Chapter 9 — Lessor Accounting

Chapter 9 — Lessor Accounting

9.1 Overview

ASC 842-30

05-1 This Subtopic addresses accounting

by lessors for leases that have been classified as sales-type leases, direct

financing leases, or operating leases in accordance with the requirements in

Subtopic 842-10. Lessors should follow the requirements in this Subtopic as well

as those in Subtopic 842-10.

15-1 This Subtopic follows the same

Scope and Scope Exceptions as outlined in the Overall Subtopic; see Section

842-10-15.

This chapter discusses the different steps in a lessor’s accounting for

leases. Specifically, Section

9.2 discusses classification of the various lease types and Section 9.3 addresses recognition and

measurement considerations related to each of these classifications. Section 9.4 covers other lessor

reporting issues. Section 9.5

covers leveraged leases.

As discussed in Chapter

1, the primary objective of the Board’s leasing project was to require

presentation of the lessee’s off-balance-sheet liabilities. However, a common misconception

is that lessor accounting has not changed much under ASC 842. Specific improvements the

Board made to lessor accounting include those to align ASC 842 with (1) enhancements made to

its revenue standard, ASU

2014-09 (codified as ASC 606), and (2) updates to key terms related to

lessee accounting.

Regarding the alignment with the revenue standard, because lessors’

adoption of ASC 842 was after their adoption of ASC 606, preparers need to establish the

timing of changes and how such changes should be reflected. Further, both the revenue and

lease models now underscore the principle of control transfer rather than the transfer of

risks and rewards, the latter of which was the principle under ASC 605 and ASC 840.

Although lease classification for lessees under ASC 842 is similar to that

for lessors, it is not fully symmetrical. For instance, there are two classes of leases for

a lessee and three for a lessor. In addition, because of the amendments made by

ASU 2021-05 (see

Section 9.2.1.6 for more

information), the existence of variable lease payments in a lease sometimes could influence

classification for a lessor.

We recommend supplementing a review of this section of the Roadmap with a

review of the following chapters:

-

Chapter 2, which discusses how to identify whether an arrangement is within the scope of the leasing standard.

-

Chapter 3, which discusses whether an arrangement is, or contains, a lease.

-

Chapter 4, which discusses how to identify the separate lease components and nonlease components within a contract and how the consideration is allocated to components.

-

Chapter 5, which discusses the term over which a lessor recognizes consideration related to the lease component.

-

Chapter 6, which discusses the initial and subsequent measurement of consideration that must be allocated to the components identified.

In July 2018, the FASB issued ASU 2018-11, which contains a new practical

expedient in ASC 842-10-15-42A under which lessors can elect, by class of underlying asset,

not to separate lease and nonlease components if certain criteria are met. See Section 4.3.3.2 for further details

about the practical expedient related to a lessor’s separation of lease and nonlease

components.

Lessors that do not elect the practical expedient must allocate

consideration in the contract to the separate lease and nonlease components on a relative

stand-alone selling price basis in a manner consistent with ASC 606. This chapter focuses on

the accounting for the lease component and presumes that the lessor has already applied the

provisions (separation and allocation) discussed in Chapter

4.

In accounting for leases, it is important for an entity to determine

whether a lessor is combining or separating lease and nonlease components. There are many

differences between the accounting for a lease component under ASC 842 and that for a

nonlease component under another Codification topic (e.g., differences related to the

treatment of variable lease payments).

Connecting the Dots

Variable Consideration

While there are conceptual consistencies between ASC 606 and ASC 842,

principally with respect to their reliance on control transfer, the two standards

sometimes differ in their recognition and measurement principles. For example, under ASC

606, variable payments are estimated and included in the transaction price subject to a

constraint; under ASC 842, however, variable lease payments not linked to an index or

rate are generally excluded from the determination of a lessor’s lease receivable.

Variable consideration may be allocated in a contract to a lease component (recognition

governed by ASC 842) and a nonlease component (recognition most likely governed by ASC

606 — see below). In paragraph BC163 of ASU

2016-02, the FASB addresses its decisions regarding the differences

between accounting for variable payments under ASC 842 and accounting for variable

consideration under ASC 606:

The Board decided that providing guidance on consideration in the

contract was necessary to ensure consistent application of the allocation guidance

in Topic 842, particularly for lessors because of the differences between how the

Board decided a lessor should account for variable lease payments and how an entity

accounts for variable consideration in Topic 606. The Board concluded that

accounting for a variable payment that relates partially to a lease component (for

example, a performance bonus that relates to the leased asset and the lessor’s

operation of that asset) in the same manner as a variable lease payment (that is,

with respect to recognition and measurement) will be less costly and complex than

accounting for that variable payment in accordance with the variable consideration

guidance in Topic 606.

Because an entity may be permitted to recognize revenues under ASC 606

earlier than revenues generated from lease components, it is critical to determine the

allocation of the consideration to the appropriate component. See Section 4.4.2.2.1 for more

information.

9.2 Lease Classification

ASC 842-10

25-1 An entity shall classify each separate lease component at the commencement date. An entity shall not reassess the lease classification after the commencement date unless the contract is modified and the modification is not accounted for as a separate contract in accordance with paragraph 842-10-25-8. . . .

|

The five criteria that a lessor uses to

determine whether a lease is a sales-type lease are the same

as those that a lessee uses to establish whether a lease is

a finance lease. If none of those criteria are met, the

lessor evaluates whether the lease is a direct financing

lease; two criteria must be met for the lease to be

considered a direct financing lease. If neither the

sales-type lease criteria nor the direct financing lease

criteria are met, the lease is an operating lease. In

addition, because of the amendments in ASU 2021-05, even a

lease that meets one of the five criteria to be a sales-type

lease (or is classified as a direct financing lease) should

be classified as an operating lease when the lessor would

have recognized a selling loss and the arrangement includes

variable lease payments that do not depend on an index or a

rate. A lessor performs its lease classification assessment

at lease commencement (i.e., when the lessee obtains the

right to use the asset).

|

The decision tree below illustrates the lessor’s classification assessment as well as the criteria that must be met for each type of lease.

Changing Lanes

Classification Date

Unlike ASC 842, ASC 840 required entities to classify leases on the basis of the

facts and circumstances present at lease inception (i.e., the date of the

lease agreement or commitment, if earlier) instead of at lease commencement

(the date on which the lessor makes an underlying asset available to the

lessee). For many entities, there typically is not a significant lag between

lease inception and lease commencement; however, in certain circumstances,

the two dates significantly differ. In such cases, a lessor could

theoretically arrive at different conclusions if facts and circumstances

change between the dates (e.g., the fair value of the underlying asset or

the rate implicit in the lease). The diagram below illustrates the

difference between lease inception and lease commencement.

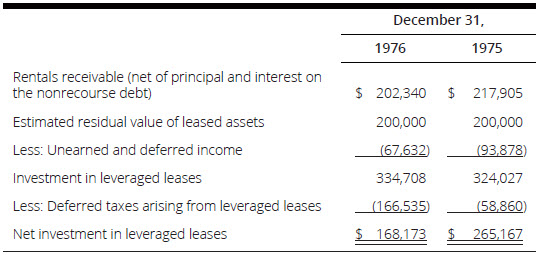

Leveraged Leases

ASC 840 addressed a fourth type of lease, a leveraged lease.

Leveraged lease accounting was a special type of accounting that a lessor

employed for certain direct financing leases. Special accounting was

required for a leveraged lease because of the unique economic effect on the

lessor. This unique economic effect stemmed from a combination of

nonrecourse financing and a cash flow pattern that typically enabled the

lessor to recover its investment in the early years of the lease (as a

result of tax benefits generated by depreciation, interest, and ITC

deductions) and subsequently afforded it the temporary use of funds from

which additional income could be derived.

The FASB did not include leveraged leases in the guidance in

ASC 842 on lease classification. In the Background Information and Basis for

Conclusions of ASU 2016-02, the FASB addresses why it decided not to retain

leveraged leases in the new leasing model, indicating that some Board

members objected to the net presentation related to leveraged leases and

others believed that the accounting for such leases was too complex.

However, the Board decided to grandfather in existing leveraged leases given

that “there would be significant complexities relating to unwinding existing

leveraged leases” during transition. Therefore, a lessor must continue to

apply the accounting in ASC 840 for such a lease (as carried forward in ASC

842) and classify the lease as a leveraged lease provided that it enters

into the lease before the effective date of ASC 842. See Section 9.5 for more

information about how to account for grandfathered leveraged leases.

Bridging the GAAP

IFRS 16 Does Not Distinguish Between

Sales-Type and Direct Financing Leases

Unlike ASC 842, IFRS 16 does not differentiate sales-type

leases from direct financing leases. Rather, lessors account for leases as

either operating or finance leases. See Appendix B for a summary of the

differences between ASC 842 and IFRS 16.

9.2.1 Sales-Type Lease

In a sales-type lease, the lessor transfers control of the underlying asset to

the lessee. In paragraph BC93 of ASU 2016-02, the FASB acknowledges that “[e]ven

though a sales-type lease is not necessarily identical to a sale, the

transactions are economically similar (for example, because sales-type lessors

often use leasing as an alternative means to sell their assets and have no

intention of reusing or re-leasing assets leased under a sales-type lease).”

Paragraph BC93 of ASU 2016-02 further points out that the hallmark of a

sales-type lease is the recognition of “selling profit at lease commencement”

and that such recognition “is consistent with the principle of a sale in Topics

606 and 610.”

Changing Lanes

Sales-Type Leases Affected by Shift From Risks-and-Rewards Model to

Control Model

A sales-type lease results in the recognition of profit (or loss). Therefore, to

be consistent with ASC 606, the FASB decided to align the

transfer-of-control notion, as it applies to the evaluation of whether a

lease qualifies as a sales-type lease, with that in ASC 606. In

paragraph BC121 of ASU 2014-09, the Board observes:

[T]he assessment of when control has transferred

could be applied from the perspective of either the entity

selling the good or service or the customer purchasing the good

or service. Consequently, revenue could be recognized when the

seller surrenders control of a good or service or when the

customer obtains control of that good or service. Although in

many cases both perspectives lead to the same result, the Boards

decided that control should be assessed primarily from the

perspective of the customer. That perspective minimizes the risk

of an entity recognizing revenue from undertaking activities

that do not coincide with the transfer of goods or services to

the customer.

The evaluation of whether a lease qualifies as a sales-type lease therefore focuses on whether

the lessee effectively obtains control of the entire underlying asset (i.e., and not just the right

to use it) rather than whether the lessor has relinquished control. Accordingly, an arrangement

that a lessor historically classified as a sales-type lease because it transferred a portion of the

risks and rewards of the underlying asset to the lessee and a portion to a third party through

a residual value guarantee (e.g., residual value insurance) may no longer qualify as a sales-type

lease.

ASC 842-10

25-2 [A] lessor shall classify a lease as a sales-type lease when the lease meets any of the following criteria at lease commencement:

- The lease transfers ownership of the underlying asset to the lessee by the end of the lease term.

- The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

- The lease term is for the major part of the remaining economic life of the underlying asset. However, if the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for purposes of classifying the lease.

- The present value of the sum of the lease payments and any residual value guaranteed by the lessee that is not already reflected in the lease payments in accordance with paragraph 842-10-30-5(f) equals or exceeds substantially all of the fair value of the underlying asset.

- The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term.

25-3A Notwithstanding the

requirements in paragraphs 842-10-25-2 through 25-3, a

lessor shall classify a lease with variable lease

payments that do not depend on an index or a rate as an

operating lease at lease commencement if classifying the

lease as a sales-type lease or a direct financing lease

would result in the recognition of a selling loss.

25-7 See paragraphs 842-10-55-2 through 55-15 for implementation guidance on lease classification.

The criteria in ASC 842-10-25-2 for a lessor’s sales-type lease classification

are identical to the criteria lessees use to identify a finance lease. (See

Section 8.1 for

a discussion of the lessee’s classification.) Therefore, the lessee’s

classification will often be similar to the lessor’s; however, as further

discussed below, there are differences between the two, such as leases with a

day 1 selling loss for the lessor or differences in the assumptions (e.g.,

residual asset value) or discount rate used (rate implicit in the lease for the

lessor and the incremental borrowing rate for the lessee).

Connecting the Dots

Sales-Type Leases for Real

Estate

Because a lease may qualify as a sales-type lease

without a title transfer under ASC 842, more leases will qualify for

sales-type classification. ASC 842 does not distinguish between the

accounting for real estate and that for non–real estate. In paragraph

BC99 of ASU 2016-02, the FASB states, in part:

Previous GAAP included different lessor

requirements for leases of real estate (for example, a lease of

real estate could only be a sales-type lease if it transferred

title to the real estate to the lessee by the end of the lease

term) because the revenue requirements in previous GAAP for the

sale of real estate differed from the revenue requirements in

previous GAAP applicable to the sale of other assets. The

creation of Topic 606 eliminated those different revenue

accounting requirements; therefore, there is no longer a reason

for the accounting for leases of real estate to differ from the

accounting for leases of other assets.

Real Estate Lessors Must Perform

Classification Test

Since ASC 842 does not distinguish between real estate

leases and non–real estate leases and does not require that title

transfer occur before a sales-type lease is recognized, real estate

lessors will need to evaluate whether leases meet the criteria for

classification as a sales-type lease.

Collectibility Does Not Affect

Classification as Sales-Type Lease

While collectibility affects recognition related to

sales-type leases under ASC 842 (discussed in Section 9.3.7.2), ASC 842 does not

address collectibility with respect to the classification of such

leases. Therefore, because the classification criteria in this regard

are less strict, more leases will qualify as sales-type leases than

under previous guidance.

9.2.1.1 Transfer of Ownership at the End of the Lease Term — ASC 842-10-25-2(a)

ASC 842-10

55-4 The criterion in paragraph 842-10-25-2(a) is met in leases that provide, upon the lessee’s performance

in accordance with the terms of the lease, that the lessor should execute and deliver to the lessee such

documents (including, if applicable, a bill of sale) as may be required to release the underlying asset from the

lease and to transfer ownership to the lessee.

55-5 The criterion in paragraph 842-10-25-2(a) also is met in situations in which the lease requires the payment

by the lessee of a nominal amount (for example, the minimum fee required by the statutory regulation to

transfer ownership) in connection with the transfer of ownership.

55-6 A provision in a lease that ownership of the underlying asset is not transferred to the lessee if the lessee

elects not to pay the specified fee (whether nominal or otherwise) to complete the transfer is an option

to purchase the underlying asset. Such a provision does not satisfy the transfer-of-ownership criterion in

paragraph 842-10-25-2(a).

If the lease transfers ownership, such as through the transfer of title at or

shortly after the end of the lease term, the above criterion in ASC

842-10-25-2(a) would be met. In substance, such a transaction is akin to a

financed purchase (i.e., the asset was purchased and financed through lease

payments). If the lessee is required to pay a nominal fee for title

transfer, the lease would meet the criterion in ASC 842-10-25-2(a). If

paying the fee (even in circumstances in which the fee is nominal) is

optional, the lease would not meet this criterion, although the lease should

be evaluated under the “reasonably certain purchase option” criterion in ASC

842-10-25-2(b); see further discussion in the next section.

9.2.1.2 Purchase Option Reasonably Certain to Be Exercised — ASC 842-10-25-2(b)

As indicated in ASC 842-10-25-2(b), when a “lease grants the lessee an option to

purchase the underlying asset,” it must be reasonably certain that the

lessee will exercise that option, at which point the lessor is required to

classify the lease as a sales-type lease. “Reasonably certain” is a high

threshold. A purchase option’s exercise may be reasonably certain for many

reasons (e.g., an economic compulsion or incentive for the lessee to

exercise its option). See Section 5.2.2 for a discussion of the notion of “reasonably

certain.”

ASC 842-10-55-26 includes a list of economic factors (not all-inclusive) for an entity to consider when

evaluating whether the exercise of an option is reasonably certain. Such an evaluation must include an

assessment of whether an economic compulsion exists.

The examples below demonstrate scenarios in which the lessee’s exercise of its purchase option would be reasonably certain.

Example 9-1

Entity P leases a tractor that it may purchase for $10,000 at the end of the lease term. The fair value of the tractor is expected to be $20,000 when the lease term ends. Further, P has provided the lessor with a residual value guarantee of $25,000 in the event that P does not exercise the purchase option.

Example 9-2

Entity U leases an airplane in which it installs luxury seating and a gold-plated cocktail bar, both of which add significant value to the airplane. At the end of the lease term in three years, U may purchase the airplane for an amount that is commonly paid for an airplane that does not have luxury seating and a cocktail bar. The remaining useful life of the seating and bar assets extends 20 years after the noncancelable lease term.

9.2.1.3 Major Part of the Remaining Economic Life — ASC 842-10-25-2(c)

ASC 842-10

55-2 When determining lease classification, one reasonable approach to assessing the [criterion in paragraph] 842-10-25-2(c) . . . would be to conclude:

- Seventy-five percent or more of the remaining economic life of the underlying asset is a major part of the remaining economic life of that underlying asset. . . .

The ASC master glossary defines economic life as “[e]ither the period over which

an asset is expected to be economically usable by one or more users or the

number of production or similar units expected to be obtained from an asset

by one or more users.” As noted above, if the “lease term is for the major

part of the remaining economic life of the underlying asset,” the lease is a

sales-type lease; however, if the lease term begins “at or near the end of

the economic life of the underlying asset,” the lessor should not use this

criterion in its evaluation. (For further discussion, see Section

9.2.1.3.5.)

The lease classification guidance in ASC 842-10-25-2 does not explicitly

prescribe bright-line thresholds as part of the economic-life test;

therefore, an entity is permitted, but is not required, to assess certain

quantitative bright-line thresholds when classifying a lease under ASC

842.

The implementation guidance in ASC 842-10-55-2 further states that a

reasonable approach to applying the lease classification criteria in ASC 842

would be the use of certain bright-line thresholds as follows:

When determining lease classification, one

reasonable approach to assessing the criteria in paragraphs

842-10-25-2(c) through (d) and 842-10-25-3(b)(1) would be to

conclude:

-

Seventy-five percent or more of the remaining economic life of the underlying asset is a major part of the remaining economic life of that underlying asset.

-

A commencement date that falls at or near the end of the economic life of the underlying asset refers to a commencement date that falls within the last 25 percent of the total economic life of the underlying asset.

-

Ninety percent or more of the fair value of the underlying asset amounts to substantially all the fair value of the underlying asset.

On the basis of this implementation guidance, we would not

object if an entity were to apply bright-line thresholds when classifying a

lease under ASC 842. We would expect that under such an approach, an entity

would classify a lease in accordance with the quantitative result. That is,

if an entity, as an accounting policy, elects to apply bright-line

thresholds and determines that a lease term is equal to 76 percent of an

asset’s useful life, the entity should classify the lease as a sales-type

lease. The entity should not attempt to overcome the assessment with

qualitative evidence to the contrary. Likewise, if the same entity were to

determine that a lease term is equal to 74 percent of an asset’s useful

life, the entity should classify the lease as an operating lease (provided

that other lease classification criteria are not met). We would expect that

if an entity were to decide to apply the bright-line thresholds in ASC 840

when classifying a lease, the entity would apply those thresholds

consistently to all of its leases.

9.2.1.3.1 Estimated Economic Life Versus Depreciable Life

Generally, we would expect the economic life of an asset

to correspond to its depreciable life used for financial reporting. In

accordance with ASC 360, depreciable life is calculated on the basis of

the asset’s useful life, which is similar but not identical to

the economic life an entity uses in performing the lease

classification test.

The ASC master glossary defines useful life as the

“period over which an asset is expected to contribute directly or

indirectly to future cash flows” and economic life as “[e]ither the

period over which an asset is expected to be economically usable by one

or more users or the number of production or similar units expected to

be obtained from an asset by one or more users.”

The objective of determining either the useful life or

economic life of an asset is to identify the period over which the asset

will provide benefit. The asset’s useful life represents the period over

which the reporting entity will benefit from use

of the asset. In contrast, the economic life represents the period over

which “one or more users” will benefit from use

of the asset. Therefore, the asset’s estimated depreciable life pertains

to the intended use by the current owner, whereas the estimated economic

life may encompass both the current and future owners of the asset.

This difference between the two definitions is not

relevant in many cases since a single entity (the current owner) is

often expected to use an asset for its entire life. However, depending

on the facts and circumstances, it may sometimes be appropriate for an

entity to use an estimated economic life for lease classification

purposes that is longer than the asset’s estimated depreciable life.

Example 9-3

Company X, an automobile lessor,

routinely purchases automobiles that are

economically usable for seven years. Company X

leases the automobiles to lessees for three years

and sells the automobiles after the end of the

three-year lease term. Company X may have a

supportable basis for using a three-year

depreciable life (with a correspondingly higher

salvage value) for financial reporting purposes

but a seven-year economic life for lease

classification purposes.

9.2.1.3.2 Economic Life Considerations for Land

Land has an infinite economic life and therefore could

never meet the criterion in ASC 842-10-25-2(c). Thus, the estimated

economic-life test cannot be applied to a lease that only involves land

or when land is treated as a separate lease component.

9.2.1.3.3 Impact of Lessor’s Intent to Sell Leased Property at the End of the Lease Term on Determination of the Estimated Economic Life of Leased Property

As described in ASC 842-10-25-2(c), the third criterion

for classifying a lease as a sales-type lease is that the “lease term is

for the major part of the remaining economic life of the underlying

asset.” However, an entity should not use this criterion to classify the

lease “if the commencement date falls at or near the end of the economic

life of the underlying asset.”

The lessor’s intention to sell the leased property

immediately after the end of the lease term should not influence the

asset’s estimated economic life if the asset can still be used for its

intended purpose by other users. Generally, decisions concerning

economic lives for leased property will be similar to those for owned

assets. Thus, the estimated economic life of a leased asset generally

will be the same as the depreciable life of a similar asset for

financial reporting purposes (except as discussed in Section

9.2.1.3.1).

9.2.1.3.4 Lease Agreement Covering a Group of Assets That Have Different Economic Lives

A lease contract often includes a package of equipment.

For example, an equipment lease may include virtually all pieces of

equipment necessary to operate a store (e.g., refrigeration cases, air

conditioning units, alarm and phone systems, cash registers, and store

furniture).

When pieces of equipment that have different useful

economic lives are leased in the aggregate, an entity should consider

the guidance in ASC 842-10-15-28, which states that a right to use an

asset would be considered a separate lease component when it meets the

following two criteria:

-

The lessee can benefit from the right of use either on its own or together with other resources that are readily available to the lessee. Readily available resources are goods or services that are sold or leased separately (by the lessor or other suppliers) or resources that the lessee already has obtained (from the lessor or from other transactions or events).

-

The right of use is neither highly dependent on nor highly interrelated with the other right(s) to use underlying assets in the contract. A lessee’s right to use an underlying asset is highly dependent on or highly interrelated with another right to use an underlying asset if each right of use significantly affects the other.

To the extent that the above guidance does not require

separation, an entity should then consider the provisions of ASC

842-10-25-5, which indicates that “[i]f a single lease component

contains the right to use more than one underlying asset (see paragraphs

842-10-15-28 through 15-29), an entity shall consider the remaining

economic life of the predominant asset in the lease component for

purposes of applying the criterion in paragraph 842-10-25-2(c).”

Regarding the assessment of the predominant asset in a lease component,

paragraph BC74 of ASU 2016-02 states, in part:

The Board noted that assessing the predominant

asset in a lease component that includes multiple underlying

assets will be straightforward in most cases. That is, the

assessment is a qualitative one that requires entities to

conclude on what is the most important element of the lease,

which should be relatively clear in most cases. The Board also

noted that if an entity is unable to identify the predominant

asset, it may indicate that there is more than one separate

lease component in the contract.

Chapter 4 discusses, in detail, the guidance in ASC

842-10-15-28 on separating leasing components.

9.2.1.3.5 At or Near the End of the Remaining Economic Life

ASC 842-10

55-2 When determining lease classification, one reasonable approach to assessing the [criterion in paragraph]

842-10-25-2(c) . . . would be to conclude: . . .

b. A commencement date that falls at or near the end of the economic life of the underlying asset refers

to a commencement date that falls within the last 25 percent of the total economic life of the underlying

asset. . . .

If a lease component is at or near the end of its economic life, it is not

subject to the economic-life test. In its 2013 leasing ED, the FASB

contemplated not including this exception. Paragraph BC71 of ASU 2016-02

addresses the Board’s reasons for ultimately including the exception in

the leasing guidance and states, in part:

The exception to considering this criterion when

the lease commences at or near the end of the economic life of

the underlying asset is contrary to the lease classification

principle because a lessee can direct the use of and obtain

substantially all the remaining benefits from a significantly

used asset just the same as it can a new or slightly used asset.

However, the Board determined that an exception is appropriate

because it would be inconsistent to require that a lease

covering the last few years of an underlying asset’s economic

life be recorded as a finance lease by a lessee (or sales-type

lease by a lessor) when a similar lease of that asset earlier in

its economic life would have been classified as an operating

lease. The Board concluded that this would not appropriately

reflect the economics of those leases.

9.2.1.4 Substantially All of the Fair Value of the Underlying Asset — ASC 842-10-25-2(d)

ASC 842-10

25-4 A lessor shall assess the criteria in paragraphs 842-10-25-2(d) . . . using the rate implicit in the lease. For purposes of assessing the criterion in paragraph 842-10-25-2(d), a lessor shall assume that no initial direct costs will be deferred if, at the commencement date, the fair value of the underlying asset is different from its carrying amount.

55-2 When determining lease classification, one reasonable approach to assessing the [criterion in paragraph 842-10-25-2(d)] would be to conclude: . . .

c. Ninety percent or more of the fair value of the underlying asset amounts to substantially all the fair value of the underlying asset.

55-8 When evaluating the lease classification criteria in paragraphs 842-10-25-2(d) and 842-10-25-3(b)(1), the fair value of the underlying asset should be reduced by any related investment tax credit retained by the lessor and expected to be realized by the lessor.

As indicated in ASC 842-10-25-2(d), if the “present value of the sum of the lease payments and any residual value guaranteed by the lessee that is not already reflected in the lease payments . . . equals or exceeds substantially all of the fair value of the underlying asset,” the lease is classified as a sales-type lease. The present value is calculated by using a discounted cash flow approach. (See Chapter 6 for details on the amounts included in this calculation.) While a lessee will generally use its incremental borrowing rate (if the rate implicit in the lease is not readily determinable) to calculate the present value of its lease payments, as discussed in Section 7.2, a lessor must use the rate implicit in the lease. The ASC master glossary defines the rate implicit in the lease as follows:

The rate of interest that, at a given date, causes the aggregate present value of (a) the lease payments and (b) the amount that a lessor expects to derive from the underlying asset following the end of the lease term to equal the sum of (1) the fair value of the underlying asset minus any related investment tax credit retained and expected to be realized by the lessor and (2) any deferred initial direct costs of the lessor. However, if the rate

determined in accordance with the preceding sentence is less than zero, a rate implicit in the lease of zero shall

be used.

An entity may solve for the rate implicit in the lease by

using the internal-rate-of-return calculation function through either a

spreadsheet database (as shown in the example below) or another calculator

mechanism.

Example 9-4

A lessor leases a yacht with a fair

value of $256,300 to an actor for three years for an

annual payment made in arrears of $75,000. When the

actor returns the yacht, the fair value of the asset

is expected to be $90,000. Using an

internal-rate-of-return functionality, the lessor

determines that its rate implicit in the lease is

9.57 percent.

Note that, in this example, no ITCs

were received and no initial direct costs were

incurred.

Connecting the Dots

Calculating a Negative “Rate

Implicit in the Lease”

We have observed situations in which the outcome of

the calculation of the “rate implicit in the lease,” which is based

on how that term is defined in ASC 842-30-20, may result in a

negative discount rate. However, at the FASB’s November 30, 2016,

meeting, the Board acknowledged that using a negative discount rate

to determine the rate implicit in the lease (as defined in ASC

842-10-20) is inappropriate. ASU 2018-10 clarifies

that lessors should use a 0 percent discount rate when measuring the

net investment in a lease if the rate implicit in the lease is

negative. See Section E.3.1.3 for further discussion of the

ASU.

Use of Bright-Line Thresholds — Fair Value Test and

“Substantially All”

The lease classification guidance in ASC 842-10-25-2

does not explicitly prescribe bright-line thresholds as part of the

fair value test; therefore, an entity is permitted but is not

required to assess certain quantitative bright-line thresholds when

classifying a lease under ASC 842.

The implementation guidance in ASC 842-10-55-2 further states that

the use of the following bright-line thresholds would be a

reasonable approach to applying the lease classification criteria in

ASC 842:

When determining lease classification, one reasonable

approach to assessing the criteria in paragraphs

842-10-25-2(c) through (d) and 842-10-25-3(b)(1) would be to

conclude:

- Seventy-five percent or more of the remaining economic life of the underlying asset is a major part of the remaining economic life of that underlying asset.

- A commencement date that falls at or near the end of the economic life of the underlying asset refers to a commencement date that falls within the last 25 percent of the total economic life of the underlying asset.

- Ninety percent or more of the fair value of the underlying asset amounts to substantially all the fair value of the underlying asset.

On the basis of this implementation guidance, we would not object if

an entity were to apply bright-line thresholds when classifying a

lease under ASC 842. We would expect that, under such an approach,

an entity would classify a lease in accordance with the quantitative

result. That is, if an entity, as an accounting policy, elects a

bright-line threshold of 90 percent as substantially all, when the

present value of the lease payments equals 91 percent of the

underlying asset’s fair value, the entity should classify the lease

as a sales-type lease. The entity should not attempt to overcome the

assessment with qualitative evidence to the contrary. Likewise, if,

as a result of the present value calculation, the present value of

the lease payments equals 89 percent of the underlying asset’s fair

value, the entity should classify the lease as an operating lease

(provided that other lease classification criteria are not met). We

would expect that if an entity decides to apply bright-line

thresholds when classifying a lease, the entity would apply those

thresholds consistently to all of its leases.

Evaluating “Substantially

All”

One of the most notable aspects of ASC 842 is the

exclusion of “bright lines” (e.g., the 90 percent previously used in

the fair value test) from the lease classification tests. However,

ASC 842-10- 55-2 acknowledges that 90 percent may be an appropriate

threshold for the “substantially all” criterion. See Section

9.2.1.3 for more information. An entity will need to

evaluate the “substantially all” criterion when classifying a lease

under ASC 842, regardless of when the lease term begins.

At or Near the End of Its

Economic Life and “Substantially All”

As discussed in Section 9.2.1.3.5, the FASB

allowed lessors not to consider the economic-life test if the lease

commences within the final 25 percent of the total economic life of

the underlying asset. Accordingly, lessors have one less criterion

to assess for an asset that is near the end of its useful life;

however, the “substantially all” test still applies to those same

leases. Therefore, even if the underlying asset is in the last 25

percent of its economic life, sales-type lease classification may

still be warranted if the lessor concludes, after considering the

threshold described in ASC 842-10-55-2(c), that substantially all of

the associated value is being transferred to the lessee.

Evaluating 89.9 Percent Lease

Payments

Under ASC 840, there were many opportunities to

create highly structured leases. Specifically, many leases were

designed so that the present value of lease payments would be 89.9

percent of the fair value. Because the FASB has taken a more

principles-based approach to classification in ASC 842, we do not

believe that an 89.9 percent present value would necessarily result

in a non-sales-type lease. However, this would depend on the

entity’s accounting policies (see Section 9.2.1.3), which should

be consistently applied.

Consideration of

Nonperformance-Related Default Provisions

Some lease agreements contain nonperformance-related

default provisions that may require the lessee to purchase the

leased asset or make another payment if the lessee is in default

under such provisions. For more information about this issue and

about lessees’ treatment of payments associated with

nonperformance-related default provisions under ASC 842, see

Section

8.3.3.6. In line with the discussion in that section,

lessors should generally treat these payments as variable and should

consider the guidance in ASC 842-30. See Section 9.3 for more

information about a lessor’s treatment of variable lease

payments.

9.2.1.4.1 Lessor’s Consideration of Initial Direct Costs Related to the Rate Implicit in the Lease

In considering initial direct costs when calculating the

rate implicit in the lease, a lessor must first assess the appropriate

classification of the lease. This assessment would start with a

determination of whether the lease (1) should be classified as a

sales-type lease because it meets any of the criteria in ASC 842-10-25-2

and (2) meets the criterion in ASC 842-10-25-3A. If none of the criteria

in ASC 842-10-25-2 or ASC 842-10-25-3A are met, the lessor is next

required to determine whether the lease must be classified as a direct

financing lease in accordance with ASC 842-10-25-3(b); if not, the lease

would be classified as an operating lease.

ASC 842-10-25-2(d), which contains one of the criteria

for sales-type lease classification, states:

The present value of the sum of the lease

payments and any residual value guaranteed by the lessee that is

not already reflected in the lease payments in accordance with

paragraph 842-10-30-5(f) equals or exceeds substantially all of

the fair value of the underlying asset.

To determine the “present value of the sum of the lease

payments and any residual value guaranteed by the lessee,” the lessor

must determine the “rate implicit in the lease.” The ASC master glossary

defines the rate implicit in the lease as follows:

The rate of interest that, at a given date,

causes the aggregate present value of (a) the lease payments and

(b) the amount that a lessor expects to derive from the

underlying asset following the end of the lease term to equal

the sum of (1) the fair value of the underlying asset minus any

related investment tax credit retained and expected to be

realized by the lessor and (2) any deferred initial direct costs

of the lessor. However, if the rate determined in accordance

with the preceding sentence is less than zero, a rate implicit

in the lease of zero shall be used.

ASC 842-10-25-4 clarifies that “[f]or purposes of

assessing the criterion in paragraph 842-10-25-2(d), a lessor shall

assume that no initial direct costs will be deferred if, at the

commencement date, the fair value of the underlying asset is different

from its carrying amount.”

As a result, when determining whether a lease is a

sales-type lease under ASC 842-10-25-2(d) (quoted above), the lessor does not include initial direct costs in its

determination of the rate implicit in the lease if the underlying

asset’s fair value differs from its carrying value.

In all other cases (i.e., when the underlying asset’s

fair value equals its carrying value in the determination of whether a

lease is a sales-type lease under ASC 842-10-25-2(d) or whether a lease

is a direct financing lease under ASC 842-10-25-3(b)), the lessor would

include initial direct costs in its

determination of the rate implicit in the lease.

With respect to initial recognition and measurement, a

lessor is required to recognize (at commencement) a net investment in

the lease for sales-type and direct financing leases. The net investment

in the lease comprises the sum of the lease receivable and any

unguaranteed residual value, both of which are measured at present value

by using the same rate implicit in the lease that was used for lease

classification purposes.

For sales-type leases, ASC 842-30-25-1(c) requires that

initial direct costs be expensed “if, at the commencement date, the fair

value of the underlying asset is different from its carrying amount.” In

these cases, because the rate implicit in the lease (as determined

during lease classification) did not include

initial direct costs because they were not eligible for deferral, those

costs are automatically excluded from the net investment in the lease

(i.e., there is no need to remove them separately).

In all other cases (i.e., when the underlying asset’s

fair value equals its carrying value in the determination of whether a

lease is a sales-type lease or whether a lease is a direct financing

lease under ASC 842-10-25-3(b)), “[i]f the fair value of the underlying

asset equals its carrying amount, initial direct costs . . . are

deferred at the commencement date and included in the measurement of the

net investment in the lease” in accordance with ASC 842-30-25-1(c).

Therefore, because the initial direct costs are eligible for deferral

and were included in the determination of the

rate implicit in the lease for classification purposes, they are

automatically included in the rate used to calculate the net investment

in the lease.2

This is consistent with ASC 842-30-25-1(c) (sales-type lease recognition)

and ASC 842-30-25-8 (direct financing lease recognition), each of which

suggests that the rate implicit in the lease is defined in such a way

that initial direct costs eligible for deferral “are included

automatically in the net investment in the lease; there is no need to

add them separately.”

9.2.1.4.2 Unit of Account for Assessing Lease Classification

The lessor must classify a lease as a sales-type lease

if (1) any of the lease classification criteria in ASC 842-10-25-2 are

met and (2) there is no selling loss in a lease containing variable

payments that do not depend on an index or a rate in accordance with ASC

842-10-25-3A.

In evaluating the criterion in ASC 842-10-25-2(d) (i.e.,

in assessing whether the lease is a sales-type lease), a multiunit real

estate lessor would use the fair value of the unit allocable to the

lease component in its present value test. In other words, the lessor

would identify the underlying asset at the level associated with the

space being leased and not beyond the identified lease component (e.g.,

at the level of a retail store in a shopping mall, not at the level of

the shopping mall itself).

Example 9-5

Lessor A leases a retail store

at the mall it owns. The fair value of the mall is

$10 million, and the fair value of the individual

retail store is $500,000. The present value of the

lease payments for the retail store is $450,000

(there is no residual value guarantee). To

determine the classification of the lease, the

lessor should compare the fair value of the

portion of the building allocable to the lease

component ($500,000) with the present value of the

lease payments ($450,000).

Connecting the Dots

ASU 2019-01 on

Acquisition Costs for Lessors That Are Not Manufacturers

or Dealers

In March 2019, the FASB issued ASU

2019-01, which provides guidance on how

lessors that are not manufacturers or dealers (qualifying

lessors) should determine the fair value of the underlying asset

and apply it to lease classification and measurement.

Specifically, for qualifying lessors, the fair value of the

underlying asset at lease commencement should be its cost,

including any acquisition costs, such as sales taxes or delivery

charges. Accordingly, many costs related to the fulfillment of

sales-type leases and direct financing leases should be

capitalized as part of the net investment in the lease for

qualifying lessors. However, if a significant lapse of time

occurs between the acquisition of the underlying asset and lease

commencement, lessors are required to determine fair value in

accordance with ASC 820, which does not include such costs.

Moreover, since this ASU does not apply to manufacturers and

dealers, such lessors are always required to determine fair

value in accordance with ASC 820. See Section E.3.1.7 for more

information about ASU 2019-01.

9.2.1.4.3 Impracticable to Determine Fair Value

ASC 842-10

55-3 In some cases, it may not be practicable for an entity to determine the fair value of an underlying asset. In the context of this Topic, practicable means that a reasonable estimate of fair value can be made without undue cost or effort. It is a dynamic concept; what is practicable for one entity may not be practicable for another, what is practicable in one period may not be practicable in another, and what is practicable for one underlying asset (or class of underlying asset) may not be practicable for another. In those cases in which it is not practicable for an entity to determine the fair value of an underlying asset, lease classification should be determined without consideration of the criteria in paragraphs 842-10-25-2(d) and 842-10-25-3(b)(1).

We believe it would be unlikely that a lessor would not be able to determine the

fair value of an underlying asset, including portions of larger assets.

Lessors that consider this paragraph to be applicable to their facts and

circumstances should consult their accounting advisers.

In determining whether to classify a lease as a

sales-type or direct financing lease, a lessor must determine whether

“the present value of the sum of the lease payments . . . equals or

exceeds substantially all of the fair value of the underlying asset” in

accordance with ASC 842-10-25-2(d) (see Section 9.2.1.4). Accordingly,

when classifying the lease (i.e., as a sales-type, direct financing, or

operating lease), the lessor must determine the fair value of the

underlying asset — for use in the fair value test — at the level

associated with the identified lease component (see Section

9.2.1.4.2). This level could be a portion of a larger asset,

such as a floor of an office building. If it is impracticable for a

lessor to determine the fair value of an underlying asset in accordance

with ASC 842-10-55-3, the lessor should assess the lease classification

without considering the criterion in ASC 842-10-25-2(d) and ASC

842-10-25-3(b)(1). In this context, “practicable” means that fair value

can be reasonably estimated without undue cost or effort.

Consider an example in which a lessor leases space on a

cell tower (e.g., a hanger) to a lessee. The lessor previously recorded

the entire cell tower (i.e., the larger asset) on its books, and the

hanger is considered a portion of the larger asset. The lessor has a

practice of leasing individual hangers within the cell tower to lessees;

thus, the individual hanger would be the unit of account from a leasing

perspective. A similar situation may arise when a lessor leases a floor

of a building to a lessee. The entire building (i.e., the larger asset)

is recorded on the lessor’s books. The lessor commonly leases individual

floors in the building to lessees. As stated above, when classifying the

lease, the lessor must determine the fair value of the underlying asset

for use in the fair value test — which would be at the level of the

individual hanger or individual floor in these examples — unless it is

impracticable to do so.

While ASC 842 does not address how a lessor should

determine the fair value of a portion of a larger asset, we believe that

the lessor can use various methods to determine the fair value of a

portion of a larger asset, depending on the facts and circumstances.

Because a lessor will typically be able to determine the fair value of

the entire larger asset (e.g., a cell tower or building, as described in

the examples above), it will often be appropriate to use an “allocation

approach” to allocate the fair value of the larger asset to the

respective portions of the larger asset that are being leased.

For example, the fair value of the larger asset could be

proportionately allocated — on the basis of the perceived value of the

individual leasable spaces — to the individual portions of the larger

asset that the lessor leases. When this method is used, other conditions

that may be more representative of the fair value of the leased asset

should be considered. In a building, for instance, higher floors are

often more desirable, have a higher stand-alone selling price, and are

leased at a higher cost to the lessee than lower floors. In such

circumstances, use of an appropriate allocation method would result in

the allocation of a greater fair value to the higher floors. Such an

allocation would better represent the economics of the individual lease

arrangements and better reflect the fair value of each respective

portion.

Likewise, we believe that an entity that is estimating

the fair value of a portion of a larger asset should consider the

intended use of the asset. It is also important not to confuse relative

fair value with relative construction or replacement costs. In the cell

tower example described above, while the percentage of the costs for the

individual hangers may not be disproportionately high compared with the

cost of the overall structure, it is likely that the hangers in the

aggregate account for most of the fair value of the tower since they

represent its revenue-producing parts. In other words, we would

sometimes expect the fair value of discrete portions of a larger asset

to be disproportionate compared with that of the entire asset on a space

or square-footage basis when the relative revenue-producing potential of

the discrete portions is taken into account.

We generally believe that it would be unusual for a

lessor not to be able to determine the fair value of a portion of an

underlying asset. Further, we would expect that a lessor that can

estimate the fair value of the larger asset (which will generally be the

case) would typically be able to reasonably allocate an appropriate

percentage of that fair value to the portion being leased without undo

cost or effort.

9.2.1.4.4 Residual Value Guarantees Provided for a Portfolio of Assets

ASC 842-10

55-9 Lessors may obtain

residual value guarantees for a portfolio of

underlying assets for which settlement is not

solely based on the residual value of the

individual underlying assets. In such cases, the

lessor is economically assured of receiving a

minimum residual value for a portfolio of assets

that are subject to separate leases but not for

each individual asset. Accordingly, when an asset

has a residual value in excess of the “guaranteed”

amount, that excess is offset against shortfalls

in residual value that exist in other assets in

the portfolio.

55-10 Residual value guarantees of a portfolio of underlying assets preclude a lessor from determining the amount of the guaranteed residual value of any individual underlying asset within the portfolio. Consequently, no such amounts should be considered when evaluating the lease classification criteria in paragraphs 842-10-25-2(d) and 842-10-25-3(b)(1).

Although a lessor would consider residual value guarantees on individual leases

as part of the lease payments when performing the lease classification

test, such guarantees would generally be excluded from the test when

they are provided for a portfolio of assets under ASC 842-10-55-10.

However, as discussed below, there is a potential exception to this

rule.

Lessors often enter into lease agreements to lease

multiple similar assets to lessees. In these circumstances, lessees will

often guarantee the residual value for the group of assets being leased

(e.g., the portfolio of underlying assets) rather than that for each

individual underlying asset. ASC 842-10-55-10 states that a lessor should not consider residual value guarantees

of a portfolio of underlying assets when evaluating the lease

classification criteria, since “[r]esidual value guarantees of a

portfolio of underlying assets preclude a lessor from determining the

amount of the guaranteed residual value of any individual underlying

asset within the portfolio.”

The guidance in ASC 842 on how lessors should treat

residual value guarantees of a portfolio of underlying assets when

classifying a lease is similar to historical practice under ASC 840.

Specifically, in an inquiry, the SEC was asked to give its views on how

a lessor should apply ASC 840-10-25-1(d) and ASC 840-10-25-5 in

determining the minimum lease payments for lease classification purposes

when the lessee provided a guarantee of the aggregate residual value of

a portfolio of leased assets. ASC 840-30-S99-1 states that, in response

to this inquiry, the SEC staff indicated the following:

The SEC staff believes that residual value

guarantees of a portfolio of leased assets preclude a lessor

from determining the amount of the guaranteed residual value of

any individual leased asset within the portfolio at lease

inception and, accordingly, no such amounts should be included

in minimum lease payments.

Therefore, the general practice under ASC 840 was for a

lessor not to include residual value guarantees for a portfolio of

leased assets in the determination of minimum lease payments, since it

is not possible to identify the individual residual value guarantee for

any individual leased asset within the portfolio. Because the

classification analysis under ASC 840 was performed on an

individual-asset basis, it is rare for a lessor to include a residual

value guarantee of a portfolio of assets in the determination of minimum

lease payments. However, in certain circumstances, it is appropriate to

do so. Specifically, under ASC 840, if a group of leased assets

associated with the PRVG met the following criteria, the PRVG was

factored into the calculation of minimum lease payments:

-

The leases commenced and ended at the same time.

-

The leased assets were physically similar to each other.

-

The variability associated with the expected residual values was expected to be highly correlated (i.e., one asset’s residual value was expected to be similar to that of the other assets’ residual values).

Under ASC 842, a lessor can account for a group of

leases at a portfolio level provided that (1) the leases are similar in

nature (e.g., have similar underlying assets) and (2) have identical or

nearly identical contract provisions (see Section 8.2.2). In addition,

paragraph BC120 of ASU 2016-02 states, in part:

[T]he Board decided to explicitly state that

lessees and lessors are permitted to apply the leases guidance

at a portfolio level. The Board acknowledged that an entity

would need to apply judgment in selecting the size and

composition of the portfolio in such a way that the entity

reasonably expects that the application of the leases model to

the portfolio would not differ materially from the application

of the leases model to the individual leases in that

portfolio.

Because ASC 842 can be applied at a portfolio level,

lessors have questioned whether it is appropriate for them to factor in

a residual value guarantee for a group of assets being leased when

determining the lease classification of each separate lease. We believe

that, when certain facts and circumstances exist, it may be appropriate

for a lessor to consider a PRVG for a group of assets being leased.

Consider the example below.

Example 9-6

A lessor enters into an

agreement to lease 10 physically similar laptops

to a lessee. The leases commence and end on the

same day. The agreement has no stated renewal or

purchase options. The individual assets have a

fair value at commencement of $500 each and an

expected residual value at the end of the lease

term of $150 each. The variability associated with

the expected residual value of each laptop is

expected to be highly correlated. The lessee

guarantees that the combined residual value of the

leased assets will be $1,500. If the PRVG were

excluded from the lease classification test, all

of the individual leases would be operating

leases. However, if the PRVG were included,

classification may change depending on the

attribution of the PRVG to the individual leases

in the portfolio.

We believe that, as described in the example above,

there are circumstances in which it may be acceptable for a lessor to

include a PRVG in the classification of leased assets that are subject

to a residual value guarantee for the group of assets. In such

circumstances, we would expect the PRVG to be apportioned equally to

each leased asset (e.g., $150 per laptop in the above example).

In addition, we believe that the lessor may consider a

PRVG when classifying the individual leases within a portfolio when an

arrangement meets the following criteria that were applied in practice

under ASC 840 (outlined above and repurposed below):

-

The leases commence and end at the same time.

-

The leased assets are physically similar to each other.

-

The variability associated with the expected residual values is expected to be highly correlated.

While ASC 842-10-55-10, read literally, suggests that a

PRVG should never be considered in the lessor’s determination of lease

classification, we believe that the FASB did not intend to change this

historical practice under ASC 840. Further, we believe that use of the

criteria above will result in a lease classification that is consistent

with the underlying economics of the leasing arrangement.

9.2.1.5 Underlying Asset Is Specialized and Has No Alternative Use to the Lessor at the End of the Lease Term — ASC 842-10-25-2(e)

ASC 842-10

55-7 In assessing whether an underlying asset has an alternative use to the lessor at the end of the lease term

in accordance with paragraph 842-10-25-2(e), an entity should consider the effects of contractual restrictions

and practical limitations on the lessor’s ability to readily direct that asset for another use (for example, selling

it or leasing it to an entity other than the lessee). A contractual restriction on a lessor’s ability to direct an

underlying asset for another use must be substantive for the asset not to have an alternative use to the lessor.

A contractual restriction is substantive if it is enforceable. A practical limitation on a lessor’s ability to direct

an underlying asset for another use exists if the lessor would incur significant economic losses to direct the

underlying asset for another use. A significant economic loss could arise because the lessor either would incur

significant costs to rework the asset or would only be able to sell or re-lease the asset at a significant loss. For

example, a lessor may be practically limited from redirecting assets that either have design specifications that

are unique to the lessee or that are located in remote areas. The possibility of the contract with the customer

being terminated is not a relevant consideration in assessing whether the lessor would be able to readily direct

the underlying asset for another use.

The criterion in ASC 842-10-25-2(e) states that if the “underlying asset is of such a specialized nature

that it is expected to have no alternative use to the lessor at the end of the lease term,” the lease is a

sales-type lease. When an underlying asset has no alternative use to the lessor at the end of a lease

term, it is presumed that the lessee will consume all (or substantially all) of the benefits of the asset. The

substantive lack of alternative use can be identified if there is a contractual restriction or an anticipated

significant economic loss related to directing the asset for another use.

Connecting the Dots

Meeting the Criterion in ASC

842-10-25-2(e)

It is unlikely that the criterion in ASC

842-10-25-2(e) would be met in isolation because a lessor

economically would not enter into an arrangement in which it would

not be compensated to obtain a worthless asset at the end of a lease

term. We do not believe that this criterion should be interpreted as

applying to situations in which the underlying asset is near the end

of its economic life and the lessee, by virtue of the lease,

therefore has obtained all of the use of the asset so that it has

“no alternative use.” This criterion is intended to identify

situations in which the lessee uses all of the asset’s economic

benefits because the asset is so specialized for that particular

lessee that the lessor would not be expected to generate economic

benefit from the asset’s use outside of the lease. For example, if a

lease is structured with entirely variable lease payments that do

not depend on an index or a rate (and the lease therefore does not

meet the criterion in ASC 842-10-25-2(d)), the lease may be more

likely to meet criterion (e) in isolation. However, if such leases

result in a selling loss, they may need to be classified as

operating leases in accordance with the amendments made by ASU

2021-05, as discussed in the section below.

9.2.1.5.1 Significant Economic Losses to Direct an Underlying Asset for Another Use

ASC 842-10-55-7 states, in part:

A practical limitation on a lessor’s ability to

direct an underlying asset for another use exists if the lessor

would incur significant economic losses to direct the underlying

asset for another use. A significant economic loss could arise

because the lessor either would incur significant costs to

rework the asset or would only be able to sell or re-lease the

asset at a significant [economic] loss.

Although ASC 842 does not define the term “significant

economic loss,” the standard and the Background Information and Basis

for Conclusions of ASU 2016-02 discuss the term “significant economic

incentive.” When an entity has a significant economic incentive, it may

conclude that the exercise of a purchase option or renewal option is

reasonably certain in accordance with ASC 842-10-30-1 through 30-3.

Because “reasonably certain” is a high threshold in the assessment of

renewal (termination) options and purchase options (as discussed in

Section

5.2.2), we would expect the threshold for a significant

economic loss to also be high.

In addition, an entity can consider ASC 606-10-55-10

when assessing situations in which a significant loss exists. ASC

606-10-55-10 states:

A practical limitation on an entity’s ability to

direct an asset for another use exists if an entity would incur

significant economic losses to direct the asset for another use.

A significant economic loss could arise

because the entity either would incur significant costs to

rework the asset or would only be able to sell the asset at

a significant loss. For example, an entity may be

practically limited from redirecting assets that either have

design specifications that are unique to a customer or are

located in remote areas. [Emphasis added]

Example 9-7

An entity leases a highly

specialized underwater vehicle with patented

technology to another entity. The asset took three

years to produce. The lessee uses the asset to

search the deep ocean floor for buried treasure in

a remote area of the Arctic Ocean. The cost of

transporting the asset to the search site was

approximately half the cost of the asset itself,

and it is not expected that any other entity is

going to want to use that asset in that specific

location. The lessor would incur significant

losses in transporting the asset to its

manufacturing facility in Chicago at the end of

the lease term for refurbishment and redeployment.

The lessor does not believe that any other

entities would be interested in a similar use

(searching the Arctic Ocean for buried treasure),

and the asset is designed for that particular

environment and no other. As a result, the lessor

in this example would meet the criterion for

classifying the lease as a sales-type lease (i.e.,

the criterion in ASC 842-10-25-2(e)). We believe

that it is likely that other criteria for

sales-type classification (e.g., the

“substantially all of the fair value” test) would

also be met in such situations.

9.2.1.6 Lessor’s Accounting for Certain Leases With Variable Lease Payments

|

In July 2021, the FASB issued

ASU

2021-05, which requires a lessor to

classify a lease with variable lease payments that

do not depend on an index or rate as an operating

lease on the lease commencement date if specified

criteria are met. ASC 842-10-25-3A requires a lessor

to classify a lease with variable lease payments

that do not depend on an index or rate as an

operating lease at lease commencement if both of the

following conditions are met:

|

Because these leases will be classified as operating leases,

when applying the guidance in ASC 842-10-25-3A, the lessor would not

derecognize the underlying asset upon lease commencement but would continue

to depreciate the underlying asset over its useful life. Further, in

accordance with ASC 842-30-25-11(a), the lessor would recognize fixed lease

payments as “income . . . over the lease term on a straight-line basis

unless another systematic and rational basis is more representative of the

pattern in which benefit is expected to be derived from the use of the

underlying asset.” Variable lease payments would be recognized as “income in

profit or loss in the period in which the changes in facts and circumstances

on which the variable lease payments are based occur,” as indicated in ASC

842-30-25-11(b).

Note that the guidance in ASC 842-10-25-3A does not

prescribe a threshold for the amount of variable payments; the guidance must

be applied when a lease contains any amount of variable payments (in

addition to the requirement that the lessor would have otherwise recognized

a selling loss at lease commencement).

Connecting the Dots

Treatment of Leases with

Variable Payments

Under ASU 2021-05, which modified the lease

classification requirements, more lessors are required to classify

leases as operating leases rather than as sales-type or direct

financing leases. Accordingly, additional leases qualify for the

lessor practical expedient in ASC 842-10-15-42A, which allows

lessors to combine lease and nonlease components into a single

component if certain scope requirements are met. One of these

requirements is that the underlying lease component must be

classified as an operating lease. (See Section 4.3.3.2 for more

information about the lessor practical expedient.) In addition, the

classification as an operating lease may allow certain

sale-and-leaseback transactions to qualify as successful sales. (See

Section

10.3 for more information about evaluating

sale-and-leaseback transactions.)

Under ASC 606, variable payments are estimated and included in the

transaction price subject to a constraint. By contrast, under ASC

842, variable lease payments not linked to an index or rate are

generally excluded from the determination of a lessor’s lease

receivable.

Accordingly, sales-type or direct financing leases that have a

significant variable lease payment component may result in an

entity’s determination that there would be a loss at commencement

because the measurement of the lease receivable plus the

unguaranteed residual asset is less than the net carrying value of

the underlying asset. This could occur, for example, if lease

payments are based entirely on the number of units produced by the

leased asset (i.e., payments are 100 percent variable) or when a

portion of the expected cash flows from the lease is variable (e.g.,

50 percent of the total expected cash flows are variable). However,

these transactions typically do not represent an economic loss for

the lessor. A lease that meets these criteria records the lease as

an operating lease rather than a sales-type or direct financing

lease.

Types of Arrangements With

Significant Variable Lease Payments

Lease arrangements in a number of industries often

include significant or wholly variable lease payments. It is not

uncommon for such arrangements to be long-term enough that they

result in sales-type or direct financing lease classification under

ASC 842-10-25-2 and 25-3. However, these arrangements often would be

classified as operating leases since the criteria in ASC

842-10-25-3A would be met.

Arrangements in the energy sector are frequently

accounted for as leases with wholly variable payment streams. For

example, PPAs related to renewable energy (i.e., from solar or wind

generation facilities) (1) are commonly long-term and for the major

part of the economic life of the generation facility, (2) provide

for payments at a fixed price per unit of electricity output (e.g.,

$50 per megawatt hour [MWh]), and (3) require the lessee to take all

of the output produced by the facility but do not specify a minimum

level of production (i.e., the volume of output is wholly variable).

Although the output quantity is weather-dependent, the lessor

expects the arrangement to be profitable on the basis of historical

weather data.

We are also aware of arrangements in the oil and gas

industry in which a company builds a gathering and processing system

and leases it to a single user under a variable payment structure.

For example, an exploration company with rights to multiple oil

wells on dedicated acreage may contract with a midstream company to

construct and lease the infrastructure necessary to gather and

process the oil extracted from the wells. The arrangement may be

long-term and for a major part of the economic life of the

infrastructure, and the payment for the use of the infrastructure

may be 100 percent variable (e.g., a fixed price per unit multiplied

by the number of units gathered or processed) without a minimum

volume requirement. The midstream company would be willing to accept

variable consideration in the arrangement if reserve data related to

the wells suggest that a sufficient volume of oil will be extracted

over the term of the contract to make the arrangement

profitable.

In the real estate sector, a commercial real estate

lease arrangement (e.g., a lease of retail space) may be priced in

such a way that a significant amount of the expected payments is

contingent on the lessee’s sales (e.g., payments that are a fixed