. Pol'y 1 (2010).

[4] Talib Visram, Tax Cut Fuels Record $200 Billion Stock Buyback Bonanza, CNN.com (June 5, 2018); see also William Lazonick, Stock Buybacks: From Retain-and-Reinvest to Downsize-and-Distribute, Brookings Initiative on 21st Century Capitalism (April 2015), at 2 ("Over the decade 2004-2013, 454 companies in the S&P 500 Index in March 2014 that were publicly listed over the ten years did $3.4 trillion in stock buybacks, representing 51 percent of net income.").

[5] Savvy market observers also worry that the magnitude of this year's buyback spree reflects a troubling trend in corporate investment. See, e.g., Matt Egan, Goldman Sachs Warns Against Falling in Love with Stock Buybacks, CNNMoney.com (April 26, 2018) (noting a recent equity research report describing the perhaps-unsurprising result that, since the 2016 presidential election, "Goldman Sachs's collection of stocks that are focused on capital spending and research and development soared 42% . . . besting the S&P 500's 24% gain").

[6] For an exceptionally clear demonstration as to how buybacks can harm investors while benefiting insiders, see Jesse M. Fried, Insider Trading Via the Corporation, 162 U. Pa. L. Rev. 801, 805 (2014) (referring to stock buybacks as "indirect insider trading" and noting that such "trading likely imposes considerable costs on public investors in two ways. First, just like ‘ordinary' direct insider trading, indirect insider trading secretly redistributes value from public investors to insiders. . . . Second, the use of the corporation as a vehicle for insider trading can lead insiders to waste economic resources.").

[7] In these remarks, I focus on executives' use of buybacks to cash out shares granted as part of compensation packages otherwise designed to link executive pay with long-term performance. There are, of course, circumstances where managers who founded the firm or are otherwise large shareholders seek liquidity for those holdings using buybacks. Those cases, too, should be addressed if the SEC chooses to reevaluate its rules in this area. But here I focus on cases where executives use buybacks to cash out shares granted as stock-based pay.

[8] See, e.g., George Constantinides & Bruce Grundy, Optimal Investment with Stock Repurchase and Financing as Signals, 2 Rev. Fin. Stud. 445 (1989) (providing a theoretical model on the role of repurchases when a firm is undervalued).

[9] Among other reasons, a safe harbor is necessary because firms often pursue buybacks under informational circumstances that might lead to securities-law liability in other contexts. See Fried, supra note 5, at 813-814 ("The SEC takes the position that Rule 10b-5 . . . applies to a firm buying its own shares.").

[10] Securities and Exchange Commission, Final Rule: Purchases of Certain Equity Securities by the Issuer and Others, Release Nos. 33-8335, 34-48766, 17 C.F.R. Pt. 228 et seq.

[11] For example, because these rules permitted firms to announce a buyback—generating a stock-price spike—and then choose not to buy back any stock at all without disclosing that fact to investors, commentators and the SEC worried that managers opportunistically used buyback announcements to manipulate share prices. See, e.g., Jesse Fried, Informed Trading and False Signaling with Open Market Repurchases, 93 Cal. L. Rev. 1323, 1336-40 (2005); see also Final Rule, supra note 8 ("Studies have . . . shown that some issuers publicly announce repurchase programs, but do not purchase any shares or purchase only a small portion of the publicly disclosed amount.").

[12] See Final Rule, supra note 8. Among other things, commentators have pointed out that the SEC's still-lax disclosure rules regarding buybacks give corporate insiders "a strong incentive to exploit [those] rules in order to engage in indirect insider trading: having the firm buy and sell its own shares at favorable prices to increase the value of the insiders' equity." Fried, supra note 8, at 804. Indeed, there is important evidence that the limited tightening of disclosure rules in this area have had some benefits in addressing opportunistic buyback activity. See Michael Simkovic, The Effect of Mandatory Disclosure on Open-Market Stock Repurchases, 6 Berkeley Bus. L. J. 98 (2009). That evidence makes the case for revisiting these rules now all the more compelling. Indeed, the Commission issued a proposal to update these rules in 2010, see Proposed Rule, Purchases of Certain Equity Securities by the Issuer and Others, Release No. 34-61414 (2010), but to date has taken no action on the proposal.

[13] See, e.g., Kevin J. Murphy, Executive Compensation: Where We Are and How We Got There, in George Constantinides, Milton Harris, and Rene Stulz, Eds., Handbook on Economics and Finance 211 (2013).

[14] See, e.g., Robert J. Jackson, Jr., Stock Unloading and Banker Incentives, 112 Colum. L. Rev. 951 (2012); Robert J. Jackson, Jr. & Colleen Honigsberg, The Hidden Nature of Executive Retirement Pay, 100 Va. L. Rev. 479 (2014); Robert J. Jackson, Jr. & Jonathon Zytnick, The Effects of a Tax Notch on CEO Golden Parachute Contracts and Option Exercises (working paper 2018).

[15] See, e.g., Kevin Murphy, Executive Compensation, in Orley C. Ashenfelter & David Card, Eds., 3B Handbook of Labor Economics 2485 (1999).

[16] See Lucian A. Bebchuk, Jesse Fried, and David Walker, Managerial Power and Rent Extraction in the Design of Executive Compensation, 69 U. Chi. L. Rev. 751 (2002); see also Lucian A. Bebchuk & Jesse Fried, Paying for Long-Term Performance, 158 U. Pa. L. Rev. 1915, 1921 (2010) (describing concerns related to "ensuring that, whatever equity incentives are used [in executive pay, executives'] payoffs are primarily based on long-term stock values rather than on short-term gains that may be reversed.").

[17] Lucian A. Bebchuk, Alma Cohen, and Holger Spamann, The Wages of Failure: Executive Compensation at Bear Stearns and Lehman 2000-2008, 27 Yale. J. Reg. 257 (2012).

[18] Robert J. Jackson, Jr., Private Equity and Executive Compensation, 60 U.C.L.A. L. Rev. 638, 640 (2013) ("[T]he pay-performance link is much weaker in public companies than in companies owned by private equity investors. Borrowing from their private equity counterparts, public company boards seeking to strengthen the link between pay and performance should restrict CEOs' freedom to unload.").

[19] See, e.g., Dodd-Frank Wall Street Reform and Consumer Protection Act §§ 953(a), 954, 955, Pub. L. No. 111-203, 124 Stat. 1376 (2010) (requiring the SEC to adopt rules requiring disclosure of the pay-performance link, public companies' policies related to the clawback of erroneously awarded compensation, and policies related to insider hedging of public companies' stocks, none of which has been finalized).

[20] We drew information on buybacks from the Securities Data Company (SDC) database, using transactions identified by SDC as buybacks with announcements in the year 2017 and the first three months of 2018. For consistency in treatment across the sample, we identify an initial sample of 708 repurchases and retain only the first repurchase announcement by each company—and only those repurchases not followed by a subsequent repurchase announcement within 60 days. We merged those data with information from the Center for Research on Securities Prices (CRSP) database, leaving a sample of 385 public company buybacks.

[21] We used data from Form 4 filed pursuant to Section 16. See Securities and Exchange Commission, Ownership Reports and Trading By Officers, Directors and Principal Securities Holders, 56 Fed. Reg. 7,242 (Feb. 21, 1991); see also Securities and Exchange Commission, Mandated Electronic Filing and Web Site Posting for Forms 3, 4 and 5, 68 Fed. Reg. 25,788 (May 13, 2003).

[22] That finding is consistent with the longstanding finance literature on the effects of these announcements on stock prices. See, e.g., David Ikenberry, Josef Lakonishok, and Theo Vermalen, Market Underreaction to Open Market Share Repurchases, 39 J. Fin. Econ. 181 (1995); Jesse M. Fried, Insider Signaling and Insider Trading with Repurchase Tender Offers, 67 U. Chi. L. Rev. 421 (2000).

[23] On an average day, between 3 and 4 percent of corporate insiders trade in the company's stock, but we found that, during the eight days following a buyback announcement, more than 8 percent do. We direct the interested reader to the data appendix to this speech, where you can learn more about our methodology and analysis.

[24] Investors receive a mixed signal from a buyback announcement that is accompanied by insider selling. Indeed, as we explain in our data appendix, we observe statistically significantly lower returns during the ten- and thirty-day window following buyback announcements with executive selling than we do in buybacks where executives hold their shares for the long term.

[25] The precise way in which the safe-harbor could be restructured to disfavor the use of buybacks for insider sales is beyond the scope of my remarks—and, in all events, well within the expertise of our exceptional Staff. Suffice it to say that, if the Commission were so inclined, our Staff would have little difficulty making sure that our rules are not used in a way that encourages corporate executives to use buybacks to sell their shares.

[26] We should also use this opportunity to review other problems with Rule 10b-18 and related rules—including the fact that they require only quarterly disclosure of the amount of shares a company has actually repurchased, leaving investors largely in the dark about corporate trading in their own shares. For an exceptionally thoughtful proposal in this respect, see Fried, supra note 5.

[27] Except, of course, the fact that our rules let them. See Final Rule, supra note 8; but see Schnell v. Chris-Craft Industries, Inc., 285 A.2d 437, 444 & n.15 (Del. 1971) ("Inequitable action does not become permissible simply because it is legally possible.").

[28] It's true, of course, that investors eventually receive disclosure of executives' selling on Form 4, which is how we were able to conduct this study. But those disclosures come after the executive has already sold—too late for shareholders to price the executive's decision into their own determination whether to sell their shares. See Fried, supra note 5.