Chapter 3 — Identifying a Lease

Chapter 3 — Identifying a Lease

3.1 Introduction

As indicated in the decision tree in Section 2.2, whether a contract is within the

scope of ASC 842 is only a gating question. Once an entity determines that the

contract is within the scope, it must then proceed through the analysis in ASC

842-10-15 to determine whether the contract is or contains a lease.

Although a contract is not recognized and measured until commencement if it is a lease (see Chapters 8 and 9 for a detailed discussion of lessee and lessor accounting, respectively), the lease identification analysis must be performed at inception. If an arrangement is determined not to be, or not to contain, a lease, an entity must look to other U.S. GAAP (e.g., ASC 606) to determine the appropriate accounting and must apply the appropriate recognition and measurement guidance in such GAAP at whatever time is required, which could be at a contract’s inception.

Changing Lanes

Definition of a Lease Is the New Line

Between On- and Off-Balance-Sheet Treatments

Under ASC 842, the determination of whether an

arrangement is or contains a lease is critical. A lessee’s failure to

identify leases, including those embedded in service arrangements, is likely

to lead to a financial statement error given that ASC 842 requires lessees

to reflect all leases, other than short-term leases, on the balance sheet

(see Chapter 8

for further discussion of the lessee accounting model). On the other hand,

if a customer concludes that a contract is a service arrangement and does

not contain an embedded lease, the customer is not required to reflect the

contract on its balance sheet (unless it is required to do so by other U.S.

GAAP).

The assessment of the arrangement may be more critical under

ASC 842 than under ASC 840 because, under ASC 840, the balance sheet and

income statement treatment of operating leases was often the same as that of

service arrangements. In other words, under ASC 840, the difference between

on- and off-balance-sheet treatments often depended on whether the lease is

classified as operating or capital. Under ASC 842, however, all leases

(other than short-term leases) are on the balance sheet. Therefore, an

off-balance-sheet treatment will often depend on whether an arrangement

meets the definition of a lease.

3.2 Definition of a Lease

ASC 842-10

15-3 A contract is or contains a lease if the contract conveys the right to control the use of identified property,

plant, or equipment (an identified asset) for a period of time in exchange for consideration. A period of time

may be described in terms of the amount of use of an identified asset (for example, the number of production

units that an item of equipment will be used to produce).

Pending Content (Transition

Guidance: ASC 842-10-65-7)

15-3A As a practical

expedient, an entity that is not a public business

entity; a not-for-profit entity that has issued or

is a conduit bond obligor for securities that are

traded, listed, or quoted on an exchange or an

over-the-counter market; or an employee benefit

plan that files or furnishes financial statements

with or to the U.S. Securities and Exchange

Commission may use the written terms and

conditions of a related party arrangement between

entities under common control to determine whether

that arrangement is or contains a lease. For

purposes of determining whether a lease exists

under this practical expedient, an entity shall

determine whether written terms and conditions

convey the practical (as opposed to enforceable)

right to control the use of an identified asset

for a period of time in exchange for

consideration. If an entity determines that a

lease exists, the entity shall classify and

account for that lease on the basis of those

written terms and conditions. An entity may elect

the practical expedient on an

arrangement-by-arrangement basis.

15-3B If no written terms or

conditions exist, an entity shall not apply the

practical expedient in paragraph 842-10-15-3A.

Rather, the entity shall determine whether the

related party arrangement between entities under

common control is or contains a lease in

accordance with paragraph 842-10-15-3 and, if so,

classify and account for that lease on the basis

of its legally enforceable terms and conditions in

accordance with paragraph 842-10-55-12.

15-3C If after an entity has

applied the practical expedient in paragraph

842-10-15-3A an arrangement is no longer between

entities under common control, the entity shall

determine whether a lease exists in accordance

with paragraph 842-10-15-3.

-

If the arrangement was previously determined to be a lease and continues to be a lease, the entity shall classify and account for the lease on the basis of the enforceable terms and conditions. If the enforceable terms and conditions differ from the written terms and conditions previously used to apply paragraph 842-10-15-3A, the entity shall apply the modification requirements in paragraphs 842-10-25-9 through 25-17 using the enforceable terms and conditions. If the enforceable terms and conditions are the same as the written terms and conditions previously used to apply paragraph 842-10-15-3A, the modification requirements in those paragraphs are not applicable.

-

If the arrangement was previously not determined to be a lease and is determined to be a lease, the entity shall account for the arrangement as a new lease.

-

If the arrangement was previously determined to be a lease and the lease ceases to exist:

-

A lessee shall apply the derecognition requirements for fully terminated leases in paragraph 842-20-40-1.

-

A lessor with a lease previously classified as a sales-type lease or a direct financing lease shall apply the derecognition requirements for terminated leases in paragraph 842-30-40-2.

-

A lessor with a lease previously classified as an operating lease shall derecognize any amounts that would not exist if the arrangement was not accounted for as a lease and account for the arrangement in accordance with other generally accepted accounting principles (GAAP).

-

15-4 To determine whether a contract conveys the right to control the use of an identified asset (see

paragraphs 842-10-15-17 through 15-26) for a period of time, an entity shall assess whether, throughout the

period of use, the customer has both of the following:

- The right to obtain substantially all of the economic benefits from use of the identified asset (see paragraphs 842-10-15-17 through 15-19)

- The right to direct the use of the identified asset (see paragraphs 842-10-15-20 through 15-26). . . .

15-5 If the customer has the right to control the use of an identified asset for only a portion of the term of the

contract, the contract contains a lease for that portion of the term.

ASC 842-10-15-3 indicates that a lease is a contract — or part of a contract —

in which a supplier conveys to a customer “the right to control the use of

identified [PP&E] for a period of time in exchange for consideration.” The

graphic below illustrates this relationship.

Although the definition of a lease in ASC 842-10-15-3 includes the phrase “in exchange for

consideration,” the identification of a lease does not depend on whether the contract contains stated

or cash consideration. See Chapter 6 for a detailed discussion of lease payments and what constitutes

consideration.

3.2.1 Process for Identifying a Lease

|

To help entities determine whether a

contract is or contains a lease in accordance with ASC

842-10-15-3 and 15-4, the FASB included a flowchart in

its implementation guidance. Each piece of this

flowchart will be further discussed throughout the

remainder of this chapter.

|

ASC 842-10

15-8 Paragraph 842-10-55-1 includes a flowchart that depicts the decision process for evaluating whether a

contract is or contains a lease.

Identifying a Lease

55-1 The following flowchart depicts the decision process to follow in identifying whether a contract is or contains a lease. The flowchart does not include all of the guidance on identifying a lease in this Subtopic and is not intended as a substitute for the guidance on identifying a lease in this Subtopic.

Connecting the Dots

Not a Step-by-Step

Process

The FASB’s flowchart in ASC 842-10-55-1 appears to suggest that the lease identification

assessment comprises a series of steps. For example, the flowchart seems to imply that, in

determining whether it has the right to control the use of an asset, an entity must determine

whether there is an identified asset in the contract before it can move on to assessing the right

to control the use in the following sequential manner:

- Whether there is an identified asset.

- Whether the customer has the right to obtain substantially all of the economic benefits from use of the identified asset.

- Whether the customer has the right to direct the use of the identified asset.

However, Example 10, Case A, in ASC 842-10-55-124 through 55-126 (reproduced in Section

3.7.10) states that when the customer in a contract does not have the right to control the use

of PP&E, an entity does not need to assess whether the PP&E is an identified asset. Accordingly,

we do not think that it is necessary for lease identification to be performed on a step-by-step

basis. (However, a step-by-step assessment is required for the specific evaluation of whether the

customer has the right to direct the use of the asset — see Section 3.4.2 for further discussion.)

One way to think about identifying a lease is that the definition of a lease

sits on a three-legged stool. Each leg represents one of the three

requirements in ASC 842-10-15-4: (1) the contract depends on an

identified asset, (2) the customer has the right to obtain substantially

all of the economic benefits from use of the PP&E, and (3) the

customer has the right to direct the use of the PP&E. If you were to

kick out any one of the three legs (i.e., if you were to determine that

a contract does not meet any one of the requirements), the stool falls

over and the definition of a lease is not met.

The flowchart below illustrates an entity’s determination of whether a contract

is or contains a lease and ties into the discussion in the remainder of this

chapter.

Connecting the Dots

It’s All About

Control

The notion of control is critical in ASC 842. The concept is used to identify a lease as well as to classify one when it is identified (see Chapters 8 and 9 for a discussion of the lessee’s and lessor’s classification, respectively). Accordingly, there is effectively a two-step process related to the control concepts behind the FASB’s ROU model in ASC 842:

- Step 1 — Determine whether the customer has the right to control the use of an identified asset. If so, the contract is or contains a lease. If not, the supplier has the right to control the use of the asset.

- Step 2 — Determine the extent of the customer’s control over the use of the asset. There is a range of outcomes from this step. However, if enough control of the use rests with the customer, the customer effectively obtains control of the entire asset. The extent to which the customer has control of the use of the asset governs the classification of the lease and its accounting.

In paragraphs BC124 and BC125 of ASU 2016-02, the FASB notes that the control concept in the

definition of a lease (i.e., step 1 as described above) should be compatible with the same concept

articulated in the revenue standard (i.e., ASC 606) and the consolidation guidance (i.e., ASC 810). Further,

paragraph BC134 of ASU 2016-02 indicates that, in the determination of whether a customer has the

right to control the use of an asset under ASC 842, the concept of control should have “power” and

“benefits” (or “economics”) elements, just as ASC 606 or ASC 810 do for control of a good (or service) or

another entity, respectively.

The table below compares the control principles from the leasing, revenue, and

consolidation standards.

|

|

Consolidation

|

Revenue

|

Leasing

|

|---|---|---|---|

|

ASC Reference

|

810-10-25-38A

|

606-10-25-25

|

842-10-15-4

|

|

Control principle (power and economics

elements)

|

“A reporting entity shall be deemed to

have a controlling financial interest in a VIE if it has

both of the following characteristics:

|

“Goods and services are assets, even if

only momentarily, when they are received and used (as in

the case of many services). Control of an asset refers

to the ability to direct the use of [power element], and

obtain substantially all of the remaining benefits from,

the asset [economics element].”

|

“To determine whether a contract conveys

the right to control the use of an identified asset . .

. for a period of time, an entity shall assess whether,

throughout the period of use, the customer has both of

the following:

|

3.2.2 Embedded Leases

Section

3.1 clarifies the balance sheet impact of properly

differentiating between a lease and a service under ASC 842. Further, certain

contracts may not be wholly a lease or wholly a service; in fact, it is not

uncommon for some service arrangements to contain a right to control the use of

an asset. An entity may enter into a service arrangement that involves PP&E

necessary to deliver the contract’s promised services. The importance of the

PP&E to the overall delivery of the service may vary depending on the type

of arrangement. For example, a customer contracting for transportation services

to ship a package from Munich to Milwaukee may care little about the PP&E

used to perform the services. In contrast, a customer contracting a vessel and

crew for a specified period to transport its goods where and when it chooses is

likely to be more concerned with the PP&E used in the arrangement. Both

arrangements, however, involve a significant service component provided by the

supplier to operate the PP&E used to fulfill its transportation

obligations.

In accordance with ASC 842-10-15-2, entities must evaluate

service arrangements that involve the use of PP&E to determine whether the

arrangements contain a lease at contract inception. Often, the assessment of

whether a contract is or contains a lease will be straightforward. However, the

evaluation will be more complicated when a service arrangement involves a

specified physical asset or when both the customer and the supplier make

decisions about the use of the underlying asset. Examples of these more

ambiguous and complex arrangements include those that involve cloud computing

services (i.e., if there is a lease of the supporting equipment, such as

mainframes and servers) and cable television services (i.e., if the cable box

provided to the customer is a leased asset).

Further, not all leases will be labeled as such, and leases may

be embedded in larger arrangements. For example, supply agreements, power

purchase agreements (PPAs), and oil and gas drilling contracts may contain

leases (i.e., there may be an embedded lease of a manufacturing facility,

generating asset, or drill rig, respectively). If an entity identifies PP&E

in an arrangement (either explicitly or implicitly), the customer and supplier

must both determine whether the customer controls the use of the PP&E

throughout the period of use.

3.2.2.1 Embedded Leases and Service Providers

In a manner consistent with the discussion in Section

3.2.2, it is important to review contracts (particularly

service contracts) to determine whether they are or contain a lease. When

the service provider also conveys control of PP&E to a customer, an

embedded lease (to the customer) is likely to exist. On the other hand, when

the customer conveys control of PP&E to the service provider to

facilitate the delivery of the service, it is less likely that there is an

embedded lease in the arrangement.

In certain industry sectors, it is common for a customer to

provide a vendor with the use of an asset (e.g., a piece of customer-owned

equipment) so that the vendor can provide goods or services to the customer

(i.e., the “vendor’s revenue contract”). The vendor’s use of the equipment

is typically limited to activities defined in the contract that by their

nature only benefit the customer. Further, the vendor would not have the

right to opt out of using the customer-owned equipment (i.e., the vendor

could not choose to bring vendor-owned or vendor-leased equipment). In

summary, the vendor typically must use the customer-furnished asset and the

asset’s use is contractually limited to fulfilling the terms of the vendor’s

revenue contract with the customer (i.e., the asset cannot be used to

satisfy the terms of other contracts of the vendor and may not be assigned

to third parties).

Arrangements in which customer-furnished assets are used

exclusively to fulfill the vendor’s contract with the customer typically

include either of the following:

-

One or more embedded leases that should be accounted for separately (i.e., a lease from the customer to the vendor and then a corresponding lease back from the vendor to the customer); some may describe such accounting as accounting for the arrangement on a gross basis.

-

No leases (such accounting is sometimes described as accounting on a net basis, suggesting an equal and offsetting exchange of rights because the substance of the transaction is that no leases exist).

We believe that, in accounting for such arrangements, an

entity should carefully evaluate the facts and circumstances to determine

whether control of an asset is transferred through the rights to use the

asset as conveyed in the arrangement. In some cases, it will be appropriate

to recognize a lease; however, we believe that when the three criteria

outlined below are met, control of the asset is not conveyed to one party

(vendor) and then transferred back to the owner (customer).

When the three criteria are met, the substance of the

transaction is that there are no leases (i.e., neither inbound nor outbound)

and the accounting should therefore be on a net basis (i.e., there are no

separate accounting effects related to the customer-furnished assets).

However, if these criteria are not met or are only met for a portion of the

term of the use of the customer-furnished asset, the vendor and customer

should further evaluate whether the customer has leased its asset to the

vendor.

The vendor (potential lessee/sublessor) and customer

(potential lessor/sublessee) should not treat customer-furnished assets as

embedded leases (and recognize the gross effects of such leases) only if all

of the following three criteria are met:

-

Linked contracts — The right to use the asset is directly linked to the revenue arrangement. That is, the arrangement is executed as part of one contract or each part of two or more contracts is deemed to be combined and accounted for as a single transaction since the contracts are interdependent.

-

Coterminous period — Some or all of the period of use of the asset is coterminous with the revenue arrangement. As discussed further below, if the period of use for the asset begins before or ends after the revenue arrangement, this condition would only be satisfied (and therefore net treatment would only be appropriate) for the overlapping period.

-

Restricted use — During the coterminous period identified in criterion 2, the vendor’s use of the asset is either restricted contractually or limited practically to solely transferring the goods or services promised in the revenue arrangement, including restricting the vendor from assigning or transferring the rights of the asset without the customer’s consent.

Accordingly, when all of the above criteria are met, there

are no leases of the asset and there would be no gross-up of revenue and

related expense (i.e., both the customer and the vendor would account for

the arrangement as a typical service contract) for the period in which the

vendor’s use of the identified asset coincides with the related revenue

contract (including renewal/extension options). If the vendor can use the

identified asset for a period longer than the related revenue contract,

there may be a lease for the excess period (i.e., use of the asset before or

after the related revenue contract begins or ends, respectively, provided

that control is conveyed to the vendor before or after the revenue contract

begins or ends, respectively). Therefore, the counterparties would need to

determine whether a lease commences when the related revenue contract

expires (or before it starts) because the output from the use of the

identified asset is no longer limited to satisfying the related revenue

contract.

The examples below illustrate situations in which the three

criteria are met and the arrangements would be accounted for on a net

basis.

Example 3-1

Customer-Furnished Equipment

Contractor C enters into a

three-year arrangement with Governmental Agency G,

the customer. Under the arrangement, C provides G

with military base operations related to mail and

food services while G owns and will provide C with

exclusive use of its mail sorting and delivery

equipment and food service equipment over the

three-year term to execute the services. That is, G

owns and will provide the use of all equipment that

C would need to deliver its services to G. The terms

of the contract explicitly limit C’s use of the

equipment to activities defined in the contract as

“contract activities,” and such contract activities

directly benefit G through the services provided by

C under the arrangement. Further, C cannot assign or

transfer its rights under the contract or further

sublease the equipment.

In this example, the three criteria

are met as follows:

-

Linked contracts — The right to use the equipment is directly linked to the revenue arrangement. That is, the military base operations arrangement is executed as a single contract that includes C’s use of G’s equipment to execute the contract activities that directly benefit G.

-

Coterminous period — The period of use of the equipment is coterminous with the three-year arrangement for military base mail and food services.

-

Restricted use — The right to use the equipment is contractually restricted to solely transferring the services promised in the military base operations arrangement. That is, C cannot use the equipment to derive other economic benefits (through offering services to other customers or for C’s internal use). In addition, the contract explicitly restricts C from assigning or transferring its rights under the contract or further subleasing the equipment.

Accordingly, there is no lease of

the mail sorting and delivery equipment or the food

service equipment. Therefore, G will not recognize

lease income as a lessor for C’s right to use its

assets and a separate lease expense associated with

the embedded lease in the services it receives from

C. Similarly, C will not recognize lease expense as

a lessee for its right to use G’s assets and

separate lease income for its provision of an

embedded lease within its service revenue

agreement.

Example 3-2

Customer-Furnished Property

Vendor V enters into a five-year

arrangement with a customer, Freight Carrier F, to

provide the maintenance services on F’s railcars.

The maintenance facility that V will use to execute

its services is owned by F. That is, F owns and will

provide exclusive use of its maintenance facility to

V to perform all the maintenance work over the

five-year term. The terms of the contract explicitly

limit V’s use of the maintenance facility to

activities defined in the contract as “contract

activities.” Accordingly, V cannot use the

maintenance facility (1) to service any customer

other than F or (2) for its internal use. Vendor V

cannot assign or transfer its rights under the

contract or further sublease the maintenance

facility.

In this example, the three criteria

are met as follows:

-

Linked contracts — The right to use the maintenance facility is directly linked to the revenue arrangement. That is, the maintenance services arrangement is executed as a single contract that includes V’s use of F’s maintenance facility to execute the contract activities that directly benefit F.

-

Coterminous period — The period of use of the maintenance facility is coterminous with the five-year arrangement for maintenance services.

-

Restricted use — The right to use the maintenance facility is contractually restricted to solely transferring the services promised in the maintenance services arrangement. That is, V cannot use the maintenance facility to derive other economic benefits (through offering services to other customers or for V’s internal use). In addition, the contract explicitly restricts V from assigning or transferring its rights under the contract or further subleasing the maintenance facility.

Accordingly, there is no lease of

the maintenance facility.1 Therefore, F will not recognize lease income

as a lessor for V’s right to use its maintenance

facility and a separate lease expense associated

with the embedded lease in the maintenance services

it receives from V. Similarly, V will not recognize

lease expense as a lessee for its right to use F’s

maintenance facility and separate lease income for

its provision of an embedded lease within its

service revenue agreement.

3.2.3 Joint Operations or Joint Arrangements

ASC 842-10

15-4 . . . If the customer in the contract is a joint operation or a joint arrangement, an entity shall consider whether the joint operation or joint arrangement has the right to control the use of an identified asset throughout the period of use.

Companies in a number of industries enter into joint arrangements to achieve a common commercial objective. These arrangements may include the use of specified PP&E for a stated time frame. Accordingly, under ASC 842-10-15-4, entities should evaluate such arrangements to determine whether they have the right to control the use of an asset.

Bridging the GAAP

No Joint Definitions

The terms “joint arrangement” and “joint operation” are defined in IFRS

Accounting Standards but not in U.S. GAAP. Under IFRS 11, a joint

arrangement is “an arrangement of which two or more parties have joint

control” and a joint operation is a type of joint arrangement

“whereby the parties that have joint control of the arrangement have

rights to the assets, and obligations for the liabilities, relating to

the arrangement.”

Although ASC 842 does not define these two terms, their use in U.S. GAAP is

aligned with that in IFRS Accounting Standards. The terms appear in ASC

842-10-15-4 for two reasons:

-

The FASB and IASB decided that the definition of a lease in ASC 842 would be converged with that in IFRS 16.

-

The FASB wanted to close a structuring opportunity so that entities cannot come together in a joint arrangement or joint operation structure to avoid identifying a lease and recognizing lease assets and lease liabilities.

Connecting the Dots

Joint Operating Agreements in the

Oil and Gas Industry

Entities in the oil and gas industry often enter into joint operating agreements (JOAs) in which

two or more parties (i.e., operators and nonoperators), without setting up a separate or new

legal entity, collaboratively explore for and develop oil or natural gas properties by using the

experience and resources of each party. These agreements often require the use of leased

equipment. Questions have arisen regarding ASC 842’s lease assessment requirements for

parties to JOAs. While we expect that the analysis of JOAs will be largely based on facts and

circumstances, the example and analysis below should be helpful to companies as they consider

these arrangements.

Example 3-3

Three companies — A, B, and C — form a JOA to execute an offshore drilling program. For the companies

to fulfill the JOA’s objective, a specific asset (e.g., a drill rig) will be necessary. Company A will act as the

counterparty to major contracts of the JOA, including a five-year contract to lease a specific drill rig from its

owner (Lessor X).

Question 1: Which Party, if Any, Is Leasing the Rig?

Given A’s role as primary obligor in the drill rig lease (the rig’s owner may

not be aware of the JOA and the parties that constitute

it), A will generally be deemed the lessee in the

arrangement. Accordingly, A will record the entire lease

on its balance sheet. Even though other parties will

receive economic benefits from the rig, those benefits

arise from the JOA and do not affect the

economic-benefits analysis of the contract between A and

the rig’s owner, X.

Question 2: What Is the Effect of the JOA?

The JOA’s terms may represent a sublease of the rig from A to the JOA. That is, ASC 842 requires the parties

to the JOA to consider the terms and determine whether the JOA is, or includes, a “virtual” lessee of the rig.

Although the JOA is typically not a legal entity that prepares financial statements, a conclusion that the JOA is a

lessee of the rig would have the following implications:

- Company A, as sublessor, would separately account for its sublease to the JOA (apart from its head lease with X, the rig’s owner).

- Each party to the JOA would need to consider other GAAP (e.g., proportionate consolidation guidance) that may require it to record its pro rata portion of lease assets and lease liabilities.

Note that the “other GAAP” mentioned in Question 2 of the example above may vary by industry (e.g.,

proportionate consolidation guidance is not applicable in many industries). Also note that the analysis

should be performed at the appropriate level, which may not always be the JOA. The “joint operation” or

“joint arrangement” mentioned in ASC 842-10-15-4 could be a subset of a JOA to the extent that multiple

parties have agreed to jointly use an identified asset for a defined time frame. For example, in a five-year

JOA involving five parties, if three of the parties agree to jointly develop a property by using a specified

drill rig for the first two years, it may be necessary to evaluate that two-year agreement to determine

whether it contains a lease.

The above example is not meant to suggest that most JOAs will contain leases but to highlight and explain the analysis that ASC 842-10-15-4 requires for joint arrangements involving the use of specified PP&E. We encourage entities affected by this issue to check with their auditors and accounting advisers for input on the accounting for specific arrangements.

Footnotes

1

While this example focuses on

the maintenance facility itself, a similar

analysis would apply to the land on which the

maintenance facility resides. Furthermore, we

believe that there are scenarios involving

vendor-owned assets attached to customer-owned

land (e.g., vendor-owned solar panels attached to

customer-owned land) whereby the land use rights

would be subject to the interpretive guidance in

this section.

3.3 Identified Asset

In accordance with the definition of a lease in

ASC 842, fulfillment of the contract must depend

on the use of an identified asset. This is an

important concept, as the Board notes in paragraph

BC128 of ASU 2016-02, because the customer must

know the asset over which it is agreeing to have a

right to control the use. Similarly, paragraph

BC105(a)(1) of the 2013 leasing exposure draft

(ED) explained that in contracts that do not

involve an identified asset (e.g., a service), the

customer does not have the right to control the

use of an asset.

Effectively, the FASB recognized that if an arrangement does not contain an identified asset, it is unlikely that the customer has the right to control the use of an asset. Accordingly, the Board decided against broadening the concept of identified assets to include, for example, assets of a particular specification. The Board stated as much in paragraph BC105(a)(2) of the 2013 leasing ED:

In most contracts for which there is no identified asset, the customer does not have the right to control the use of an asset. Consequently, widening the definition in that respect would possibly have forced some entities to go through the process of assessing whether the customer obtains the right to control the use of an asset, only to conclude that it does not. That would potentially have increased costs for little benefit.

Connecting the Dots

Explicit and Implicit Identification Are

Consistent With ASC 840

Paragraph BC128 of ASU 2016-02 states, in part, that the “requirement that there

be an identified asset is substantially the same as the requirement in previous GAAP

that a lease depends on the use of a specified asset.” In addition, ASC 840-10-15-5

noted that a specified asset may be either explicitly or implicitly specified in the

arrangement, which is consistent with ASC 842-10-15-9. Therefore, we do not expect ASC

842 to significantly differ from ASC 840 with respect to the explicit or implicit

identification of an asset.

However, the identified-asset notion in ASC 842’s definition of a lease differs

from ASC 840 regarding the assessment of substitution rights. See Section 3.3.3 for a detailed

discussion of this issue.

In many cases, the PP&E being leased will be

identified by an address, serial number, VIN, GPS

coordinates, etc. However, the assessment

sometimes may be more complex. The decision tree

below illustrates the process an entity should

consider when determining whether PP&E is

identified in the contract:

The remainder of this section walks through this decision tree in greater

detail.

3.3.1 Explicitly and Implicitly Specified Assets

ASC 842-10

15-9 An asset typically is identified by being explicitly specified in a contract. However, an asset also can be identified by being implicitly specified at the time that the asset is made available for use by the customer.

The most observable forms of identified assets are those that are explicitly specified in the arrangement. Typically, an asset is explicitly specified through the inclusion of a serial number or part number in the contract. For example, if a customer enters into an arrangement to lease a computer server and the contract states that the customer has the right to use Server ABC123, the server is explicitly specified. Alternatively, if the contract states that the customer has a right to use any of the company’s servers that meet certain specification and functionality requirements, the server is not explicitly specified.

If an asset is not explicitly specified in the contract, an entity should consider whether an asset is implicitly specified in the arrangement. As stated in ASC 842-10-15-9, an asset that is implicitly specified can qualify as an identified asset. This concept is further expanded in paragraph BC128 of ASU 2016-02:

Nonetheless, when assessing whether there is an identified asset, an entity does not need to be able to identify the particular asset that will be used to fulfill the contract to conclude that there is an identified asset. Instead, the entity simply needs to know whether an asset is needed to fulfill the contract from commencement. If that is the case, an asset is implicitly specified.

The examples below illustrate cases in which assets are implicitly

specified.

Example 3-4

Railcars

Customer JB enters into a contract with Supplier TK to use a railcar to transport hazardous liquids over a three-year period. The contract does not explicitly specify the railcar that will be used to transport JB’s products but does stipulate that the railcar used must be capable of transporting hazardous bulk commodities (e.g., hazardous liquids and gases). Supplier TK has a large fleet of railcars but only one railcar that is designed to transport hazardous bulk commodities. Therefore, although the railcar is not explicitly specified in the contract, it is implicitly specified because TK has only one railcar that can be used to fulfill the contract.

If other, similar railcars are readily available to TK in the marketplace, substitution rights may need to be considered in the analysis as well. See Section 3.3.3 for further discussion of substitution rights.

Example 3-5

Servers

Customer TP, a health care provider, enters into a contract to store sensitive customer information subject to HIPAA regulations in a server farm. The contract does not explicitly specify the server farm that will be used by TP. However, because of the highly sensitive nature of the information that will be stored in the servers, the contract states that the server farm used must meet specific security and encryption requirements. Although the supplier has various server farms across the country, it only has one server farm with servers outfitted to match the security and encryption requirements outlined in the contract. Therefore, although that server farm is not explicitly specified in the contract, the server farm is implicitly specified as a result of the contractual provisions. To determine whether there is an identified asset, the parties must next assess whether the contract involves a capacity portion of the implicitly specified server farm that represents substantially all of the capacity of the server farm (see Section 3.3.2).

Example 3-6

Satellites

Supplier KB enters into a contract with Customer NL for satellite services so that the end users of NL’s services

can communicate across the globe. Supplier KB operates and maintains several satellites in orbit. However,

the services NL offers include global communication with specific compression and encryption. Accordingly,

NL needs a satellite that can transmit a unique signal that is specifically compressed and encrypted. Supplier

KB only has one satellite in orbit that can transmit this signal. Therefore, although this satellite is not explicitly

specified in the contract, it is implicitly specified because of the terms of the contract with NL. To determine

whether there is an identified asset, the parties must next assess whether the contract involves a capacity

portion of the implicitly specified satellite that represents substantially all of the capacity of the satellite (see

Section 3.3.2).

Connecting the Dots

Identified Assets When the Customer Has the

Right to Select and Use Parcels of Land Within a Larger Plot

Certain contracts grant customers the right to select and use a parcel of land within a larger plot

of land for a period of time. In these situations, the customer would need to assess whether it

has exclusive use of the parcels selected and whether the landowner retains the right to use

the remainder of the land that has not been selected by the customer. Questions have arisen

regarding whether the specified asset in these arrangements is the specific parcel(s) of land

selected by the customer or the larger plot of land. This determination is based on facts and

circumstances, and reasonable judgment may need to be applied. The example below illustrates

such scenarios. Also see Section 2.4 for a similar discussion related to land easements.

Although an asset may be explicitly or implicitly specified in the arrangement,

an entity must also evaluate whether (1) the

specified asset is a portion of a larger asset and

whether that portion is physically distinct or

substantially all of the larger asset’s capacity

and (2) the supplier has the right to substitute

the underlying asset throughout the period of use

and, if so, whether the supplier’s substitution

right is substantive. See the next section and

Section 3.3.3 for further discussion

of portions of assets and substantive substitution

rights, respectively.

3.3.2 Portions of Assets (Capacity and Physical Distinctness)

ASC 842-10

15-16 A capacity portion of

an asset is an identified asset if it is

physically distinct (for example, a floor of a

building or a segment of a pipeline that connects

a single customer to the larger pipeline). A

capacity or other portion of an asset that is not

physically distinct (for example, a capacity

portion of a fiber optic cable) is not an

identified asset, unless it represents

substantially all of the capacity of the asset and

thereby provides the customer with the right to

obtain substantially all of the economic benefits

from use of the asset.

An entity will need to use judgment in distinguishing between a lease and a capacity contract. ASC 842-10-

15-16 clarifies that a “capacity portion of an asset is an identified asset if it is physically distinct” (e.g., a

floor of a building).

Example 3-7

Use of a Portion of a Fiber-Optic Cable

Customer M, a telecommunications provider, enters into a 10-year contract with Supplier R for the right to use two fibers in a fiber-optic cable to transport data from New York City to London. Each fiber within the fiber-optic cable is physically distinct, and the contract explicitly specifies the two fibers that will be provided to M; therefore, the arrangement contains an identified asset.

On the other hand, a capacity portion of a larger asset that is not physically

distinct (e.g., a percentage of the capacity of a

pipeline) is not an identified asset unless the

portion represents substantially all of the

asset’s capacity.

Although ASC 842 does not

define “substantially all,” it uses the term in

the context of determining whether a capacity

portion of an asset represents an identified asset

as well as in discussion of the lease

classification test (i.e., determining whether the

present value of the lease payments represents

substantially all of the fair value of the

underlying asset). To help entities determine

whether the “substantially all” criterion is met

in the lease classification test, the FASB

included implementation guidance that allows

entities to use a 90 percent threshold.

Specifically, paragraph BC73 of ASU 2016-02

states, in part:

Nevertheless, the Board

understands that entities need to ensure the

leases guidance is operational in a scalable

manner, which often requires the establishment of

internal accounting policies and controls. As a

result, the Board included implementation guidance

in Topic 842 that states that one reasonable

application of the lease classification guidance

in that Topic is to conclude, consistent with

previous GAAP, that . . . 90 percent or greater is

“substantially all” the fair value of the

underlying asset.

Likewise, we believe that 90

percent should generally be used to determine

whether a capacity portion of an asset meets the

“substantially all” threshold. Therefore, under

this guidance, if the capacity portion being used

by the customer is 90 percent or more of the

asset’s total capacity, the customer is using

substantially all of the capacity of the asset. In

such a scenario, the entire asset would represent

an identified asset (subject to the guidance on

substantive substitution rights, discussed in

Section 3.3.3). Companies should

consult with their auditors, accounting advisers,

or both if they are considering the use of a

different percentage threshold for this

purpose.

Again, the FASB’s decisions

regarding portions of larger assets reflect the

importance of the control concept and establishing

which party to the arrangement controls the right

to use an asset. Paragraph BC133 of ASU 2016-02

states, in part, the following:

The Board concluded that a

customer is unlikely to have the right to control the use of a capacity portion of a

larger asset if that portion is not physically distinct (for example, if it is a 20

percent capacity portion of a pipeline). The customer is unlikely to

have the right to control the use of its portion because decisions about the use of

the asset are typically made at the larger asset level. [Emphasis added]

The examples below illustrate

the application of the guidance in ASC

842-10-15-16.

Example 3-8

Use of a

Portion of a Pipeline

Customer C enters into a

five-year contract with Supplier S for the right

to transport natural gas through S’s pipeline from

the Marcellus shale supply region in Pennsylvania

to the New York/New Jersey demand region. The

contract specifies the amount of the pipeline’s

capacity that C may use throughout the five-year

period. In each case, S has the right to contract

with other customers for the remaining capacity

not being used by C.

Case A

— Capacity Is Substantially All

The contract gives C the right

to use 93 percent of the capacity of S’s pipeline. In this case, because 93

percent represents substantially all of the pipeline’s capacity, the arrangement

contains an identified asset (i.e., S’s pipeline).

Case B

— Capacity Is Not Substantially All

The contract gives C the right

to use 26 percent of the capacity of S’s pipeline.

In this case, C does not have the right to use

substantially all of the pipeline’s capacity;

therefore, the arrangement does not contain an

identified asset.

Example 3-9

Use of a

Portion of a Warehouse

Case A

— Contract Does Not Contain an Identified

Asset

Customer LH enters into a

contract with a warehouse operator to store up to

1,000 pallets of spare-parts inventory at one of

the operator’s warehouse locations for a

three-year period. The operator’s warehouse can

store up to 10,000 pallets of inventory. During

the contract period, the warehouse operator can

use the remaining space in its warehouse for other

storage needs. In addition, the warehouse operator

can relocate LH’s pallets within the warehouse at

any time without incurring significant costs.

Because LH does not have

exclusive use of a specified portion of the

warehouse and the portion being used is not

substantially all of the warehouse capacity, there

is no identified asset. Although the contract

specifies the amount of spare-parts inventory that

will be held, the warehouse operator can change

the inventory’s location within its warehouse at

any time.

Case B

— Contract Contains an Identified

Asset

Assume the same facts as in

Case A, except that the operator’s warehouse can

only store up to 1,100 pallets, rather than

10,000. In addition, assume that the operator

cannot relocate the inventory to a different

facility.

Since Customer LH’s storage

requirement accounts for substantially all of the

capacity of the operator’s warehouse (more than 90

percent), the arrangement contains an identified

asset (i.e., the operator’s warehouse).

Connecting the Dots

Arrangements Involving Rights to Use Portions

of Larger Assets

We have received questions

about so-called secondary-use arrangements in

which a customer shares the use of part of a

larger asset for a defined period. Examples of

such arrangements include advertising placed on

the side of a fixed asset and nonutility

customers’ attachment of distribution wires (e.g.,

cable wires) to utility poles. Often, we have been

asked (1) how to assess economic benefits when two

parties contemporaneously use the same asset and

(2) what unit of account to use for the evaluation

of control (the larger asset or the portion being

shared).

ASC 842-10-15-16 provides

guidance on evaluating whether a portion of an

asset would be considered an “identified asset”

and could be subject to ASC 842. Under this

guidance, a “capacity or other

portion of an asset that is not physically

distinct . . . is not an identified asset, unless

it represents substantially all of the capacity of

the asset and thereby provides the customer with

the right to obtain substantially all of the

economic benefits from use of the asset” (emphasis

added).

Questions sometimes arise

regarding physical distinction, particularly in

scenarios involving a larger asset, a specific

portion of which is shared by one or more parties

over a defined period for use in different ways.

An example would be a building’s exterior wall to

which one party is granted the exclusive right for

advertising while the occupants of the building

continue to use the wall for support of their

residence, protection from the elements, and so

forth. Unlike situations involving the lease of

one floor of a multistory building, which is

functionally independent and unique, these

scenarios involve simultaneous but different uses

of a portion of a larger asset. Other examples

include the placement of solar panels on a

specific section of rooftop and the attachment of

cable wires to a specific spot on a utility pole

(in both cases, the owner continues to use the

entire asset while allowing another party to use a

portion of the asset for a different purpose over

a defined period). To the extent that there are

substantive substitution rights in these

arrangements, a lease will generally not be

present. However, we understand that many of the

scenarios found in practice do not allow for

substitution. (See Section 3.3.3

for a detailed discussion of substitution

rights.)

Some considerations that may

ultimately be relevant to the determination of

whether a lease exists include whether:

-

The arrangement involves a shared use of the larger asset, including the portion specified in the arrangement.

-

The portion being used by the customer is functionally independent and therefore separable from the larger asset.

-

The portion being used by the customer is commercially significant to the asset owner by design.

Shared

Use

Shared-use arrangements will

typically involve the contemporaneous use of the

same asset (or the same portion of a larger asset)

for different purposes. For example, many

advertising scenarios feature shared use (e.g., an

ad displayed on top of a baseball dugout, on the

side of a bus, or on the floor of a grocery

store). On the other hand, if the owner of the

asset is not contemporaneously using the asset (or

is not contractually allowed to use the asset),

shared use may not exist (e.g., a cell tower

operator that allows a customer to use a specific

hosting site on the tower for a defined period or

a satellite owner that allows a customer to use a

specific transponder on the satellite for a period

of time). Shared-use arrangements are less likely

to contain leases, while exclusive-use

arrangements (i.e., arrangements in which a

customer has exclusive use of a portion of a

larger asset) are more likely to contain leases.

An entity may need to use judgment in determining

whether a particular arrangement features shared

or exclusive use of the portion of the larger

asset.

Functional Independence

It may be useful to evaluate

the functional independence of the portion being

used by the customer, including the functional use

and design of the asset that is subject to the

arrangement. To the extent that the portion being

used by the customer has a discrete functional use

(e.g., a specific floor of a building), it could

be more likely that the portion being used is

physically distinct and an identified asset. On

the other hand, if the portion being used is not

functionally distinguishable from the larger asset

(e.g., a spot on a utility pole), there may be a

reasonable basis for viewing the larger asset as

the identified asset in the arrangement.

Commercial Significance by Design

It may also be useful to

consider commercial significance by design — that

is, the commercial objectives of the asset owner

when it built or purchased the asset. To the

extent that the asset was built or purchased with

the commercial objective of leasing a specific

portion or portions to others (e.g., specific

hosting locations on a cell tower), it could be

more likely that the portion being used for these

purposes is physically distinct and therefore an

identified asset. On the other hand, if the asset

was built or purchased without such a commercial

objective (e.g., a utility pole), there may be a

reasonable basis to view the larger asset as the

identified asset in the arrangement.

Determining Whether a Lease Exists

The above indicators may help

entities assess circumstances in which the use of

a portion of an asset might reasonably be viewed

as a secondary, or incidental, use of that portion

of the asset such that the owner retains

substantive economic benefits from the use of the

portion. Sometimes, it may be reasonable to view

the larger asset as the identified asset in the

arrangement and to assess control (including

economic benefits) on that basis. Such an approach

would generally make it more likely that the

arrangement does not contain a lease since the

customer may not obtain substantially all of the

economic benefits from the use of the larger asset

(the customer’s economic benefits are limited to

the portion it uses). The right to control the use

of an identified asset is discussed in detail in

Section 3.4, while the

economic-benefits element of control is discussed

in Section

3.4.1.

Our current views on this

topic are expressed in the examples and table

below. The SEC staff has indicated that it would

respect an entity’s conclusion regarding such

arrangements provided that it was based on

reasonable judgment. Therefore, arrangements

involving rights to use portions of larger assets

should be based on a careful assessment that takes

into account all relevant facts and

circumstances.

Example 3-10

Contract

for the Use of Space on a Cell Tower

Customer A enters into a

five-year contract with Supplier B to use space on

a cell tower. Customer A is assigned a

specifically identified hanger (hosting spot) on

the cell tower on the basis of its needs to

install its antennae and other telecommunications

equipment. Each hosting spot is commercially

designed to be leased by B’s customers, and each

comprises its own functionally independent

infrastructure that allows B’s customers to

install their equipment at the hosting spots.

Accordingly, A is not the only party with

equipment installed on the overall tower; rather,

A shares the use of the tower with third

parties.

Supplier B is not permitted to

move A’s equipment to a different hosting spot or

cell tower. In addition, A is the only party that

may install equipment on its identified hosting

spot. Customer A may install whatever antennae or

equipment it wants, subject to certain maximum

weight and height restrictions.

The arrangement contains an

identified asset because (1) the hosting spot is

explicitly identified in the contract and is

physically distinct from the larger asset (i.e.,

from the cell tower) and (2) B may not substitute

the asset (i.e., it may not move A’s equipment to

a different hosting spot or tower). Alternatively,

if B had the right to substitute hosting spots or

towers, the parties must assess whether that right

is a substantive substitution right (see Section

3.3.3).

Example 3-11

Contract

for the Use of a Portion of a Satellite

Customer A enters into a

five-year contract with Supplier B to use space on

a satellite. In a manner similar to the assigning

of the hanger on the cell tower in the example

above, A is assigned a specifically identified

transponder on the satellite. Each transponder is

commercially designed to be leased to B’s

customers, and each comprises its own functionally

independent infrastructure that allows B’s

customers to transmit data signals to and from the

transponder. Accordingly, A shares the use of the

overall satellite with third parties.

Supplier B is not permitted to

transfer A to a different transponder or satellite

for reasons other than warranty-related

considerations. In addition, A is the only party

that may transmit data signals to and from its

identified transponder. Customer A may transmit

whatever data it wants, subject to certain

frequency limitations that stem from the nature of

the transponder and satellite.

The arrangement contains an

identified asset because (1) the transponder is

explicitly identified in the contract and is

physically distinct from the larger asset (i.e.,

from the satellite) and (2) B does not have a

substantive substitution right (i.e., it may not

transfer A to a different transponder or

satellite, except for warranty-related

considerations).

|

Asset (Use)

|

Identified Asset?

|

Basis

|

|---|---|---|

|

Wall space (e.g., painting an advertisement on the side of

a building)

|

No

|

The advertising is a secondary use of the wall. That is,

the wall’s primary purpose — the reason it was commercially designed — is to

hold up the building structure and protect the building’s occupants from the

elements. In addition, the advertiser is unlikely to obtain substantially

all of the capacity (or economic benefits from use) from the wall by using

its portion, which indicates that there is not an identified asset with

respect to the portion.

|

|

Retail floor advertising space (e.g., painting an

advertisement on the floor of a grocery store)

|

No

|

Similar to the basis articulated for wall space.

|

|

Side of a bus shelter or commuter train shelter (e.g.,

placing an advertisement on one wall of the shelter)

|

No

|

Similar to the basis articulated for wall space.

|

|

Billboard (e.g., placing an advertisement on a stand-alone

billboard or a billboard attached to another structure)

|

Yes

|

A billboard is commercially designed to be contracted to

customers for displaying advertisements. In addition, billboards attached to

other, larger structures (e.g., when hung on the side of a building) are

physically distinct from the larger structure.

|

|

Taxi tent (e.g., placing an advertisement on the sides of

a removable, magnetic tent on top of a taxi)

|

Yes

|

Similar to the basis articulated for a billboard (i.e., a

taxi tent is effectively a mobile billboard).

|

|

Pole attachments (e.g., either (1) a utility attaching its

lines to a pole owned by a phone company, or (2) a phone company attaching

its wires to a pole owned by a utility)

|

No

|

All spots on the pole where a customer would hang its

wires are functionally dependent on the rest of the structure, and none are

physically distinct.

|

|

Space on a rooftop to construct a bar or restaurant

|

Yes

|

In this case, the rooftop functions independently as a

floor in a building would. In accordance with ASC 842-10-15-16, the floor of

a building is a physically distinct portion of a larger asset.

|

|

Space on a rooftop for an advertisement (e.g., for when

commercial airplanes fly overhead)

|

No

|

Similar to the basis articulated for wall space, retail

floor advertising space, and the side of a bus shelter or commuter train

shelter.

|

|

Space on a rooftop to install solar panels (e.g., that

serve tenants of the building or a utility’s larger customer base)

|

It depends

|

Judgment is required. Space on a rooftop to install solar

panels may be similar to (1) space on a rooftop to construct a bar or

restaurant, (2) space on a rooftop for an advertisement, or (3) both of

these.

|

|

Kiosk in a mall (e.g., used by a customer for retail

purposes)

|

Yes

|

As long as there are no substitution rights akin to those

in Example 2 in ASC 842-10-55-52 through 55-54 (reproduced in Section 3.7.2), the

kiosk is physically distinct, functionally independent, and commercially

designed to be contracted to customers as retail space.

|

3.3.2.1 Pipeline Laterals and First-Mile/Last-Mile Connections (Identified Asset)

Pipelines are generally

constructed and operated in sprawling and integrated networks that transport natural

gas, oil, and refined products from supply regions to demand regions. Some customers are

connected to, and receive deliveries of transported commodities through, the larger

pipeline system via dedicated laterals. In addition, a pipeline system must, by its

nature, have starting and ending points. Therefore, these customers are connected to the

pipeline system through laterals, because they are connected to the first mile or last

mile of the larger pipeline system.

Customers connected to a

lateral or first mile/last mile of a pipeline system enter into contracts with the

pipeline system owner for transportation services through the network to their

connection point. Those contracts should be assessed to determine whether they are or

contain leases of the lateral or first mile/last mile.

ASC 842-10-15-16 (reproduced in Section 3.3.2) states

that a “capacity portion of an asset is an

identified asset if it is physically distinct (for

example, a floor of a building or a segment of

a pipeline that connects a single customer to the

larger pipeline)” (emphasis added). Pipeline

laterals and first-mile/last-mile connections

therefore are physically distinct from the larger

asset (i.e., the integrated pipeline system) and

are identified assets.

The FASB addressed this topic

at its May 10, 2017, Board meeting on implementation issues related to ASC 842. The

Board agreed that under ASC 842-10-15-16, a pipeline lateral is an identified asset and

that the assessment of whether it is a lease must focus on whether the customer has the

right to control the use of the identified asset in accordance with ASC 842-10-15-4

(reproduced in Section

3.2). See Section

3.4.2.1.2.2 for further discussion of the analysis related to whether the

customer has the right to control the use of the identified asset (i.e., the pipeline

lateral).

First-mile/last-mile

connections to other types of assets and infrastructural systems are generally

identified assets. In accordance with ASC 842-10-15-16, a portion of a larger asset is

physically distinct, and thus an identified asset, if it connects a single customer to

the larger asset or system. Even when the portion is part of a contiguous asset and is

not separable from the larger system, that portion may only serve a single customer and

thus is physically distinct.

Portions of assets to which

the guidance in ASC 842-10-15-16 may apply include, but are not limited to:

- Train tracks that connect a customer’s facility to the larger rail network.

-

Electric distribution lines that run (either overhead or underground) from the street, transformer, etc., to a customer’s home or facility.

-

Telephone wires that run (either overhead or underground) from the street to a customer’s home.

-

Coaxial and fiber-optic cables (i.e., for cable television and Internet) that run (either overhead or underground) from the street to a customer’s office building.

In line with the above

discussion, even if the arrangement depends on an identified asset because the first

mile/last mile is considered physically distinct, the customer may not have the right to

direct the use of the first mile/last mile (see Section 3.4.2.1.2.2 for detailed discussion).

3.3.3 Substantive Substitution Rights

ASC 842-10

15-10 Even if an asset is

specified, a customer does not have the right to

use an identified asset if the supplier has the

substantive right to substitute the asset

throughout the period of use. A supplier’s right

to substitute an asset is substantive only if both

of the following conditions exist:

-

The supplier has the practical ability to substitute alternative assets throughout the period of use (for example, the customer cannot prevent the supplier from substituting an asset, and alternative assets are readily available to the supplier or could be sourced by the supplier within a reasonable period of time).

-

The supplier would benefit economically from the exercise of its right to substitute the asset (that is, the economic benefits associated with substituting the asset are expected to exceed the costs associated with substituting the asset).

15-11 An entity’s evaluation of whether a supplier’s substitution right is substantive is based on facts and

circumstances at inception of the contract and shall exclude consideration of future events that, at inception,

are not considered likely to occur. Examples of future events that, at inception of the contract, would not be

considered likely to occur and, thus, should be excluded from the evaluation include, but are not limited to, the

following:

- An agreement by a future customer to pay an above-market rate for use of the asset

- The introduction of new technology that is not substantially developed at inception of the contract

- A substantial difference between the customer’s use of the asset, or the performance of the asset and the use or performance considered likely at inception of the contract

- A substantial difference between the market price of the asset during the period of use and the market price considered likely at inception of the contract.

Once an entity has determined that PP&E is specified in a contract, it must also evaluate whether

the supplier has the right to substitute the underlying asset throughout the period of use and, if so,

whether the supplier’s substitution right is substantive. If the supplier has a substantive substitution

right, the underlying asset does not represent an identified asset and the contract does not contain a

lease. Paragraph BC128 of ASU 2016-02 notes that the FASB’s reason for establishing this requirement

was that if a supplier has a substantive right to substitute the asset throughout the period of use, “the

supplier (and not the customer) controls the use of the asset . . . , thereby deciding for what purpose the

asset is used.”

Accordingly, the FASB developed guidance in ASC 842-10-15-10 through 15-15 to help entities determine whether a substitution right is substantive. The Board explains in paragraph BC129 of ASU 2016-02 that its purpose in establishing this guidance was to differentiate between the following:

- Substitution rights that result in there being no identified asset because the supplier, rather than the customer, controls the use of an asset

- Substitution rights that do not change the substance or character of the contract because it is either not practically or economically feasible for the supplier to exercise those rights or not likely the supplier will be able to exercise those rights.

When developing the framework for the identified-asset notion in the 2013 leasing ED, the Board received significant feedback from stakeholders indicating that substitution rights and clauses in contracts could be used to structure arrangements so that they did not meet the definition of a lease (and, thus, so that lessees could avoid recognizing lease assets and lease liabilities on the balance sheet). The Board acknowledged this in paragraph BC105(b) of the 2013 leasing ED, which stated, in part:

The [Board has] included additional language to help determine when substitution rights are substantive. [Its] intention in doing so is to discourage the insertion of a substitution clause in a contract, which does not change the substance or character of the contract, solely to achieve a particular accounting outcome.

For a substitution right to be considered substantive, the following two conditions must be met:

- The supplier must have the “practical ability” to substitute the identified asset (see Section 3.3.3.1).

- The supplier must economically benefit from the substitution (see Section 3.3.3.2).

Connecting the Dots

Economically Beneficial Substitution Is a

Higher Hurdle Than Under ASC 840

ASC 840-10-15-10 through 15-14 addressed substitution rights. Generally, if an

arrangement gives the supplier a substitution right and the supplier has the practical

ability to exercise that right, the fulfillment of the arrangement does not depend on

the specified PP&E. Under ASC 840, “practical ability” took into account

contractual, legal, and economic constraints but does not require that a supplier

economically benefit from a substitution.

Accordingly, ASC 842’s requirement that a substitution right be economically beneficial to a supplier is a higher threshold than the requirements in ASC 840. We therefore expect that fewer entities will be able to avoid lease identification as a result of substitution rights in their arrangements. In other words, we expect that more arrangements will be subject to lease accounting under ASC 842.

The next section and Section

3.3.3.2 address how an entity would

assess the two conditions in ASC 842-10-15-10 to

conclude that a substitution right is substantive.

See also Example 2 in ASC 842-10-55-52 through

55-54 (reproduced in Section 3.7.2),

which illustrates the assessment of these

conditions in the context of concession space in

an airport.

3.3.3.1 Practical Ability to Substitute Alternative Assets

ASC 842-10

15-13 If the supplier has a right or an obligation to substitute the asset only on or after either a particular date or the occurrence of a specified event, the supplier does not have the practical ability to substitute alternative assets throughout the period of use.

Common indicators that the supplier has the practical ability to substitute alternative assets throughout

the period of use include the following:

- The customer cannot prevent the supplier from substituting an asset (i.e., the customer cannot block the substitution). See further discussion below.

- Alternative assets are readily available to the supplier or could be sourced by the supplier within a reasonable period. However, in accordance with ASC 842-10-15-11, the supplier may not consider future events that, at inception, are considered unlikely to occur. If such events are considered unlikely to occur, the supplier may not assume in its assessment that alternative assets will be readily available to the supplier because of circumstances such as future manufacturing economies of scale, future technological developments, or assets otherwise becoming available in the future that are not available at inception.

- There are no contractual restrictions on when a supplier may substitute the asset. ASC 842-10-15-13 states that the supplier does not have the practical ability to substitute the asset when substitution rights are only exercisable on, or after, a particular date or are only exercisable upon the occurrence of a certain event or the resolution of a contingency.

These common indicators are further considered below.

Connecting the Dots

When Contractual Provisions Specify That

Customer Approval Is Needed Before Substitution

Certain contracts may specify that the supplier must obtain

approval from the customer before substituting the underlying asset. In such

circumstances, because the customer can block the supplier from substituting the

underlying asset, the supplier does not have the practical ability to substitute the

asset. Therefore, the supplier’s substitution right is not substantive.

To have the practical ability to substitute the asset in

accordance with ASC 842-10-15-10(a), the supplier must be able to substitute the

asset without the customer’s approval. Customer consent or approval rights may come

in different forms. For example, the customer may be contractually granted a right

that allows it to block the substitution itself or may be able to prevent the

supplier from accessing the customer’s premises to substitute the asset when the

underlying asset is located there. An entity should consider the substance and

nature of any rights granted in the contract that may give the customer the right to

prevent substitution.

Substantive Substitution Rights Less Relevant for Implicitly

Specified Assets

We think that the assessment of whether a supplier has a

substantive substitution right in contracts that explicitly specify the asset to be

used to fulfill the contract is generally more relevant than that in arrangements

for which fulfillment depends on the use of an implicitly specified asset. As

discussed in Section

3.3.1, an implicitly specified asset typically exists when the supplier

has only one asset (or very few assets) that may be used to fulfill the supplier’s

obligation under the contract (e.g., a railcar that can carry hazardous commodities,

a server farm with specific security features, or a satellite that can transmit a

unique signal). If a supplier only has one asset that can be used to fulfill its

obligations under the contract, the supplier most likely does not have the practical

ability to substitute the underlying asset. For that reason, a supplier generally

does not have a substantive substitution right for implicitly identified assets.

Example 3-12

Supplier Does Not Have the

Practical Ability to Substitute

Company BC enters into an arrangement with Supplier LP

under which LP will provide a customized Model 5000 copier to BC for two

years. Supplier LP only has one customized Model 5000 copier. The

arrangement allows LP to replace the copier at will. However, LP would

need several months to manufacture such a replacement. Accordingly, no

alternative assets are available for substitution. Because LP only has

one asset that can be used to honor the agreement with BC and does not

have the practical ability to substitute it, LP’s substitution right is

not substantive.

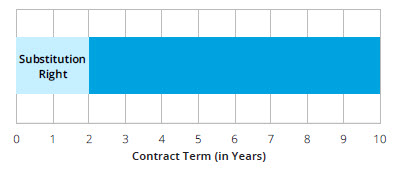

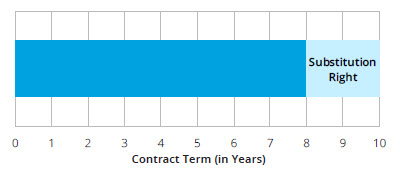

Evaluating the Period of Use When a Substitution Right

Exists

ASC 842-10-15-13 states that when a “supplier has a right or an

obligation to substitute [PP&E] only on or after either a particular date or the

occurrence of a specified event, the supplier does not have the practical ability to

substitute alternative assets throughout the period of use”