Chapter 6 — Cash Conversion Features

Chapter 6 — Cash Conversion Features

6.1 Overview

6.1.1 General Considerations

ASC 470-20

05-13 The Cash Conversion Subsections address certain convertible debt instruments that may be settled in cash upon conversion as specified in paragraph 470-20-15-3.

This chapter discusses the guidance in the Cash Conversion subsections of ASC 470-20 on an issuer’s accounting for certain instruments that contain a CCF. The guidance applies not only to debt instruments but also to liability-classified convertible preferred stock (see Section 6.2.2). However, the CCF guidance does not apply if the conversion feature must be bifurcated and accounted for as a derivative instrument under ASC 815-15 (see Sections 2.3 and 6.2.4.1).

6.1.2 Objective of the CCF Guidance

ASC 470-20

10-1 The objective of the guidance in the Cash Conversion Subsections is that the accounting for a convertible debt instrument within the scope of those Subsections reflect the entity’s nonconvertible debt borrowing rate when interest cost is recognized in subsequent periods.

Economically, a convertible debt instrument can be analyzed as a combination of (1) a debt obligation with a below-market interest coupon and (2) an equity conversion option. Investors are willing to accept a below-market interest rate on their investment because they also receive an equity conversion option. If, for accounting purposes, all the issuance proceeds are attributed to the debt feature, it may appear that the issuer is able to borrow at a below-market rate; however, this ignores the fact that the issuer has given investors a valuable equity conversion option in exchange for the low interest rate. In the absence of a conversion feature, the issuer would have to pay a higher rate that is commensurate with its nonconvertible debt borrowing rate.

Consequently, the objective of the CCF guidance in ASC 470-20 is to ensure that the interest cost of instruments within its scope reflects the issuer’s nonconvertible borrowing rate. That is, as indicated in paragraph B7 of the Background and Basis for Conclusions of FSP APB 14-1, the cost recognized should reflect “the same interest cost [the issuer] would have incurred had it issued a comparable debt instrument without the embedded conversion option.” The issuer accomplishes this by allocating the amounts received as follows:

- To the liability component — An amount of proceeds that equals the fair value of a similar liability that does not have an associated equity component.

- To the equity component — The remainder of the proceeds.

The resulting debt discount (or reduction in debt premium) increases the reported interest cost in future periods as a result of the application of the effective interest method. Since any debt discounts or premiums are amortized to earnings under this method, the reported interest cost includes the implicit interest cost that was “paid” through the inclusion of a conversion option in the instrument.

The FASB concluded that it would be inappropriate to account for convertible

debt instruments that may be settled in cash (including partial settlement) upon

conversion wholly as debt in accordance with ASC 470-20-25-12 (see Chapter 4). In paragraph

B3 of FSP APB 14-1, the Board observed that such accounting guidance “was based,

in part, on [an assumption of] the mutual exclusivity of the debt and the

conversion option such that the holder cannot exercise the option to convert

into equity shares unless the holder forgoes the right to repayment of the debt

component”; however, that assumption is not valid for convertible debt

instruments that may be settled in cash upon conversion. Further, such

accounting “can provide misleading information to investors,” since “the diluted

earnings-per-share treatment of convertible debt instruments with the

characteristics of Instrument C [as described in Section 6.1.3] is a treasury-stock-type method that is

consistent with the diluted earnings-per-share treatment of debt issued with

detachable warrants.”

As indicated in paragraph B5 of FSP APB 14-1, the Board considered but decided against expanding the scope of the CCF guidance “broadly to all convertible debt instruments, including those instruments that must be settled entirely in shares upon conversion,” pending “a broad reconsideration of the accounting for all convertible instruments . . . in connection with the Board’s liabilities and equity project.”

The separation and allocation approach required under the CCF guidance differs from approaches that apply to other types of debt instruments with conversion features. In developing the guidance, the FASB concluded that the liability-first separation approach would be less difficult to apply than an equity-first separation approach or a relative-fair value separation approach that potentially would have required an entity to determine the fair value of the conversion feature by using complex option-pricing models. Further, the Board noted that the CCF guidance has a different objective (i.e., to measure the interest cost that is “paid” with the conversion feature) than other separation or allocation approaches under GAAP (e.g., to measure bifurcated embedded derivatives at fair value; see Section 3.5.4).

6.1.3 Common Variants

While more traditional forms of convertible debt instruments must be physically

settled in the issuer’s equity shares upon conversion, an instrument with a CCF requires or permits settlement of all or part of the instrument’s conversion value by the transfer of cash or other assets. In Issue 90-19, the EITF

identified three variants of convertible bonds with CCFs (Instruments A, B, and

C); and in his remarks at the 2003 AICPA Conference on Current SEC

Developments, then SEC Professional Accounting Fellow Robert Comerford

identified a fourth variant (Instrument X):

|

|

Settlement Provision

|

Description

|

|---|---|---|

|

Instrument A

|

Cash settlement

|

“Upon conversion, the issuer must

satisfy the obligation entirely in cash based on the

fixed number of shares multiplied by the stock price on

the date of conversion (the conversion value).”

|

|

Instrument B

|

Issuer option to elect either cash or

physical share settlement

|

“Upon conversion, the issuer may satisfy

the entire obligation in either stock or cash equivalent

to the conversion value.”

|

|

Instrument C

|

Cash settlement of accreted value and

issuer option to elect either net cash or net share

settlement of conversion spread

|

“Upon conversion, the issuer must

satisfy the accreted value of the obligation (the amount

accrued to the benefit of the holder exclusive of the

conversion spread) in cash and may satisfy the

conversion spread (the excess conversion value over the

accreted value) in either cash or stock.”

|

|

Instrument X

|

Combination settlement

|

“Instrument X provides the issuer with

the ability to settle investor conversions in any

combination of shares or cash.”

|

Example 6-1

Variants of Convertible Debt With CCF

The following table illustrates how Instruments A, B, C, and X, as described above, would be settled if they each

have an accreted value of $1 million and are convertible into 10,000 shares, and the current stock price at the

time of conversion is $125:

Type | Settlement Upon Conversion |

|---|---|

Instrument A | The issuer must pay cash of $1,250,000 (10,000 × $125). |

Instrument B | The issuer can elect to either deliver 10,000 equity shares or pay cash of $1,250,000

(10,000 shares × $125). |

Instrument C | The issuer must pay $1,000,000 of cash to settle the accreted value of the debt obligation.

To settle the conversion spread, the issuer can elect to either deliver 2,000 equity shares

($250,000 ÷ $125) or pay $250,000 of cash. |

Instrument X | The issuer can elect to deliver any combination of cash and shares whose aggregate value

equals $1,250,000 (e.g., 1,000 shares and $1,125,000 of cash). |

Note that convertible debt in the form of Instrument A would be exempt from the scope of the CCF guidance in

ASC 470-20 because of the requirement to cash settle the conversion feature (see Section 6.2.4.1).

6.2 Scope

6.2.1 Convertible Debt

ASC 470-20

15-3 The Cash Conversion Subsections follow the same Scope and Scope Exceptions as outlined in the General

Subsection of this Section, with specific instrument qualifications and exceptions and other considerations

noted below.

15-4 . . . The guidance in the Cash Conversion Subsections applies only to convertible debt instruments that, by

their stated terms, may be settled in cash (or other assets) upon conversion, including partial cash settlement,

unless the embedded conversion option is required to be separately accounted for as a derivative instrument

under Subtopic 815-15. . . .

The CCF guidance in ASC 470-20 applies to an issuer’s accounting for a convertible debt instrument

that meets the following two conditions: (1) upon conversion, it may be settled either fully or partially in

cash or other assets in accordance with its stated terms and (2) the CCF is not required to be separately

accounted for as a derivative instrument under ASC 815-15 (see Sections 2.3 and 6.2.4.1). Thus, if

convertible debt in the form of Instrument B, C, or X (as described in Section 6.1.3) contains a CCF that

is not bifurcated under ASC 815, such instrument is within the scope of the CCF guidance. Similarly, if, upon conversion, a convertible debt instrument permits (1) the counterparty to elect either cash or net share settlement of all or part of the accreted value and (2) the issuer to satisfy the conversion spread in either cash or net shares, such instrument is within the scope of the CCF guidance in ASC 470-20 unless the CCF is bifurcated under ASC 815-15.

6.2.2 Liability-Classified Convertible Preferred Stock

ASC 470-20

15-6 For purposes of determining whether an instrument is within the scope of the Cash Conversion Subsections, a convertible preferred share shall be considered a convertible debt instrument if it has both of the following characteristics:

- It is a mandatorily redeemable financial instrument.

- It is classified as a liability under Subtopic 480-10.

For related implementation guidance, see paragraph 470-20-55-70.

55-70 An example of a convertible preferred share that paragraph 470-20-15-6 requires an entity [to] consider as a convertible debt instrument for purposes of the scope application of the Cash Conversion Subsections is a convertible preferred share that has a stated redemption date and also would require the issuer to settle the face amount of the instrument in cash upon exercise of the conversion option. Such a convertible preferred share is a mandatorily redeemable financial instrument and is classified as a liability under Subtopic 480-10 because it embodies an unconditional obligation to redeem the instrument by transferring assets at a specified or determinable date (or dates).

ASC 480-10 — Glossary

Mandatorily Redeemable Financial Instrument

Any of various financial instruments issued in the form of shares that embody an unconditional obligation requiring the issuer to redeem the instrument by transferring its assets at a specified or determinable date (or dates) or upon an event that is certain to occur.

The CCF guidance in ASC 470-20 applies to the issuer’s accounting for convertible preferred stock that meets all of the following four conditions:

- Upon conversion, it may be settled either fully or partially in cash or other assets in accordance with its stated terms.

- It meets the definition of a mandatorily redeemable financial instrument in ASC 480-10 (see Section 4.1.1 of Deloitte’s Roadmap Distinguishing Liabilities From Equity).

- It is classified as a liability under ASC 480-10 (i.e., it is a mandatorily redeemable financial instrument that is not exempt from the scope of ASC 480-10; see Section 4.1.5 of Deloitte’s Roadmap Distinguishing Liabilities From Equity).

- The CCF is not required to be separately accounted for as a derivative instrument under ASC 815-15 (see Section 2.3).

In the application of the CCF guidance in ASC 470-20, such convertible preferred stock is treated as convertible debt.

For a convertible preferred share to meet the definition of a mandatorily redeemable financial instrument and be classified as a liability under ASC 480-10, it must embody an unconditional obligation to transfer assets. A convertible preferred share that the issuer must settle at least partially in cash irrespective of whether it is converted embodies such an obligation, since a transfer of cash or other

assets is certain to occur unless there is a violation of the contractual terms. A fixed-term convertible

preferred share with conversion terms that are similar to those of Instrument C (as described in Section

6.1.3) typically would meet the definition of a mandatorily redeemable financial instrument and be

classified as a liability under ASC 480-10. Accordingly, such an instrument would be within the scope of

the CCF guidance in ASC 470-20 unless the CCF must be bifurcated as a derivative instrument under

ASC 815-15.

Example 6-2

Convertible Preferred Stock Subject to CCF Guidance

A convertible preferred share has (1) a fixed redemption date on which the issuer will settle its stated par

amount in cash and (2) a substantive conversion option that, if exercised by the counterparty, requires the

issuer to settle the par amount in cash but permits it to settle the excess of the conversion value over the par

amount (the conversion spread) in either cash or shares. The convertible preferred share meets the definition

of a mandatorily redeemable financial instrument and is classified as a liability under ASC 480-10 since the

issuer has an unconditional obligation to transfer cash or other assets in exchange for the par amount.

Because the issuer has the option to settle the conversion spread in either cash or shares upon conversion,

the instrument is within the scope of the CCF guidance in ASC 470-20 unless the issuer concludes that the

conversion feature must be bifurcated as an embedded derivative under ASC 815-15 (see Section 2.3).

A convertible preferred share that has a stated redemption date and permits the

issuer to elect settlement of the entire

instrument in either cash or shares (in a manner

similar to Instrument B as described in Section

6.1.3) or any combination of cash or

shares (in a manner similar to Instrument X as

described in Section

6.1.3) does not contain an

unconditional obligation to transfer assets

because the issuer has the right to settle the

entire conversion value in shares. Accordingly,

preferred stock with terms similar to those of

Instrument B or X is not within the scope of the

CCF guidance in ASC 470-20.

A requirement to transfer assets that is contingent on the counterparty’s election of a cash settlement

or the occurrence (or nonoccurrence) of an uncertain future event represents a conditional, rather

than an unconditional, obligation to transfer assets. Thus, convertible preferred stock that has such

a requirement is not within the scope of the CCF guidance in ASC 470-20. For example, a perpetual

convertible preferred share that must be settled in cash or other assets upon the counterparty’s

election to convert does not meet the definition of a mandatorily redeemable financial instrument in

ASC 480-10 because the obligation to transfer cash or other assets is contingent on such election.

Connecting the Dots

For further discussion of determining whether a share meets the definition of a

mandatorily redeemable financial instrument and would be classified as a

liability under ASC 480-10, see Chapter 4 of Deloitte’s Roadmap

Distinguishing

Liabilities From Equity.

6.2.3 Exceptions

6.2.3.1 Equity-Classified Convertible Stock

ASC 470-20

15-5 The Cash Conversion Subsections do not apply to any of the following instruments:

a. A convertible preferred share that is classified in equity or temporary equity. . . .

The CCF guidance in ASC 470-20 does not apply to convertible instruments that

are classified in equity or temporary equity. For instance, such guidance

does not apply to an equity-classified preferred share that contains an

option for the holder to convert it into a different class of equity shares

even if the conversion terms require or permit the issuer to pay cash to

settle the conversion value. See Chapter 9 of Deloitte’s Roadmap

Distinguishing

Liabilities From Equity for additional guidance on

preferred stock that is classified in temporary equity.

6.2.3.2 Holders of Underlying Shares Receive Same Form of Consideration

ASC 470-20

15-5 The Cash Conversion Subsections do not apply to any of the following instruments: . . .

b. A convertible debt instrument that requires or permits settlement in cash (or other assets) upon conversion only in specific circumstances in which the holders of the underlying shares also would receive the same form of consideration in exchange for their shares. . . .

The CCF guidance in ASC 470-20 does not apply if the convertible debt instrument only requires or permits settlement in cash or other assets upon conversion if the holders of the shares underlying the convertible instrument receive, or have a right to receive, the same form of consideration for their shares. However, this scope exception is not available if, upon conversion, the form of consideration (e.g., cash, shares, property, or other assets) would be different from the form of consideration paid to holders of the underlying shares.

6.2.3.3 Cash Settlement of Fractional Shares

ASC 470-20

15-5 The Cash Conversion Subsections do not apply to any of the following instruments: . . .

c. A convertible debt instrument that requires an issuer’s obligation to provide consideration for a fractional share upon conversion to be settled in cash but that does not otherwise require or permit settlement in cash (or other assets) upon conversion.

A fractional share of stock is a quantity of shares that is less than one full share. The CCF guidance in ASC 470-20 does not apply to a convertible debt instrument merely because it requires or permits the issuer to cash settle any obligation to deliver fractional shares.

Example 6-3

Convertible Debt Instrument With Fractional Shares Settled in Cash

Issuer A has an obligation to deliver 15.333 shares upon conversion of a convertible debt instrument. The terms of the instrument require A to settle the obligation in shares except for any fractional shares, which are settled in a cash amount that equals their current market value. Upon conversion, therefore, A delivers 15 shares and a cash amount that equals the current market value of 0.333 shares. Even though A has an obligation to deliver cash upon conversion, the CCF guidance in ASC 470-20 does not apply because the obligation to deliver cash applies only to fractional shares.

6.2.4 Other Considerations

6.2.4.1 Embedded Derivatives

ASC 470-20

15-4 The guidance in this Section shall be considered after consideration of the guidance in Subtopic 815-15

on bifurcation of embedded derivatives, as applicable (see paragraph 815-15-55-76A). . . . The guidance in the

Cash Conversion Subsections does not affect an issuer’s determination under Subtopic 815-15 of whether an

embedded feature shall be separately accounted for as a derivative instrument.

25-25 If a convertible debt instrument within the scope of the Cash Conversion Subsections contains

embedded features other than the embedded conversion option (for example, an embedded prepayment

option), the guidance in Subtopic 815-15 shall be applied to determine if any of those features must be

separately accounted for as a derivative instrument. As discussed in paragraph 470-20-15-4, the guidance

in the Cash Conversion Subsections does not apply if there is no equity component because the embedded

conversion option is being separately accounted for as a derivative under Subtopic 815-15.

The requirements in ASC 470-20 (e.g., the CCF guidance) do not apply if the conversion feature must

be bifurcated and accounted for as a derivative instrument under ASC 815. Therefore, an issuer needs

to determine whether ASC 815-15 requires bifurcation of the CCF before it can conclude whether the

CCF guidance in ASC 470-20 applies to the instrument. However, if a feature other than the conversion

feature (e.g., a call or put option) must be bifurcated from the convertible debt instrument, the

instrument is not exempt from the CCF guidance in ASC 470-20 (see Section 6.3.6).

Because of this scope exception, the CCF guidance in ASC 470-20 does not apply to convertible debt

instruments in the form of Instrument A (as described in Section 6.1.3). Since the issuer must settle

the conversion feature of such instruments in cash, they meet the net settlement characteristic in the

definition of derivative instruments in ASC 815-10-15-83 and do not qualify for the scope exception

in ASC 815-10-15-74(a) for certain contracts on the entity’s own equity. Further, an equity feature

is not clearly and closely related to a debt host. Therefore, unless the issuer elects to account for

convertible debt in the form of Instrument A at fair value, with changes in fair value recognized in

earnings under the fair value option in ASC 825-10 (see Section 2.5), the conversion feature in such

an instrument is separated as an embedded derivative under ASC 815-15. Irrespective of whether the

issuer bifurcates the conversion feature under ASC 815-15 or elects to apply the fair value option to the

entire instrument under ASC 825-10, convertible debt in the form of Instrument A is exempt from the

scope of ASC 470-20. For similar reasons, the CCF guidance in ASC 470-20 generally does not apply to

a convertible debt instrument if the holder has an option to require the issuer to settle either the full

conversion value or the conversion spread in cash.

A convertible debt instrument within the scope of the CCF guidance in ASC 470-20 could qualify as

conventional convertible debt under ASC 815-40-25-39 if, in a manner similar to Instrument B, the

holder is able to realize the value of the conversion option only by exercising it and receiving the entire

proceeds in a fixed number of shares or an equivalent amount of cash at the issuer’s discretion. In such

a case, some of the equity classification conditions in ASC 815-40-25 would not apply.

Connecting the Dots

For a discussion of the evaluation of whether an equity conversion feature

qualifies as equity under ASC 815-40, see Deloitte’s Roadmap

Contracts

on an Entity’s Own Equity. Section 5.5

of that Roadmap addresses the requirements related to conventional

convertible debt.

6.2.4.2 Share-Settled Redemption or Indexation Features

As discussed in Section 2.4, a contractual term that economically represents a share-settled put, call, redemption, or indexation provision should not be analyzed as a conversion feature under ASC 470-20 even if the instrument’s terms describe it as a “conversion feature.”

Example 6-4

Share-Settled Debt

The terms of a debt instrument include an option that permits the holder to “convert” the instrument on a specified date. Upon conversion, the issuer is required to settle the principal amount and any accrued and unpaid interest either in cash or a variable number of equity shares of equal value. The conversion price is defined as (1) the sum of $1 million plus unpaid and accrued interest divided by (2) the market price of the common stock on the conversion date. Although the contract refers to the option as a conversion feature and the issuer has the right to settle the feature either in cash or equity shares, the instrument should not be analyzed as a debt instrument with a CCF under ASC 470-20 because the monetary amount of the obligation is unrelated to the fair value of the issuer’s equity shares.

6.2.4.3 Fair Value Option

ASC 470-20

25-21 Paragraph 825-10-15-5(f) states that no entity may elect the fair value option for financial instruments that are, in whole or in part, classified by the issuer as a component of shareholder’s equity (including temporary equity) (for example, a convertible debt instrument within the scope of the Cash Conversion Subsections or a convertible debt security with a noncontingent beneficial conversion feature).

Because ASC 470-20 requires the issuer of a convertible debt instrument that is within the scope of the CCF guidance to separate it into liability and equity components at issuance, the issuer is not permitted to elect the fair value option in ASC 825-10 for such an instrument. By analogy, the instrument is also not eligible for the fair value option in ASC 815-15 (see Section 2.5 for further discussion).

6.2.4.4 The SEC’s Requirements Related to Temporary Equity

As discussed in Section 2.6, an issuer that is an SEC registrant should consider whether the SEC’s guidance on redeemable securities in ASC 480-10-S99-3A applies to convertible debt instruments that are separated into liability and equity components under the CCF guidance in ASC 470-20. While the SEC’s guidance on temporary equity applies to equity-classified redeemable stock even if it is not currently redeemable, such guidance does not apply to convertible debt with a CCF that is not currently redeemable even if it may become redeemable in the future. As indicated in ASC 480-10-S99-3A(12), for convertible debt with a CCF, the amount of temporary equity is limited to the excess (if any) of “(1) the amount of cash or other assets that would be required to be paid to the holder upon a redemption or conversion . . . over (2) the carrying amount of the liability-classified component of the convertible debt instrument” both at initial measurement and on subsequent balance sheet dates.

Connecting the Dots

For further discussion of the application of the SEC’s guidance on temporary

equity, see Sections 9.3.5, 9.4.8, 9.5.7, and

9.6.4 of Deloitte’s Roadmap Distinguishing

Liabilities From Equity.

Example 6-5

Application of ASC 480-10-S99-3A to Puttable Convertible Debt With a CCF

A convertible debt instrument subject to the CCF guidance in ASC 470-20 was issued for net proceeds of $100

and includes a cash-settled put option that permits the investor to put the instrument back to the issuer at any

time for $97. As of the issuance date, the issuer concluded that the put option was (1) nonsubstantive (i.e., its

exercise was not probable; see Section 6.3.2.2) and (2) not required to be bifurcated and accounted for as a

derivative under ASC 815-15. As of the reporting date, the current carrying amount of the liability component is

$90 and the current carrying amount of the equity component is $10. In this case, the issuer would present $3

of the equity component in permanent equity and $7 in temporary equity because $7 of the equity component

is currently redeemable (i.e., the excess of the current redemption amount over the carrying amount of the

debt’s liability component).

If, instead, the put option was contingent and the contingency was not met as of the reporting date, no amount

would be presented in temporary equity (irrespective of whether it was probable that the contingency would

be met in the future) because the SEC’s guidance on redeemable securities in ASC 480-10-S99-3A only applies

to convertible debt instruments with a separately classified equity component if the instrument is currently

redeemable or convertible as of the reporting date.

6.2.4.5 Beneficial Conversion Features

The General subsections of ASC 470-20 include requirements for the separate presentation in equity

of BCFs in certain convertible debt instruments (see Chapter 7). As noted in ASC 470-20-15-2, that

guidance does not apply to an equity conversion feature that causes the convertible debt instrument in

which it is embedded to be separated into liability and equity components under the CCF guidance in

ASC 470-20. Accordingly, an issuer should evaluate whether the CCF guidance applies before potentially

considering the BCF guidance. If the CCF guidance in ASC 470-20 applies, the issuer should not analyze

the conversion feature under the BCF guidance.

6.3 Initial Accounting

6.3.1 Separation of Liability and Equity Components

ASC 470-20

25-22 The liability and equity components of a convertible debt instrument within the scope of the Cash

Conversion Subsections shall be accounted for separately. Recognition of a convertible debt instrument within

the scope of the Cash Conversion Subsections is not addressed by paragraph 470-20-25-12.

25-23 The issuer of a convertible debt instrument within the scope of the Cash Conversion Subsections shall do

both of the following:

- First, determine the carrying amount of the liability component in accordance with the guidance in paragraph 470-20-30-27.

- Second, determine the carrying amount of the equity component represented by the embedded conversion option in accordance with the guidance in paragraph 470-20-30-28.

The issuer of a convertible debt instrument within the scope of the CCF guidance in ASC 470-20 is

required to (1) separate the instrument into liability and equity components and (2) allocate the issuance

proceeds and transaction costs that are attributable to the instrument between the two components.

In a manner consistent with the illustrative example in ASC 470-20-55-75, the equity component is

presented within equity as APIC.

To measure the components, the issuer uses a “liability-first” allocation approach as follows:

- Determine the carrying amount of the liability component (before the allocation of any transaction costs) on the basis of the fair value of a hypothetical nonconvertible debt instrument (see Section 6.3.2).

- Determine the carrying amount of the equity component (before allocation of any transaction costs) by using a residual approach — that is, allocate to the equity component the amount of the instrument’s issuance proceeds that remain after allocation to the liability component (see Section 6.3.3).

- Allocate qualifying transaction costs between the liability and equity components in proportion to the allocation of proceeds between each component in steps 1 and 2 (see Section 6.3.4).

If an outstanding convertible debt instrument that is not within the scope of

the CCF guidance is modified so that it becomes subject to

it, the CCF guidance is applied prospectively (see Section

6.5.3.4). If an outstanding debt

instrument with a CCF was not within the scope of the CCF

guidance because the conversion feature was required to be

bifurcated as a derivative instrument under ASC 815-15 and

the instrument subsequently becomes subject to the CCF

guidance because the conversion feature no longer requires

bifurcation under ASC 815-15, the issuer should reclassify

the current carrying amount (fair value) of the conversion

feature to equity and continue to amortize any debt discount

(see ASC 470-20-35-20 and ASC 815-15-35-4 as well as

Section 6.4 of Deloitte’s Roadmap

Contracts on an Entity’s Own

Equity).

6.3.2 Initial Measurement of the Liability Component

6.3.2.1 Hypothetical Nonconvertible Debt

ASC 470-20

30-27 The carrying amount of the liability component shall be determined for purposes of paragraph 470-20-25-23 by measuring the fair value of a similar liability (including any embedded features other than the conversion option) that does not have an associated equity component.

When allocating issuance proceeds between the liability and equity components of convertible debt under the CCF guidance in ASC 470-20, the issuer measures the initial carrying amount of the liability component as the fair value of a hypothetical nonconvertible debt instrument — that is, a comparable liability without an equity component, adjusted for any transaction costs that are allocable to the liability component (see Section 6.3.4). Such a hypothetical nonconvertible debt instrument has terms and features that exactly match those of the actual convertible debt instrument issued except for (1) the conversion feature (i.e., the equity component) and (2) any features that are nonsubstantive at issuance. For instance, the hypothetical nonconvertible debt has the same coupon rate as the convertible debt instrument. Other than the equity conversion feature, the terms of the hypothetical nonconvertible debt include all substantive terms and features of the actual convertible debt (such as any substantive embedded put or call options) embedded in the instrument irrespective of whether they must be bifurcated under ASC 815-15.

The terms of some convertible debt instruments contain exercise contingencies, such as provisions that permit the conversion feature to be exercised if (1) the underlying stock trades above a specified price (e.g., 130 percent of par), (2) the convertible debt trades for an amount below its if-converted value (e.g., 98 percent of its if-converted value), or (3) a fundamental change (e.g., a change of control) occurs. An exercise contingency that solely affects the exercisability of the conversion option should be analyzed as part of the equity conversion feature. Therefore, such a feature would not be part of the terms of the hypothetical nonconvertible debt instrument that is used to measure the liability component’s fair value.

6.3.2.2 Nonsubstantive Features

ASC 470-20

30-29 An embedded feature that is determined to be nonsubstantive at the issuance date shall not affect the

initial measurement of the liability component.

Determining Whether an Embedded Feature Is Nonsubstantive

30-30 Solely for purposes of applying the initial measurement guidance in paragraphs 470-20-30-27 through

30-28 and the subsequent measurement guidance in paragraph 470-20-35-15, an embedded feature other

than the conversion option (including an embedded prepayment option) shall be considered nonsubstantive

if, at issuance, the entity concludes that it is probable that the embedded feature will not be exercised. That

evaluation shall be performed in the context of the convertible debt instrument in its entirety.

The terms of the hypothetical nonconvertible debt used to measure the liability component’s fair value

exclude any feature of the actual convertible debt instrument (e.g., an embedded prepayment, call, or

put option) that is considered nonsubstantive as of the issuance date. The determination of whether

a feature is nonsubstantive is based on an evaluation as of the issuance date of the likelihood that the

feature will not be exercised. To make this assessment, the entity considers all the terms of the actual

convertible debt instrument, including the embedded conversion feature, rather than the terms of the

hypothetical nonconvertible debt. A feature is nonsubstantive if it is probable, at issuance, that it will not

be exercised.

Example 6-6

Put Feature

A convertible debt security has a maturity date that is 20 years from the issuance date and an embedded

put feature that is exercisable at par three months after the issuance date. The issuer concludes that, as

of the issuance date, it is probable that the put feature will not be exercised. Accordingly, the terms of

the hypothetical nonconvertible debt do not incorporate the put feature and it is ignored in the fair value

measurement of the liability component.

The guidance on nonsubstantive features in ASC 470-20 does not exempt such features from the

requirement in ASC 815-15 to evaluate whether they must be bifurcated as embedded derivatives (see

Section 2.3). Thus, an embedded feature in a convertible debt instrument subject to the CCF guidance

in ASC 470-20 may have to be bifurcated as an embedded derivative under ASC 815-15 even if it is

considered nonsubstantive under ASC 470-20. Further, the issuer would separate the embedded

feature from the liability component of the convertible debt even though it would determine the fair

value of that component without taking into account the feature under ASC 470-20.

A provision of a convertible debt instrument within the scope of the CCF guidance in ASC 470-20 might

allow the holder to require the issuer’s repayment of the debt if a change in control occurs. If it is

determined that a change-in-control provision is substantive, the entity should consider the provision

in its initial measurement of the liability component’s fair value and its assessment of the hypothetical

nonconvertible debt’s expected life for use in the amortization of any debt discount and issuance

costs. A change-in-control provision would be considered nonsubstantive if, as of the issuance date,

it was probable that a change-in-control event would not occur or, for other reasons, it was probable

that the feature would not be exercised. In determining whether the change-in-control provision is

nonsubstantive, an entity should assess the convertible debt instrument in its entirety and consider

all relevant terms and provisions (i.e., including the conversion option). The original determination of

whether the change-in-control event is likely to occur should not be reassessed unless the terms of the

debt agreement are modified.

6.3.2.3 Fair Value Measurement

ASC 470-20

55-73 . . . Depending on the terms of the instrument (for example, if the instrument contains prepayment features other than the embedded conversion option) and the availability of inputs to valuation techniques, it may be appropriate to determine the fair value of the liability component using an expected present value technique (an income approach)[,] a valuation technique based on prices and other relevant information generated by market transactions involving comparable liabilities (a market approach) or both an income approach and a market approach.

In measuring the fair value of the liability component on the basis of the terms of hypothetical nonconvertible debt, an entity applies the fair value measurement guidance in ASC 820-10. Under that guidance, the measurement objective is “to estimate the price at which an orderly transaction to . . . transfer the liability would take place between market participants at the measurement date under current market conditions.” As stated in ASC 820-10-35-16AA, to meet this objective, the issuer should “maximize the use of relevant observable inputs and minimize the use of unobservable inputs.” Depending on the terms of the hypothetical nonconvertible debt and the availability of inputs, either an income approach (e.g., the present value of the cash flows of the nonconvertible debt over its expected life discounted by using the issuer’s nonconvertible debt borrowing rate) or a market approach (e.g., using quoted prices for similar nonconvertible debt held by other parties as assets) or both may be appropriate.

6.3.2.4 Application of an Income Approach

ASC 470-20

35-15 Embedded features that are determined to be nonsubstantive at the issuance date shall not affect the expected life of the liability component. Paragraph 470-20-30-30 provides guidance on assessing whether an embedded feature other than the conversion option (including an embedded prepayment option) shall be considered nonsubstantive at issuance for purposes of this paragraph.

If the issuer initially measures the fair value of the hypothetical nonconvertible debt by using an income approach, its estimate of fair value reflects the contractual cash flows through the expected life of the hypothetical nonconvertible debt discounted by using the issuer’s nonconvertible debt borrowing rate.

6.3.2.4.1 Estimating Expected Life

Because the initial and subsequent measurements of the liability component are based on the fair value of a similar liability that does not have an associated equity component (ASC 470-20-30-27 and ASC 470-20-35-13), an entity disregards the conversion option and any other nonsubstantive embedded features in estimating the liability component’s expected life. This is the case even though the conversion option may affect the likelihood that other substantive features would be exercised or triggered. For example, an investor may be less likely to exercise a put option embedded in a debt instrument if its exercise would cause a loss of any intrinsic or time value associated with a conversion option embedded in the same instrument. Nevertheless, when estimating the expected life of the liability component, the issuer should assume that no conversion option exists.

The terms of some conversion options contain exercise contingencies (e.g., holders can only exercise an option if the last reported sales price of the issuer’s common stock is greater than or equal to 130 percent of the conversion price). If an exercise contingency solely affects the exercisability of the conversion option, the contingency should be considered part of the conversion option in the estimation of the hypothetical nonconvertible debt’s expected life. Accordingly, an issuer would not consider such

an exercise contingency when determining the expected life of the convertible debt instrument’s liability

component.

If there is a substantive put feature that holders can exercise at par before the debt’s maturity date,

the expected life of the hypothetical nonconvertible debt is usually shorter than its contractual

term. Such hypothetical debt has the same coupon rate as the convertible debt instrument, which

typically is lower than current market rates for similar nonconvertible debt. Provided that (1) interest

rates are not expected to decrease significantly and (2) no other embedded features (other than the

conversion feature) are sufficiently valuable to induce the investor to continue holding the hypothetical

nonconvertible debt instrument, the investor would be expected to exercise the put option at its first

available opportunity because the coupon rate is below market rates. Accordingly, if hypothetical

nonconvertible debt contains a substantive put feature whose exercise amount is equal to or in excess

of par, the debt’s expected life usually extends only until the earliest date on which the investor can put

the debt to the issuer. (This observation might not be valid, however, if the exercise amount of the put

feature is less than the principal amount of the debt.) Conversely, the existence of a call or prepayment

feature payable at par typically does not affect such debt’s expected life; unless there was a significant

decrease in interest rates, the issuer would not call a debt instrument that was issued at a coupon rate

below market rates.

If a convertible debt instrument contains substantive noncontingent mirror-image put and call options

that are exercisable on the same date and at the same price, it is highly likely that either the put or

call option would be exercised on that date provided that the instrument had not been previously

converted. If the fair value of the liability component is below the exercise price, the holder may be likely

to put the hypothetical nonconvertible debt; and if the fair value of the liability component exceeds the

exercise price, the issuer may be likely to call the hypothetical nonconvertible debt. In this case, the

expected life does not extend beyond the exercise date of the put and call options.

The existence of nonsubstantive features (see Section 6.3.2.2) does not affect the issuer’s estimate

of the expected life. For example, a put option that is only exercisable upon a fundamental change

would not affect the expected life of the liability component if the issuer, as of the issuance date,

concludes that it is probable that such a fundamental change will not occur. An embedded feature is

nonsubstantive if, at issuance, it is probable that it will not be exercised (see ASC 470-20-30-30).

6.3.2.4.2 Estimating Nonconvertible Debt Borrowing Rate

The nonconvertible debt borrowing rate is the interest rate the issuer would have to pay on the

hypothetical nonconvertible debt. Typically, entities do not have outstanding publicly traded or recently

issued nonconvertible debt with terms that are identical to those of the hypothetical instrument.

Therefore, they might need to determine the market interest rate that currently could reasonably

be expected for such an instrument. Two common approaches are to calculate the hypothetical

nonconvertible debt’s interest rate on the basis of (1) similar outstanding debt issued by the entity or

(2) similar debt issued by other similar entities.

If the entity determines that it is appropriate to consider the current market rates on its outstanding

debt (e.g., term loans or lines of credit) to calculate the interest rate of the hypothetical nonconvertible

debt instrument, it should consider (1) any differences between such debt and the hypothetical

nonconvertible debt (e.g., call or put options, or the level of seniority) and (2) market changes (e.g.,

interest rate changes or changes in the entities’ credit ratings) after the issuance of such debt. If any

differences exist, the entity must appropriately adjust the debt’s interest rate.

Alternatively, an entity may estimate the borrowing rate of the hypothetical debt by referring to the current market interest rates for similar debt issued by other similar entities. To be considered similar, those other entities must have, for example, comparable credit ratings and access to the market in which the entity’s own debt was issued. The entity should also consider differences in the other entities’ credit spreads and general access to debt that arise from being in different industry sectors. If any differences exist, the entity must appropriately adjust the other entities’ borrowing rate to determine the market interest rate for the hypothetical nonconvertible debt instrument.

If an entity purchases a call option on its own equity concurrently with issuing convertible debt that is within the scope of the CCF guidance, the option’s fair value may provide relevant information for determining the nonconvertible debt borrowing rate that is used under an income approach to estimate the liability component’s fair value. Paragraph B9 of FSP APB 14-1 states, in part:

[C]onvertible debt instruments issued in the United States often contain contingent interest provisions that enable the issuer to receive an income tax deduction based on its nonconvertible debt borrowing rate. Some entities purchase call options on their own stock concurrently with the issuance of convertible debt, and the two instruments are integrated for tax purposes, resulting in a tax deduction that may be similar to their nonconvertible debt borrowing rate. Consequently, many issuers of convertible debt instruments within the scope of [the CCF guidance] are obtaining some of the information that may be used to estimate the fair value of the liability component in order to adequately support deductions taken on their U.S. federal income tax returns.

6.3.3 Initial Measurement of the Equity Component

ASC 470-20

30-28 The carrying amount of the equity component represented by the embedded conversion option shall be determined for purposes of paragraph 470-20-25-23 by deducting the fair value of the liability component from the initial proceeds ascribed to the convertible debt instrument as a whole.

In the allocation of proceeds between the liability and equity components of a convertible instrument within the scope of the CCF guidance in ASC 470-20, the equity component is not measured directly but instead represents a residual amount that is determined by deducting (1) the amount allocated to the liability component from (2) the initial proceeds attributable to the convertible debt (see Section 6.3.5). As noted in paragraph B8 of FSP APB 14-1 (which quotes paragraph BC30 of IAS 32), this approach “removes the need to estimate inputs to, and apply, complex option pricing models to measure the equity component.” Further, an adjustment is made to the initial carrying amount for any transaction costs allocable to the equity component (see Section 6.3.4).

If an issuer of convertible debt purchases a call option on its own equity concurrently with the issuance of the convertible debt, the issuer cannot assume that the initial measurement of the equity component under the CCF guidance in ASC 470-20 would equal the fair value of the purchased call option. For instance, the fair value of the purchased option may differ from the amount of the proceeds allocable to the equity component because of (1) market pricing inefficiencies, (2) differences in the creditworthiness of the counterparties to the debt and the purchased call option, or (3) differences in terms or other features included in the debt and the purchased call option. Notwithstanding these differences, the call option’s fair value may be an input into the determination of the liability component’s fair value (see Section 6.3.2.4.2).

6.3.4 Transaction Costs

ASC 470-20

25-26 Transaction costs incurred with third parties other than the investor(s) and that directly relate to the

issuance of convertible debt instruments within the scope of the Cash Conversion Subsections shall be

allocated to the liability and equity components in accordance with the guidance in paragraph 470-20-30-31.

30-31 Transaction costs required to be allocated to the liability and equity components by paragraph 470-20-25-26 shall be allocated in proportion to the allocation of proceeds and accounted for as debt issuance costs

and equity issuance costs, respectively.

Third-party costs that are directly related to the issuance of a convertible instrument within the scope

of the CCF guidance are allocated to the liability and equity components in the same proportion as the

proceeds allocation. Such transaction costs are limited to specific incremental costs that are directly

attributable to issuing the convertible debt (see Section 3.5.3.1).

Accordingly, an issuer determines the amount of proceeds that should be allocated to the liability

and equity components before allocating any transaction costs. For instance, if 80 percent of the

issuance proceeds are allocated to the liability component and the remaining 20 percent to the equity

component, 80 percent of the transaction costs would be allocated to the liability component and 20

percent to the equity component.

Transaction costs allocated to the liability component are accounted for as debt issuance costs in

accordance with ASC 835-30. Under ASC 835-30-45-1A, such costs are reported on the balance sheet as

a direct deduction from the carrying amount of the liability component rather than as a deferred charge

upon issuance of the debt.

Transaction costs allocated to the equity component are recognized in APIC as equity issuance costs.

Such costs are charged against the proceeds allocated to the equity component; that is, transaction

costs allocated to the equity component are deducted from the amount of proceeds allocated to the

equity component, and the net amount is recorded in equity.

6.3.5 Multiple-Element Transactions

ASC 470-20

25-24 If the issuance transaction for a convertible debt instrument within the scope of the Cash Conversion

Subsections includes other unstated (or stated) rights or privileges in addition to the convertible debt

instrument, a portion of the initial proceeds shall be attributed to those rights and privileges based on the

guidance in other applicable U.S. generally accepted accounting principles (GAAP).

Sometimes, a convertible debt instrument is issued in a transaction that includes elements not

attributable to the debt (e.g., other freestanding financial instruments; see Section 3.4). If the issuance

of a convertible instrument within the scope of the CCF guidance in ASC 470-20 includes other rights

or privileges, the issuer is required to allocate part of the initial proceeds related to those rights and

privileges in a manner consistent with the guidance in ASC 835-30-25-6 before allocating proceeds and

transaction costs to the liability and equity components. In these circumstances, the entity might also

need to allocate a portion of the transaction costs to the other instruments or rights and privileges that

are separately recognized.

6.3.6 Embedded Derivatives

ASC 815-15

55-76A The following steps specify how an issuer shall apply the guidance on accounting for embedded derivatives in this Subtopic to a convertible debt instrument within the scope of the Cash Conversion Subsections of Subtopic 470-20.

- Step 1. Identify embedded features other than the embedded conversion option that must be evaluated under Subtopic 815-15.

- Step 2. Apply the guidance in Subtopic 815-15 to determine whether any of the embedded features identified in Step 1 must be separately accounted for as derivative instruments. Paragraph 470-20-15-4 states that the guidance for a convertible debt instrument within the scope of the Cash Conversion Subsections of Subtopic 470-20 does not affect an issuer’s determination of whether an embedded feature shall be separately accounted for as a derivative instrument.

- Step 3. Apply the guidance in paragraph 470-20-25-23 to separate the liability component (including any embedded features other than the conversion option) from the equity component.

- Step 4. If one or more embedded features are required to be separately accounted for as a derivative instrument based on the analysis performed in Step 2, that embedded derivative shall be separated from the liability component in accordance with the guidance in this Subtopic. Separation of an embedded derivative from the liability component would not affect the accounting for the equity component.

If any feature other than the conversion feature is required to be bifurcated as an embedded derivative (e.g., an embedded put or call option), it is treated as part of the liability component in the separation of the liability and equity components under the CCF guidance in ASC 470-20. After separation of the liability component, the embedded derivative is bifurcated from the liability component at its fair value and has no effect on the accounting for the equity component. The portion of the amount attributable to the liability component that remains after bifurcation of the embedded derivative is allocated to the host liability component.

As indicated in ASC 470-20-15-4, the CCF guidance in ASC 470-20 does not affect the determination of whether an embedded feature should be separated and accounted for as a derivative instrument. Therefore, when evaluating whether any embedded feature other than the conversion option must be bifurcated from the convertible instrument, the issuer should not consider the separation of the equity component as having created a discount to the liability component under the CCF guidance in ASC 470-20. A discount could, however, be created from the allocation of proceeds to other separately recognized freestanding financial instruments issued in conjunction with a convertible debt instrument. For example, a discount created by the separation of an equity component under ASC 470-20 would not be treated as a discount in the evaluation of whether debt with an embedded put or call feature involves a substantial premium or discount under ASC 815-15-25-40 and ASC 815-15-25-42. Further, an entity would evaluate whether an embedded feature must be bifurcated under ASC 815-15 even if it is considered nonsubstantive under the CCF guidance in ASC 470-20.

6.3.7 Deferred Taxes

ASC 470-20

25-27 Recognizing convertible debt instruments within the scope of the Cash Conversion Subsections as two separate components — a debt component and an equity component — may result in a basis difference associated with the liability component that represents a temporary difference for purposes of applying Subtopic 740-10. The initial recognition of deferred taxes for the tax effect of that temporary difference shall be recorded as an adjustment to additional paid-in capital.

Depending on the applicable taxation requirements, the separation of an equity component under

ASC 470-20 often causes the carrying amount of the liability component under GAAP (the book basis) to

be different from the tax basis of the debt determined in accordance with ASC 740-10. In practice, such

basis differences usually result in the recognition of a deferred tax liability under ASC 740-10 upon the

issuance of an instrument within the scope of the CCF guidance in ASC 470-20 because the tax basis

exceeds the book basis after the separation of an equity component under ASC 470-20.

Paragraph B13 of FSP APB 14-1 states, in part:

In some jurisdictions, the tax basis of a convertible debt instrument at initial recognition includes the entire

amount of the proceeds received at issuance. As a result, a taxable temporary difference arises from the initial

recognition of the equity component separately from the liability component. The Board decided that the

initial recognition of deferred taxes for the tax effect of the temporary difference should be recorded as an

adjustment to additional paid-in capital. That treatment is consistent with the [guidance on convertible debt

with a beneficial conversion feature in ASC 740-10-55-51].

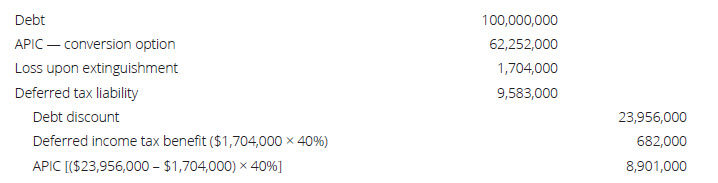

Example 6-7

Deferred Taxes on Debt With a CCF

A convertible debt instrument within the scope of the CCF guidance was issued

for proceeds of $100. The tax basis of the debt

under the applicable taxation requirements is the

original issue price adjusted for any original

issue discount or premium before any separation of

an equity component for accounting purposes (i.e.,

the tax basis is $100). However, because of the

application of the CCF guidance in ASC 470-20, the

debt’s book basis (i.e., the carrying amount of

the liability component) is $80 after separation

of an equity component. If the issuer’s tax rate

is 21 percent, it will recognize a deferred tax

liability under ASC 740-10 of $4, or ($100 – $80)

× 21%.

Because the separation of the equity component from the debt creates the basis difference in the debt, the

establishment of a deferred tax liability for the basis difference results in a charge to the related components

of shareholders’ equity (see ASC 740-20-45-11(c)). Thus, ASC 470-20-25-27 requires entities to record the

recognition of deferred taxes as an adjustment to APIC, and the initial accounting entries are as follows:

For financial reporting purposes, interest expense in subsequent periods includes a noncash component that

reflects the amortization of the debt discount created by the separation of the equity component. This noncash

component of reported interest expense is not deductible for U.S. income tax purposes. As interest expense

is recognized for the liability component after initial recognition, the deferred tax liability is reduced and a

deferred tax benefit is recognized in earnings through the amortization of the debt discount.

6.4 Subsequent Accounting

6.4.1 Liability Component

ASC 470-20

35-12 The excess of the principal amount of a liability component recognized in accordance with paragraph

470-20-25-23 over its carrying amount shall be amortized to interest cost using the interest method as

described in paragraphs 835-30-35-2 through 35-4.

35-13 For purposes of applying the interest method to a convertible debt instrument within the scope of the Cash Conversion Subsections, debt discounts and debt issuance costs shall be amortized over the expected life of a similar liability that does not have an associated equity component (considering the effects of embedded features other than the conversion option).

35-14 If, under Subtopic 820-10, an issuer uses a valuation technique consistent with an income approach to measure the fair value of the liability component at initial recognition, the issuer shall consider the periods of cash flows used in the fair value measurement when determining the appropriate discount amortization period.

35-16 The expected life of the liability component shall not be reassessed in subsequent periods unless the terms of the instrument are modified. Therefore, the reported interest cost for an instrument within the scope of the Cash Conversion Subsections shall be determined based on its stated interest rate once the debt discount has been fully amortized.

After initial recognition, the issuer measures the liability component of convertible debt subject to the CCF guidance in ASC 470-20 at amortized cost by applying the interest method in ASC 835. This means that the excess of the principal amount to be repaid at the end of the expected life of a similar hypothetical nonconvertible debt over the initial carrying amount of the liability component is treated as a debt discount. As indicated in ASC 835-30-35-2, under the interest method, the amortization of the debt discount is computed “in such a way as to result in a constant rate of interest when applied to the amount outstanding at the beginning of any given period.”

The issuer amortizes the debt discount and any transaction costs allocated to the liability component (i.e., the debt issuance costs) by using the interest method over the expected life of a similar hypothetical nonconvertible debt instrument. It determines the expected life by considering all substantive terms and features (e.g., substantive puts or calls) of the convertible debt other than the conversion feature (see Section 6.3.2.4.1). The amortization period is not subsequently reassessed unless the terms of the instrument are modified.

The periodic amortization of the debt discount and any debt issuance costs adds a noncash component to interest expense that reflects the difference between the cash coupon rate on the convertible debt and the effective interest rate on the liability component. Paragraph B14 of FSP APB 14-1 notes that this “treatment is consistent with the objective that an issuer’s reported interest cost from convertible debt instruments within the scope of [the CCF guidance in ASC 470-20] should reflect its nonconvertible debt borrowing rate” (see Section 6.1.2).

If the issuer determines the initial fair value of the liability component by using an income approach (e.g., discounted cash flows), it estimates that fair value on the basis of contractual cash flows of a similar hypothetical nonconvertible debt instrument over its expected life. In this circumstance, the entity uses the same expected-life assumption in determining the appropriate amortization period for the debt discount and any associated debt issuance costs after initial recognition.

The method of determining the amortization period over the liability component’s expected term is unique to instruments within the scope of the CCF guidance in ASC 470-20. For instruments outside the scope of the CCF guidance, the amortization period is usually the contractual life or the earliest noncontingent put date unless special requirements apply. Paragraph B15 of FSP APB 14-1 states, in

part:

The Board is aware that for debt instruments containing prepayment features, different accounting policies

have been applied in practice for purposes of estimating the amortization period for discounts, premiums,

and deferred transaction costs under [ASC 835-30]. The guidance [in the Cash Conversion subsections of

ASC 470-20] on determining an appropriate discount amortization period is not intended to be a broad-based

interpretation applicable to debt instruments that are not within the scope of [this guidance].

6.4.2 Equity Component

ASC 470-20

35-17 The equity component (conversion option) shall not be remeasured as long as it continues to meet

Subtopic 815-40’s conditions for equity classification.

35-18 A reclassification of the equity component (conversion option) would not affect the accounting for the

liability component.

35-19 If Subtopic 815-40 requires the conversion option to be reclassified from stockholders’ equity to

a liability measured at fair value (see the guidance beginning in paragraph 815-40-35-8), the difference

between the amount previously recognized in equity and the fair value of the conversion option at the date of

reclassification shall be accounted for as an adjustment to stockholders’ equity.

35-20 If Subtopic 815-40 requires that a conversion option that was previously reclassified from stockholders’

equity be subsequently reclassified back into stockholders’ equity, gains or losses recorded to account for the

conversion option at fair value during the period it was classified as a liability shall not be reversed.

After initial recognition, the issuer does not remeasure the equity component of convertible debt

subject to the CCF guidance in ASC 470-20 unless the conversion feature no longer meets the equity

classification conditions in ASC 815-40. In a manner consistent with the guidance in ASC 815-40-35-8,

the issuer reassesses the classification of the equity component of a convertible debt instrument

accounted for under the CCF guidance in ASC 470-20 as of each balance sheet date. If an event causes a

change in the required classification, the contract is reclassified as of the date of the event.

If the conversion feature no longer meets the equity classification conditions in ASC 815-40 (e.g.,

because the issuer has voluntarily issued equity shares so that it no longer has a sufficient number of

authorized and unissued shares to settle the convertible debt in shares upon conversion), the issuer

reclassifies the previously recognized equity component as a liability. The liability and equity components

of the convertible debt instrument are not recombined; instead, the liability component and the

conversion feature continue to be treated as two separate units of account. The entity continues to

accrete the liability component and accounts for the previously recognized equity-classified conversion

feature as a liability at fair value, with changes in fair value recognized in earnings under ASC 815-40, as

long as the feature does not meet the equity classification conditions in ASC 815-40.

An issuer would not reclassify the equity component as a liability merely because it has decided to settle

the instrument in cash upon conversion (or has a history of cash settlements of similar contracts) as

long as the conversion feature continues to meet the criteria for equity classification in ASC 815-40 (e.g.,

the issuer could not be forced to cash settle the feature upon conversion).

Connecting the Dots

For a discussion of the application of ASC 815-40, see Deloitte’s Roadmap

Contracts on an

Entity’s Own Equity.

See Section 2.6 for discussion of the requirement for SEC registrants to classify the equity component in temporary equity.

6.5 Derecognition

6.5.1 General Approach

ASC 470-20

40-19 If an instrument within the scope of the Cash Conversion Subsections is derecognized, an issuer shall allocate the consideration transferred and transaction costs incurred to the extinguishment of the liability component and the reacquisition of the equity component.

40-20 Regardless of the form of consideration transferred at settlement, which may include cash (or other assets), equity shares, or any combination thereof, that allocation shall be performed as follows:

- Measure the fair value of the consideration transferred to the holder. If the transaction is a modification or exchange that results in derecognition of the original instrument, measure the new instrument at fair value (including both the liability and equity components if the new instrument is also within the scope of the Cash Conversion Subsections).

- Allocate the fair value of the consideration transferred to the holder between the liability and equity components of the original instrument as follows:

- Allocate a portion of the settlement consideration to the extinguishment of the liability component equal to the fair value of that component immediately before extinguishment.

- Recognize in the statement of financial performance as a gain or loss on debt extinguishment any difference between (i) and (ii):

- The consideration attributed to the liability component.

- The sum of both of the following:01. The net carrying amount of the liability component02. Any unamortized debt issuance costs.

- Allocate the remaining settlement consideration to the reacquisition of the equity component and recognize that amount as a reduction of stockholders’ equity.

40-21 If the derecognition transaction includes other unstated (or stated) rights or privileges in addition to the settlement of the convertible debt instrument, a portion of the settlement consideration shall be attributed to those rights and privileges based on the guidance in other applicable U.S. GAAP.

40-22 Transaction costs incurred with third parties other than the investor(s) that directly relate to the settlement of a convertible debt instrument within the scope of the Cash Conversion Subsections shall be allocated to the liability and equity components in proportion to the allocation of consideration transferred at settlement and accounted for as debt extinguishment costs and equity reacquisition costs, respectively.

When an instrument within the scope of the CCF guidance is derecognized (e.g., because it is converted or otherwise settled), the transaction is accounted for as an extinguishment of the liability component (a debt extinguishment) and the reacquisition of the equity component (an equity transaction) irrespective of the form of settlement (e.g., cash or shares or a combination of both). Transactions that could cause an instrument within the scope of the CCF guidance in ASC 470-20 to be derecognized include those in which the issuer is relieved of its obligations through:

- The conversion of the instrument in accordance with its contractual terms.

- A settlement of the convertible debt instrument in which cash is paid to the creditor (e.g., the exercise of an embedded call or put option), which results in the expiration of the conversion feature in accordance with the contractual terms.

- The reacquisition of the convertible debt instrument before its maturity (e.g., in an open-market repurchase of outstanding convertible debt) irrespective of whether the instrument is cancelled or held in treasury.

- A modification of the instrument’s contractual terms if the modification is treated as an extinguishment under ASC 470-50.

- An exchange of the instrument for another instrument if the exchange is treated as an extinguishment under ASC 470-50.

Upon derecognition of the instrument, the fair value of the consideration transferred to the holders

(e.g., cash, other assets, equity shares, services, or a combination thereof) is allocated between the two

components by using the same method as that for allocating the original issuance proceeds between

the two components irrespective of whether the issuer transfers cash, shares, or a combination of cash

and shares upon conversion. The portion of the consideration allocated to the extinguishment of the

liability component is equal to the fair value of that component immediately before conversion. The

amount of consideration that remains is allocated to the reacquisition of the equity component. No gain

or loss is recognized for the amount allocated to the equity component. (ASC 260-10-S99-2 does not

apply to the settlement of the equity component.)

Third-party transaction costs that are directly related to the settlement are allocated to the liability

component as debt extinguishment costs in proportion to the allocation of consideration transferred

to the liability component at settlement. The remaining third-party transaction costs that are directly

related to the settlement are treated as equity reacquisition costs.

Any difference between (1) the amount of settlement consideration plus the costs allocated

to the liability component and (2) the liability component’s net carrying amount (including any

remaining unamortized discount and debt issuance costs) is recognized as a gain or loss upon debt

extinguishment. Accordingly, the settlement of a convertible debt instrument subject to the CCF

guidance in ASC 470-20 typically results in a gain or loss upon extinguishment.

6.5.2 Induced Conversions

ASC 470-20

40-26 An entity may amend the terms of an instrument within the scope of the Cash Conversion Subsections to

induce early conversion, for example, by offering a more favorable conversion ratio or paying other additional

consideration in the event of conversion before a specified date. In those circumstances, the entity shall

recognize a loss equal to the fair value of all securities and other consideration transferred in the transaction

in excess of the fair value of consideration issuable in accordance with the original conversion terms. The

settlement accounting (derecognition) treatment described in paragraph 470-20-40-20 is then applied using

the fair value of the consideration that was issuable in accordance with the original conversion terms. The

guidance in this paragraph does not apply to derecognition transactions in which the holder does not exercise

the embedded conversion option.

To induce conversion of convertible debt instruments before a specified date (see Section 4.5.4),

issuers sometimes change the conversion terms (e.g., reduce the conversion price) or give the holders

additional consideration (e.g., cash, equity shares, warrants, other securities).

The wording of the scope guidance on induced conversions of

convertible debt within the scope of the CCF guidance differs from that on

induced conversions of traditional convertible debt (see Section 4.5.4.1). ASC

470-20-40-14 specifies that the induced conversion guidance on traditional

convertible debt applies to an exchange of a convertible debt instrument for

shares, even if the exchange does not involve the legal exercise of the

contractual conversion privileges included in the terms of the debt. However,

ASC 470-20-40-26 notes that the induced conversion guidance on convertible debt

within the scope of the CCF guidance does not apply to derecognition

transactions in which the holder does not exercise the embedded conversion

option. An entity should consider its specific facts and circumstances and the

substance of the transaction in evaluating whether an exchange that does not

involve the legal exercise of contractual conversion privileges should be

accounted for as an induced conversion under ASC 470-20-40-26.

If a holder exercises its option in an induced conversion of a debt instrument within the scope of the CCF guidance in ASC 470-20, the issuer would apply the following two-step model to account for the conversion:

- Step 1 — Determine the amount of the inducement expense. Recognize a loss (an inducement expense) equal to the excess of (1) the fair value of the consideration transferred over (2) the fair value of the consideration that would have been issuable under the original conversion terms. In a manner consistent with the guidance in ASC 470-20-40-16, fair value is determined as of the date the inducement offer is accepted by the convertible debt holder (such as the conversion date or the date the holder enters into a binding agreement to convert, as applicable; see Section 4.5.4 for further discussion).

- Step 2 — Determine the amount of any debt extinguishment gain or loss. Allocate the fair value of consideration issuable under the original terms between (1) the extinguishment of the liability component and (2) the reacquisition of the original instrument’s equity component in accordance with ASC 470-20-40-20. The fair value of the liability component is allocated to the liability component and compared with the net carrying amount of the liability component in the determination of a gain or loss upon debt extinguishment. Any remaining amount of the fair value of consideration issuable under the original terms is allocated to the equity component. Said differently, the issuer applies the derecognition guidance in ASC 470-20-40-20 by using the fair value of the consideration that was issuable under the original conversion terms rather than the fair value of the consideration actually transferred to the holder.