Chapter 7 — Common Issues Related to Cash Flows

Chapter 7 — Common Issues Related to Cash Flows

The previous chapters of this Roadmap describe general

principles and provide certain examples related to the

classification of cash flows between operating, financing, and

investing activities. This chapter addresses common issues

associated with the classification of cash flows as operating,

investing, or financing.

7.1 Foreign Currency Cash Flows

ASC 830-230

45-1 A

statement of cash flows of an entity with foreign currency

transactions or foreign operations shall report the

reporting currency equivalent of foreign currency cash flows

using the exchange rates in effect at the time of the cash

flows. An appropriately weighted average exchange rate for

the period may be used for translation if the result is

substantially the same as if the rates at the dates of the

cash flows were used. (That is, paragraph 830-30-45-3

applies to cash receipts and cash payments.) The statement

of cash flows shall report the effect of exchange rate

changes on cash, cash equivalents, and amounts generally

described as restricted cash or restricted cash equivalents

held in foreign currencies as a separate part of the

reconciliation of the change in the total of cash, cash

equivalents, and amounts generally described as restricted

cash or restricted cash equivalents during the period. See

Example 1 (paragraph 830-230-55-1) for an illustration of

this guidance.

Entities may have transactions that are denominated in a foreign currency or businesses that operate in foreign currency environments. An entity should report the cash flow effect of transactions denominated in a foreign currency by using the exchange rates in effect on the date of such cash flows. As noted in ASC 830-230-45-1, instead of using the actual exchange rate on the date of a foreign currency transaction, an entity may use “an appropriately weighted average exchange rate” for translation “if the result is substantially the same as if the rates at the dates of the cash flows were used.”

A consolidated entity with operations whose functional currencies are foreign currencies may use the following approach when preparing its consolidated statement of cash flows:

- Prepare a separate statement of cash flows for each foreign operation by using the operation’s functional currency.

- Translate the stand-alone cash flow statement prepared in the functional currency of each foreign entity into the reporting currency of the parent entity.

- Consolidate the individual translated statements of cash flows.

The effects of exchange rate changes, or translation gains and losses, are not the same as the effects of transaction gains and losses and should not be presented or calculated in the same manner.

Effects of exchange rate changes may have a direct impact on cash receipts and payments but do not directly result in cash flows themselves.

Because unrealized transaction gains and losses arising from the remeasurement

of foreign-currency-denominated monetary assets and liabilities on the balance sheet

date are generally included in the determination of net income, such amounts should

be presented as a reconciling item between net income and net cash from operating

activities (either on the face of the statement under the indirect method or in a

separate schedule under the direct method).

Subsequently, any cash flows arising from the settlement of the foreign-currency-denominated asset and liability should be presented in the statement of cash flows as an operating, investing, or financing activity on the basis of the nature of such cash flows.

Translation gains and losses, however, are recognized in OCI and are not

included in the cash flows from operating, investing, or financing activities.

The effects of exchange rate changes on cash should be shown as a separate line item in the statement of cash flows as part of the reconciliation of beginning and ending cash balances. This issue was discussed in paragraph 101 of the Basis for Conclusions of FASB Statement 95, which stated, in part:

The effects of exchange rate changes on assets and liabilities denominated in foreign currencies, like those of other price changes, may affect the amount of a cash receipt or payment. But exchange rate changes do not themselves give rise to cash flows, and their effects on items other than cash thus have no place in a statement of cash flows. To achieve its objective, a statement of cash flows should reflect the reporting currency equivalent of cash receipts and payments that occur in a foreign currency. Because the effect of exchange rate changes on the reporting currency equivalent of cash held in foreign currencies affects the change in an enterprise’s cash balance during a period but is not a cash receipt or payment, the Board decided that the effect of exchange rate changes on cash should be reported as a separate item in the reconciliation of beginning and ending balances of cash. [Emphasis added]

In a manner consistent with the implementation guidance in ASC 830-230-55-15,

the effect of exchange rate changes on cash and cash equivalents is the sum of the

following two components:

-

For each foreign operation, the difference between the exchange rates used in translating functional currency cash flows and the exchange rate at year-end multiplied by the net cash flow activity for the period measured in the functional currency.

-

The fluctuation in the exchange rates from the beginning of the year to the end of the year multiplied by the beginning cash balance denominated in currencies other than the reporting currency.

Example 1 of ASC 830-230-55-1 through 55-15 (see Appendix A) illustrates the

computation of the effect of exchange rate changes on cash. The example below

illustrates the translation of a statement of cash flows that was prepared in a

functional currency into a reporting currency.

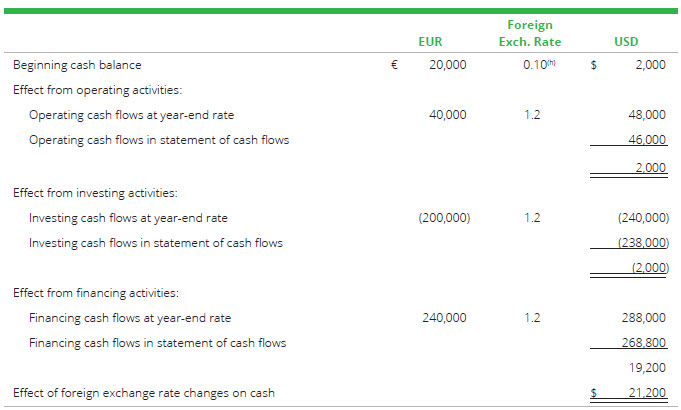

Example 7-1

Company B, a wholly owned foreign subsidiary

of Company A whose reporting currency is the U.S. dollar

(USD), is a calendar-year-end company and uses the euro

(EUR) as its functional currency. Company B issues 200,000

shares of common stock with a par value of EUR 1 on January

1, 20X0. On May 24, 20X1, B issues long-term debt of EUR

240,000, and on July 26, 20X1, B purchases equipment for EUR

200,000. Company A translates B’s statement of cash flows

into A’s reporting currency to prepare its consolidated

statement of cash flows.

The exchange rates between the EUR and the

USD are as follows:

Balance

Sheet

Statement of Income

as of December 31, 20X1

Statement of

Comprehensive Income as of December 31,

20X1

Statement of Cash

Flows as of December 31, 20X1

Notes to Table:

(a) Common stock was issued on January 1, 20X0,

when the exchange rate was 1 EUR to 1.05 USD.

(b) Retained earnings represents beginning retained

earnings plus current-period net income.

Accordingly, beginning retained earnings is

translated by using the historical rate as of

December 31, 20X0 (1.10), and current-period net

income is translated by using the 20X1

weighted-average rate (1.15). The resulting foreign

exchange rate is 1.126 but is rounded up to 1.13 for

simplicity.

(c) CTA adjustment:

(d) 20X1 weighted-average rate is used.

(e) Equipment was purchased on July 26, 20X1, when

the exchange rate was 1 EUR to 1.19 USD.

(f) A long-term debt was issued on May 4, 20X1,

when the exchange rate was 1 EUR to 1.12 USD.

(g) Effect of foreign exchange rate changes on

cash:

(h) Represents the difference between the exchange

rate on December 31, 20X0, and that on December 31,

20X1.

(i) Represents the difference between the exchange

rate on December 31, 20X1, and the 20X1

weighted-average rate.

For more information about foreign currency accounting and reporting matters,

see Deloitte’s Roadmap Foreign

Currency Matters.

7.2 Constructive Receipt and Disbursement

|

An entity may enter into arrangements in

which cash is received by or disbursed to another party on

behalf of the entity. Although these arrangements may not

result in a direct exchange of cash to or from the entity,

the same economic result is achieved if cash is received by

or disbursed to the entity directly (i.e., constructive

receipt and constructive disbursement, respectively).

Consequently, it is often difficult to determine whether the

entity should report these cash flows in its statement of

cash flows.

|

In some industries, the entity (e.g., an automobile dealer) may finance its

purchases of inventory through the supplier and, in many cases, the finance entity

is a subsidiary of the supplier. The finance subsidiary pays the supplier directly

on behalf of the automobile dealer and no cash is disbursed by the dealer until the

inventory is sold. As discussed in the nonauthoritative guidance in AICPA Technical

Q&As Section 1300.16, the dealer reports purchases as increases in inventory and

trade loans (a noncash transaction), with repayments of the trade loans presented

within operating activities in the statement of cash flows.

However, when the finance entity is not a subsidiary of a supplier (i.e., a

third party), the amounts financed are not trade loans; rather, they are third-party

loans.1 As a result, they should be reflected as cash transactions in the dealer’s

statement of cash flows as follows:

-

Unrelated finance entity remits proceeds to the supplier (on behalf of the dealer) — The dealer should present this transaction as a financing cash inflow (to reflect the amount “received” from the third-party loan) and an operating cash outflow (to reflect the amount “paid” to purchase inventory).

-

Dealer repays loan to finance company — The dealer should present this transaction as a financing cash outflow.

This principle is applicable in other industries that may not have inventory financing arrangements. For example, a company may purchase real estate by taking out a mortgage with a third-party financing entity. At the closing of the purchase transaction, the third-party lender electronically wires cash directly to an escrow account, which in turn is wired directly to the seller. The cash from the mortgage does not get deposited into the company’s bank account (or get paid out of the company’s bank accounts) since it is paid directly from the lender to the seller as part of closing escrow. Since the third-party lender is acting as the buyer’s agent and transfers the proceeds of the mortgage directly to the escrow agent on behalf of the buyer, the substance of the transaction is that the buyer received the proceeds of the mortgage as a financing cash inflow and disbursed the purchase price of the real estate as an investing cash outflow. Accordingly, the transaction should be presented in such a manner in the company’s statement of cash flows.

Footnotes

1

This issue was discussed by an SEC staff member at the 2005

AICPA Conference on Current SEC and PCAOB Developments.

7.3 Stock Compensation

Because the receipt of employee services in exchange for a share-based payment award is a noncash item, the granting of such awards is not presented in the statement of cash flows.

However, in presenting cash flows under the indirect method, an entity would present the compensation cost recognized in net income in each reporting period as a reconciling item in arriving at cash flows from operations. In addition, an entity must present any cash paid by employees (e.g., the exercise price) to the entity for such awards as cash inflows from financing activities.

However, the complexity of stock compensation arrangements often leads to

additional presentation issues related to an entity’s statement of cash flows. This

section discusses the following presentation issues:

-

Cash received upon early exercise of a share-based payment award.

-

Income tax effects of share-based payment awards.

-

Settlement of equity-classified share-based payment awards.

-

Settlement of liability-classified share-based payment awards.

-

Remittances of statutory withholding on share-based payment awards.

For more information about the accounting for share-based payment awards, see

Deloitte’s Roadmap Share-Based

Payment Awards.

7.3.1 Cash Received Upon Early Exercise of a Share-Based Payment Award

An early exercise refers to an employee’s ability to change his or her tax position by exercising a share-based payment award and receiving shares before the completion of the requisite service period (i.e., before the award is vested). The early exercise of an award results in the employee’s deemed ownership of the shares for U.S. federal income tax purposes, which in turn results in the commencement of the holding period (under the tax law), allowing any subsequent appreciation in the value of the shares received (and realized upon the sale of those shares) to be taxed at a capital gains rate rather than an ordinary income tax rate.

Under ASC 718, an early exercise of a share-based payment award is not

considered substantive for accounting purposes (see ASC 718-10-55-31(a)). That

is, the share is not considered “issued” because the employee is still required

to perform the requisite service to earn the share. Although the share is not

considered issued, the cash received from the early exercise represents proceeds

from the issuance of an equity instrument and would still be classified as a

financing activity. As a result, such cash would be recognized as a cash inflow

from financing activities under ASC 230-10-45-14(a).

In addition, as defined in ASC 230-10-20, cash flows from operating activities are “generally the cash effects of transactions and other events that enter into the determination of net income.” A transaction in which cash is received from an employee who elects to early exercise an option is not the type of transaction that enters into the determination of net income.

7.3.2 Income Tax Effects of Share-Based Payment Awards

Before the issuance of ASU 2016-09, entities were required to present any realized

excess or deficient tax deductions (“excess tax benefit” or “tax deficiency”) on

a gross basis as separate components of financing activities.2 However, ASU 2016-09 clarified that the income tax effect of any excess

tax benefit or tax deficiency is recognized in the income statement; therefore,

excess tax benefits or tax deficiencies represent operating activities in a

manner consistent with other cash flows related to income taxes.

7.3.3 Settlement of Equity-Classified Share-Based Payment Awards

When settling an equity-classified share-based payment award, an entity presents the settlement in its statement of cash flows on the basis of whether the amount paid to settle the award is greater than or less than the fair-value-based measure of the award on the settlement date:

- Amount paid to settle the award does not exceed the fair-value-based measure of the award on the settlement date — In accordance with ASC 718-20-35-7, if the cash paid to repurchase the equity-classified award does not exceed the fair-value-based measure of the award on the repurchase date, the cash paid to repurchase the award is charged to equity. That is, repurchase of the equity-classified award is viewed as reacquisition of the entity’s equity instruments. Accordingly, the cash paid to reacquire the entity’s equity instruments is presented as a cash outflow for financing activities under ASC 230-10-45-15(a), which indicates that payments of dividends or other distributions to owners, including outlays to reacquire the entity’s equity instruments, are cash outflows for financing activities.

- Amount paid to settle the award exceeds the fair-value-based measure of the award on the settlement date — If the cash paid to repurchase the equity-classified award exceeds the fair-value-based measure of the award on the repurchase date, the cash paid in excess of the fair-value-based measure of the award is viewed as compensation for additional employee services and is recognized as additional compensation cost. Accordingly, if the equity-classified award is repurchased for an amount in excess of the fair-value-based measure, the portion of the cash paid to reacquire the entity’s equity instruments that equals the fair-value-based measure of the award is presented as a cash outflow for financing activities under ASC 230-10-45-15(a). The portion of the cash paid in excess of the fair-value-based measure, for additional employee services, is presented as a cash outflow for operating activities under ASC 230-10-45-17(b), which notes that cash payments to employees for services are cash outflows for operating activities.

Example 7-2

Company A is making a tender offer to repurchase $20 million of common stock in

the aggregate (the stock was originally distributed as

share-based compensation awards) from its current

employees. On the basis of an independent third-party

valuation, A concludes that the purchase price paid to

the employees for the common stock exceeds the fair

value of the common stock by a total of $4.5 million. In

accordance with ASC 718-20-35-7, the amount paid to

employees up to the fair value of common stock acquired

should be recognized in equity as a treasury stock

transaction and should therefore be presented as a cash

outflow for financing activities. The $4.5 million that

was paid in excess of the fair value of the common stock

constitutes compensation expense and is therefore

presented as a cash outflow for operating

activities.

7.3.4 Settlement of Liability-Classified Share-Based Payment Awards

In accordance with ASC 718-30, the grant-date fair-value-based measure and any

subsequent changes in the fair-value-based measure of a liability-classified

award through the date of settlement are recognized as compensation cost.

Accordingly, the cash paid to settle the liability-classified award is

effectively payment for employee services and is presented as a cash outflow for

operating activities under ASC 230-10-45-17(b).

Note that an entity may enter into an agreement to repurchase (or offer to repurchase) an equity-classified award for cash. Depending on the facts and circumstances, the agreement to repurchase (or offer to repurchase) may be accounted for as either (1) a settlement of the equity-classified award or (2) a modification of the equity-classified award that changes the award’s classification from equity to liability, followed by a settlement of the now liability-classified award.

If the agreement to repurchase (or offer to repurchase) is considered a

settlement of an equity-classified award, the cash paid to reacquire the

entity’s equity instruments is presented in a manner consistent with the

discussion in the previous section. If the agreement to repurchase (or offer to

repurchase) is considered a modification of the equity-classified award that

changes the award’s classification from equity to liability, the cash paid to

settle the liability-classified award should be presented in the statement of

cash flows in a manner similar to the conclusion above. That is, under ASC

230-10-45-17(b), the cash paid to settle the liability-classified award is

effectively payment for employee services and is presented as a cash outflow for

operating activities.

7.3.5 Remittances of Statutory Withholding on Share-Based Payment Awards

Regardless of whether the employer meets the employee’s statutory tax

withholding requirement for liability-classified or equity-classified

share-based payment awards through either a net settlement feature or a

repurchase of shares upon exercise of an employee share option (or vesting of a

nonvested share), an entity must account for the withholding as two transactions

in the statement of cash flows. That is, in substance, this transaction is (1) a

gross issuance of shares and (2) a repurchase of the amount of shares needed to

satisfy the employee’s statutory tax withholding requirement. Therefore, the

presentation in the statement of cash flows must also reflect the two

transactions.

First, the gross issuance of shares is presented as a financing activity. For example, the cash received for an employee share option as payment for the exercise price of the award is classified as a financing cash inflow. In contrast, for a nonvested share award, because no cash is received from the employee, the gross issuance of shares is presented as a noncash financing activity.

In the second step, when an employee elects to have shares withheld to satisfy

its statutory withholding tax obligation, the employer is deemed to have

repurchased a portion of the shares that were received by the employee in the

first step. While the employee does not receive cash directly, the employer has,

in substance, repurchased shares from the employee and remitted the cash

consideration to the tax authority on the employee’s behalf. Because the cash

payment is related to a repurchase of stock, it is presented as a financing cash

outflow.

In some circumstances, an exercise of the award may occur in one reporting

period while the amount withheld for tax purposes may not be remitted to the tax

authority by an employer, on behalf of the employee, until a subsequent

reporting period. In these circumstances, for the second step of the

transaction, the financing cash outflow is reported in the period in which the

cash is paid to the tax authority. In the initial reporting period, the employer

has issued the gross amount of shares and is deemed to have repurchased the

requisite number of shares needed to satisfy the employee’s statutory tax

withholding requirement by issuing a note payable to the employee. The note

payable issued for the repurchase amount is viewed as a noncash event that has

no impact on the statement of cash flows. In the subsequent reporting period,

the employer remits the payment for the note payable; however, the employee

requests that the amount be remitted to the tax authority on the employee’s

behalf instead of directly to the employee. This results in the financing cash

outflow.

Example 7-3

An entity grants 1,000 nonvested shares to an employee. The plan allows the

employer to net-settle the award to cover the statutory

tax withholding requirement. Upon vesting, the entity

withholds 250 shares to cover the statutory withholding

requirement and issues the employee the remaining 750

shares. For cash flow purposes, the entity must account

for this transaction as (1) the gross issuance of 1,000

shares and (2) the repurchase of 250 shares to satisfy

the statutory withholding requirement. Because no cash

is received from the employee for the nonvested share

award, the gross issuance of the 1,000 shares is

classified as a noncash financing activity. The

“repurchase,” through the net settlement feature, of the

250 shares to satisfy the statutory withholding

requirement is classified as a financing cash outflow.

The contemporaneous “receipt of cash,” through the net

settlement feature, from the employee and the remittance

of cash by the entity to the tax authority have no net

impact on the statement of cash flows.

Connecting the Dots

In June 2018, the FASB issued ASU 2018-07,3 which simplifies the accounting for share-based payments granted

to nonemployees for goods and services. Under the ASU, most of the

guidance on share-based payments to nonemployees is aligned with the

requirements for share-based payments granted to employees. As a result,

much of the guidance in ASC 718, including most of its requirements

related to classification and measurement of share-based payment awards

to employees, will apply to nonemployee share-based payment

arrangements. The ASU also revises ASC 230-10-45-15(a) to extend the

requirement to classify, as a financing activity, a repurchase of shares

to satisfy an employee’s statutory tax withholding obligation related to

share-based payments granted to nonemployees.

Footnotes

2

ASU 2016-09 removed ASC 230-10-45-14(e), which stated

that the following was a cash inflow from financing activities: “Cash

retained as a result of the tax deductibility of increases in the value

of equity instruments issued under share-based payment arrangements that

are not included in the cost of goods or services that is recognizable

for financial reporting purposes. For this purpose, excess tax benefits

shall be determined on an individual award (or portion thereof) basis.”

Such excess tax benefits were the same amounts that an entity was

required to show as an operating cash outflow in accordance with ASC

230-10-45-17(c), which the ASU also removed.

3

The amendments in ASU 2018-07 are effective for

public business entities for fiscal years beginning after

December 15, 2018, including interim periods within those fiscal

years. For all other entities, the amendments are effective for

fiscal years beginning after December 15, 2019, and interim

periods within fiscal years beginning after December 15, 2020.

Early adoption is permitted, provided that the adoption date is

no earlier than the date on which an entity adopts ASC 606.

7.4 Derivatives

ASC 230-10

Cash Receipts and

Payments Related to Hedging Activities

45-27 Generally, each cash receipt or payment is to be classified according to its nature without regard to whether it stems from an item intended as a hedge of another item. For example, the proceeds of a borrowing are a financing cash inflow even though the debt is intended as a hedge of an investment, and the purchase or sale of a futures contract is an investing activity even though the contract is intended as a hedge of a firm commitment to purchase inventory. However, cash flows from a derivative instrument that is accounted for as a fair value hedge or cash flow hedge may be classified in the same category as the cash flows from the items being hedged provided that the derivative instrument does not include an other-than-insignificant financing element at inception, other than a financing element inherently included in an at-the-market derivative instrument with no prepayments (that is, the forward points in an at-the-money forward contract) and that the accounting policy is disclosed. If the derivative instrument includes an other-than-insignificant financing element at inception, all cash inflows and outflows of the derivative instrument shall be considered cash flows from financing activities by the borrower. If for any reason hedge accounting for an instrument that hedges an identifiable transaction or event is discontinued, then any cash flows after the date of discontinuance shall be classified consistent with the nature of the instrument.

In accordance with the general principle in ASC 230-10-45-27, the presentation of

cash flows associated with derivatives depends on the nature of the underlying

instrument. Such presentation would therefore be affected by whether the instrument

contains an other-than-insignificant financing element, regardless of whether the

derivative is a hedging instrument. In situations in which an arrangement contains

an other-than-insignificant financing element, the borrower and lender under the

derivative instrument classify cash flows related to the derivative instrument as

financing activities and investing activities, respectively.

The table below summarizes common cash flow classifications for various derivative

transactions. These classifications are discussed in more detail throughout this

section.

|

Derivative Instrument

|

Classification of the Derivative’s Cash

Flows

|

|---|---|

|

Derivatives with an other-than-insignificant

financing element at inception

|

Financing activities (for the deemed

borrower4) and generally investing activities (for the deemed

lender)

|

|

Derivatives acquired or originated for

trading purposes

|

Operating activities

|

|

Hedging derivatives

|

Investing activities

or

In the same category as the cash flows from

the item being hedged

|

|

Nonhedging derivatives

|

Investing activities

or

In accordance with the nature of the

derivative instrument as it is used in the context of the

entity’s business (if an economic hedge)

|

7.4.1 Determining Whether an Other-Than-Insignificant Financing Element Exists

ASC 815-10

45-11 An instrument accounted

for as a derivative instrument under this Subtopic that,

at its inception, includes off-market terms, or requires

an up-front cash payment, or both often contains a

financing element. Identifying a financing element

within a derivative instrument is a matter of judgment

that depends on facts and circumstances.

45-12 If an

other-than-insignificant financing element is present at

inception — other than a financing element inherently

included in an at-the-market derivative instrument with

no prepayments (that is, the forward points in an

at-the-money forward contract) — then the borrower shall

report all cash inflows and outflows associated with

that derivative instrument in a manner consistent with

financing activities as described in paragraphs

230-10-45-14 through 45-15.

45-13 An at-the-money

plain-vanilla interest rate swap that involves no

payments between the parties at inception would not be

considered as having a financing element present at

inception even though, due to the implicit forward rates

derived from the yield curve, the parties to the

contract have an expectation that the comparison of the

fixed and variable legs will result in payments being

made by one party in the earlier periods and being made

by the counterparty in the later periods of the swap's

term.

45-14 If a derivative

instrument is an at-the-money or out-of-the-money option

contract or contains an at-the-money or out-of-the-money

option contract, a payment made at inception to the

writer of the option for the option's time value by the

counterparty shall not be viewed as evidence that the

derivative instrument contains a financing element.

45-15 In contrast, if the

contractual terms of a derivative instrument have been

structured to ensure that net payments will be made by

one party in the earlier periods and subsequently

returned by the counterparty in the later periods of the

derivative instrument's term, that derivative instrument

shall be viewed as containing a financing element even

if the derivative instrument has a fair value of zero at

inception.

ASC 815-10-45-12 requires the deemed borrower of a financing

element in a derivative instrument to classify cash flows associated with the

derivative instrument as financing activities in accordance with ASC

230-10-45-14 and 45-15 if “an other-than-insignificant financing element is

present at inception — other than a financing element inherently included in an

at-the-market derivative instrument with no prepayments (that is, the forward

points in an at-the-money forward contract).” For example, an up-front payment

that does not represent compensation for the initial time value associated with

an at-the-money or out-of-the-money option may represent a financing element. To

determine whether a financing element is other than insignificant, an entity

often needs to use judgment and consider its specific facts and circumstances.

We have observed in practice that when making this determination, some entities

have compared the financing element with a reference amount (e.g., a comparison

to the present value of an at-the-market derivative’s fully prepaid amount).

ASC 230-10-45-27 requires an entity to evaluate whether an

other-than-insignificant financing element exists “at inception,” which is

generally the date on which the entity entered into the derivative instrument.

However, a modification made to the terms of the derivative instrument that

changes the timing or amount of cash flows is in substance a new derivative

instrument. Accordingly, the modification date would represent a new inception

date, and an entity would need to evaluate whether an other-than-insignificant

financing element exists on such date, if applicable. However, in the context of

derivative instruments modified as a result of the elimination of a benchmark

interest rate reference, we believe that an entity would not need to use the

modification date as the inception date if the entity elects to apply the

contract modification practical expedient provided under ASC 848.5 Therefore, an entity that elects to apply such practical expedient would

not need to reassess whether an other-than-insignificant financing element

exists on the modification date and, as a result, no reassessment to the cash

flow classification would be necessary.

7.4.2 Derivatives With an Other-Than-Insignificant Financing Element at Inception

Under ASC 230-10-45-27, if a derivative includes “an

other-than-insignificant financing element at inception, other than a financing

element inherently included in an at-the-market derivative instrument with no

prepayments (that is, the forward points in an at-the-money forward contract),”

the deemed borrower classifies all cash flows associated with that derivative

instrument as financing activities. While ASC 230 addresses the deemed

borrower’s classification of cash flows on a derivative with an

other-than-insignificant financing element at inception, it does not explicitly

address the deemed lender’s classification of such cash flows. In a

manner consistent with the guidance in ASC 230-10-45-27, it is appropriate for a

deemed lender to classify cash flows related to a derivative with an

other-than-insignificant financing element at inception as investing activities;

however, that classification may not be required in all circumstances. The

example below illustrates the classification of cash flows related to an

interest rate swap that is not a hedging derivative and contains an

other-than-insignificant financing element.

Example 7-4

In year 1, Entity A issues a five-year, $100 million

variable-rate corporate bond for which A pays the

secured overnight financing rate (SOFR) annually. To

minimize its exposure to fluctuations in interest rates,

A also enters into an interest rate swap agreement with

Bank B. Under the terms of the agreement, the fixed leg

of the interest rate swap is 8 percent, while the

interest rate at the inception of the instrument is 5

percent. Therefore, B will pay a premium to A at

inception. That is, A is deemed to borrow the amount of

the premium that would be repaid through higher payments

under the derivative instrument. The interest rate swap

is not designated as a hedging derivative.

Entity A concludes that the premium received at inception

represents a financing element that is other than

insignificant. Because the interest rate swap is not

designated as a hedging derivative and contains an

other-than-insignificant financing element at inception,

A should generally classify the cash flows associated

with the interest rate swap as financing

activities in its statement of cash flows since

A is the deemed borrower of the premiums received for

the swap. By contrast, B is considered the deemed lender

since B is making the premium payment at inception.

Therefore, B should classify the cash flows associated

with the interest rate swap as investing

activities in its statement of cash flows.

Note that A’s classification of the cash flows related to

the interest rate swap in this example would not be

affected if A had concluded that the instrument were a

hedging derivative.

The example below illustrates the classification of cash flows related to an

interest rate swap that is not a hedging derivative and does not contain an

other-than-insignificant financing element.

Example 7-5

Assume the same facts as in Example

7-4, except that Entity A concludes that

the interest rate swap does not contain an

other-than-insignificant financing element at inception.

Accordingly, the cash flows associated with the interest

rate swap should, on the basis of the guidance discussed

in Section 7.4.5, be classified either as

investing activities or in a

manner consistent with the nature of the derivative

instrument as it is used in the context of the entity’s

business. The interest rate swap arrangement derives its

periodic cash flows from an interest rate underlying and

was entered into to alter the entity’s periodic interest

payments. Therefore, because the cash payments for

interest are classified as operating

activities, it would be acceptable for A to

classify the cash flows from the derivative as operating

activities given the nature of the derivative instrument

as it is used in the context of the entity’s

business.

7.4.3 Derivatives Acquired or Originated for Trading Purposes

In accordance with ASC 230-10-45-19 through 45-21, cash receipts and payments

resulting from purchases and sales of securities, loans, and other assets that

are acquired specifically for resale must be classified as operating activities.

Thus, a trading entity that acquires derivatives as part of its trading business

should classify the cash flows from those derivatives as operating activities

(provided that those derivatives do not contain an other-than-insignificant

financing element at inception).

7.4.4 Hedging Derivatives

Under ASC 230-10-45-27, a cash receipt or payment related to a hedging

derivative should generally “be classified according to its nature without

regard to whether it stems from an item intended as a hedge of another item. For

example, the proceeds of a borrowing are a financing cash inflow even though the

debt is intended as a hedge of an investment, and the purchase or sale of a

futures contract is an investing activity even though the contract is intended

as a hedge of a firm commitment to purchase inventory.”

However, an entity may classify the cash flows from a derivative instrument that

is accounted for as a fair value hedge or a cash flow hedge (and that does not

contain an other-than-insignificant financing element at inception) in the same

category as the cash flows from the items being hedged as long as the entity has

elected and disclosed such classification as its accounting policy. Otherwise,

the entity should classify the cash flows from the derivative as an investing

activity under ASC 230-10-45-27. If periodic settlement payments are required

for the hedging derivative in a fair value or cash flow hedging relationship,

the cash flow classification of any termination or settlement payment should

generally be consistent with the classification of the periodic settlements.

If a derivative instrument (that does not contain an other-than-insignificant

financing element at inception) is designated as a hedging instrument in a hedge

of the foreign currency exposure related to a net investment in a foreign

operation, the cash flows from the derivative, including the cash flows

associated with the forward elements of the derivative, should generally be

classified as cash flows related to investing activities. This classification is

consistent with both the nature of the derivative and the nature of the hedged

item. If, however, an entity assesses the effectiveness of the net investment

hedging relationship by using the spot method, it is also acceptable for the

entity to classify the cash flows associated with the excluded component (e.g.,

the periodic settlement payments in a cross-currency interest rate swap)

according to their nature (i.e., as operating activities consistent with the

classification of interest payments and receipts) provided that such

classification is applied consistently and disclosed. However, the cash flow

classification of any termination or settlement payment for the derivative

should be consistent with the nature of the hedged item (i.e., as an investing

activity, because sales or purchases of the net investment would be an investing

activity).

The examples below illustrate an entity’s classification approaches when its accounting policy is to classify cash flows in the same category as the cash flows from the items being hedged.

Example 7-6

Entity A designates a forward-starting swap as a hedge of the forecasted

issuance of fixed-rate debt. The entity plans to issue

debt at par at the then-current market interest rate

(i.e., the market interest rate as of the date the debt

is issued) and will therefore have no variability in

debt proceeds; however, each of the probable interest

payments resulting from the debt is exposed to

variability up until the date of issuance. Accordingly,

the forward-starting swap is a hedge of the interest

payments, and the related cash flows should be

classified as operating activities in the statement of

cash flows.

Example 7-7

Entity B designates a forward-starting swap as a hedge of the forecasted

issuance of fixed-rate debt. The entity plans to issue

debt at a stipulated, fixed interest rate (4 percent,

regardless of current market rates as of the date the

debt is issued). As a result, the debt proceeds will be

variable (i.e., the debt will be issued at a discount or

a premium) because market rates will change during the

period leading up to the actual debt issuance date. The

interest payments are not exposed to variability (since

the entity has already determined the coupon it intends

to pay). Therefore, the forward-starting swap is a hedge

of the forecasted debt proceeds, and the cash flows on

the derivative should be classified as financing

activities in the statement of cash flows.

7.4.5 Nonhedging Derivatives

If a nonhedging derivative (1) does not contain an

other-than-insignificant financing element at inception and (2) was not acquired

or originated for trading purposes, as addressed in Sections

7.4.1 and 7.4.3, respectively, an entity

should apply the guidance discussed below.

Cash flows pertaining to physically settled derivatives related

to the entity’s ongoing revenue-producing and cost-generating activities should

generally be classified as operating activities in accordance with ASC

230-10-45-16(a) and ASC 230-10-45-17(a). For all other nonhedging derivatives,

ASC 230 does not specifically require an entity to classify cash flows as

investing activities; thus, an entity can make an accounting policy election to

apply either of the following approaches to nonhedging derivatives:

-

Classify the cash flows related to all other nonhedging derivatives as investing activities.

-

Classify the cash flows related to all other nonhedging derivatives in accordance with the nature of the derivative instrument as it is used in the context of the entity’s business.

When the cash flows associated with nonhedging derivatives are

material, an entity should disclose its policy for classifying the cash flows

associated with such instruments.

The table below outlines acceptable classifications for

nonhedging derivatives in the statement of cash flows. Note that in the

examples, none of the derivatives contain an other-than-insignificant financing

element at inception. Furthermore, when alternative classifications are

acceptable, the entity’s accounting policy election regarding the classification

of cash flows related to other nonhedging derivatives will dictate the proper

classification.

|

Derivative Example

|

Classification of the Derivative’s Cash

Flows

|

|---|---|

|

A manufacturing entity enters into a

receive-variable, pay-fixed interest rate swap in

conjunction with the issuance of a floating-rate debt

instrument. The term of the interest-rate swap coincides

with the term of the debt, and the variable leg on the

swap is the same as the floating-rate index on the debt.

The interest-rate swap was entered into to alter the

economic interest cost related to the entity’s

floating-rate debt.

|

Investing activities or operating

activities.

Classification as an investing activity

is consistent with ASC 230-10-45-27.

Classification as an operating activity

is consistent with the nature of the derivative

instrument as it is used in the context of the entity’s

business. The derivative instrument derives its periodic

cash flows on the basis of an interest rate underlying

and was entered into to alter the entity’s interest

costs. Cash payments for interest are classified as

operating activities in accordance with ASC

230-10-45-17(d).

|

|

A real estate company enters into a

variable-rate debt agreement that requires it to make

interest payments indexed to SOFR and pay a spread

quarterly. To limit its exposure to interest rates above

8 percent, which is above the current SOFR plus the

spread, the company also enters into an interest rate

cap arrangement. The company pays a premium to enter

into the interest rate cap arrangement that is not

considered an other-than-insignificant financing

element.

|

Investing activities or operating activities.

Classification as an investing activity

is consistent with the guidance in ASC 230-10-45-27.

Classification as an operating activity

is consistent with the nature of the derivative

instrument as it is used in the context of the entity’s

business. The derivative instrument was entered into to

mitigate a potential increase in the entity’s interest

cost payments. Cash payments for interest costs are

classified as operating activities in accordance with

ASC 230-10-45-17(d).

|

|

A financial institution enters into a

foreign currency forward contract that requires it to

pay USD and receive EUR. The forward contract matures on

the same date as the maturity of the principal amount of

the institution’s EUR-denominated long-term debt. The

forward contract was entered into to alter the

USD-equivalent amount that must be paid at maturity of

the debt.

|

Investing activities or financing

activities.

Classification as an investing activity

is consistent with ASC 230-10-45-27.

Classification as a financing activity

is consistent with the nature of the derivative

instrument as it is used in the context of the entity’s

business. The derivative instrument derives its cash

flows on the basis of a currency underlying and was

entered into to alter the amount payable upon maturity

of the institution’s debt. Cash payments made to repay

amounts borrowed are classified as financing activities

in accordance with ASC 230-10-45-15(b).

|

|

A power generator that uses a gas-fired

plant to generate electricity enters into physically

settleable forward gas purchase contracts that are

within the scope of ASC 815. The gas purchased is used

to run the power plant.

|

Operating activities.

Since the derivative is physically

settled and the gas purchased is used to operate the

power plant, cash flows related to the derivative should

be classified as an operating activity. Otherwise, the

power generator could potentially reflect a significant

amount of its cost-generating activities as investing

activities.

|

|

A power generator that uses a gas-fired

plant to generate electricity enters into futures

contracts on gas to economically hedge its exposure to

gas prices. The power generator does not plan to take

delivery of the gas.

|

Investing activities or operating

activities.

Classification as an investing activity

is consistent with ASC 230-10-45-27.

Classification as an operating activity

is consistent with the nature of the derivative

instrument as it is used in the context of the entity’s

business. The derivative may be considered part of the

ongoing revenue-producing and cost-generating activities

of the power generator. Cash receipts and payments

related to sales and costs of goods sold are classified

as operating activities in accordance with ASC

230-10-45-16 and 45-17.

Note that since the derivative will be

net settled, the power generator is not required to

classify the cash flows as an operating activity.

|

|

An Internet advertising agency enters

into a one-year futures contract on crude oil. The

agency expects that crude oil prices will increase

between the trade date and maturity date of the futures

contract, resulting in a gain upon settlement. The

agency does not plan to take delivery of the crude oil.

The futures contract is not held for trading

purposes.

|

Investing activities.

Classification as an investing activity

is consistent with ASC 230-10-45-27. Such classification

is also consistent with the nature of the derivative

instrument as it is used in the context of the entity’s

business. The crude oil futures contract was entered

into for speculative or investment purposes.

|

|

In year 1, Entity D issues a 10-year, $400 million

variable-rate debt instrument. Entity D pays SOFR plus a

spread of 200 basis points annually. To hedge its

exposure to interest rate risk, D also enters into a

receive-variable, pay-fixed interest rate swap

agreement.

In year 3, D terminated the interest rate swap

arrangement.

|

Year 1:

Investing activities or operating

activities.

Classification as an investing activity is consistent

with the guidance in ASC 230-10-45-27.

Classification as an operating activity is consistent

with the nature of the derivative instrument as it is

used in the context of the entity’s business. The

derivative instrument derives its periodic cash flows on

the basis of an interest rate underlying and was entered

into to alter the entity’s interest costs. Cash payments

for interest are classified as operating activities in

accordance with ASC 230-10-45-17(d).

Year 3:

In a manner consistent with the classification of the

periodic settlements, D should classify cash flows

associated with the termination of the interest rate

swap as investing activities or operating

activities.

|

Footnotes

4

The “deemed borrower” refers to the

party that benefits from a financing element in a

derivative instrument in early periods of the

instrument’s term. For example, a party that

receives a premium upon entering into an arrangement

because of the arrangement’s off-market terms is

considered to be the deemed borrower.

5

See Section 8.2.2.2 of Deloitte’s Roadmap

Hedge Accounting for more

information about this practical expedient.

7.5 Business Combinations

Cash flows related to the purchases and sales of businesses, PP&E, and other

productive assets are presented as investing activities in the statement of cash

flows. In a business combination, all cash paid to purchase the business is

presented as a single line item in the statement of cash flows, net of any cash and

cash equivalents acquired (including acquired restricted cash and restricted cash

equivalents after the adoption of ASU 2016-18). That is, changes in the individual

assets acquired and liabilities assumed that occur on the acquisition date are no

longer reflected as separate line items in the statement of cash flows. After an

acquisition, the cash flows of the acquirer and acquiree are combined and presented

in a consolidated statement of cash flows.

An entity may also need to consider other financial reporting implications of a

business combination depending on the nature and terms of the transaction. For

example, any noncash effects of a business combination, such as an acquisition

involving noncash consideration (as described in Example

5-2), must be disclosed in a narrative format or summarized in a

schedule.

For additional considerations related to an entity’s accounting for a business

combination, see Deloitte’s Roadmap Business Combinations.

7.5.1 Presentation of Acquisition-Related Costs

When consummating a business combination, an acquirer frequently incurs acquisition-related costs such as advisory, legal, accounting, valuation, and professional and consulting fees. Except for certain debt and equity issuance costs, ASC 805 requires that an entity expense all such acquisition-related costs as incurred. The costs of issuing debt or equity securities as part of a business combination are recognized in accordance with other applicable accounting literature.

In the deliberations before the issuance of Statement 141(R) (codified in ASC 805), the FASB determined that acquisition-related costs are not considered part of the fair value exchange between the buyer and seller of the business; rather, they are separate transactions in which the buyer pays for services that it receives. Further, the definition of “operating activities” in the ASC master glossary states, in part, that “[c]ash flows from operating activities are generally the cash effects of transactions and other events that enter into the determination of net income.” Because acquisition-related costs accounted for under ASC 805 are expensed and affect net income, these costs should be reflected as operating cash outflows in the statement of cash flows.

7.5.2 Settlement of Acquired Liabilities After a Business Combination

After an acquisition, the acquirer may make payments to settle a liability legally assumed in a business combination. The cash outflow related to the settlement of the liability could be classified as an operating, investing, or financing activity depending on the nature of the payment. The payment should be classified as it would have been in the absence of the business combination. For example:

- If the payment was for inventory purchased on account, it would represent an operating cash outflow.

- If the payment was for PP&E that was purchased on account and was paid within three months of its original purchase date, it would represent an investing cash outflow.

- If the payment was in connection with a debt obligation legally assumed in an acquisition that remained outstanding after the acquisition, it would represent a financing cash outflow. However, as described below, if the payment is related to debt extinguished in conjunction with a business combination, the entity must consider certain facts and circumstances of the business combination to determine the appropriate presentation in its statement of cash flows.

7.5.3 Debt in a Business Combination

An acquirer may sometimes use cash to settle debt of the acquiree at or close to the acquisition date. In such cases, it is necessary to determine whether the cash distributed should be reported as consideration transferred to effect the acquisition or as cash paid to settle the debt assumed in the acquisition. While cash paid on the acquisition date to settle debt of the acquiree is generally reported as consideration transferred, cash paid close to the acquisition date to settle debt of the acquiree might also be reported as consideration transferred if the acquirer is deemed not to have assumed the risks inherent in the debt (e.g., when the separation of the payment from the acquisition date is more administrative).

The classification in the statement of cash flows of cash paid to settle the

acquiree’s debt in a business combination should be consistent with the

acquirer’s treatment of the debt in acquisition accounting (i.e., whether the

debt was treated as a liability assumed in acquisition accounting). If the

acquirer concludes that it assumes the acquiree’s debt as part of the business

combination, the acquirer will generally present the extinguishment as a

financing activity (in a manner consistent with how it would present the

repayment of a debt obligation outside of a business combination). Conversely,

if the acquirer concludes that it does not assume the acquiree’s debt as part of

the business combination that was subsequently extinguished, the acquirer will

generally present the extinguishment as an investing activity (in a manner

consistent with how it would present cash consideration paid in a business

combination). The example below illustrates an acquisition in which the acquirer

does not assume the acquiree's debt.

Example 7-8

Company A acquires Company B in a business combination. Before the acquisition, B had $1 million in outstanding debt owed to a third-party bank. Company A pays the seller $5 million in cash and repays the $1 million debt upon the closing of the business combination. Company A concludes that it did not assume B’s debt (i.e., that it repaid the debt on B’s behalf). As of the acquisition date, B’s net assets recognized in accordance with ASC 805 are $4 million. Company A calculates the goodwill resulting from the acquisition of B as follows:

Because A did not assume B’s debt, the total consideration transferred is $6 million in cash. Therefore, A should present the $6 million as an investing outflow in its statement of cash flows.

In the example below, the acquirer has assumed the acquiree's debt.

Example 7-9

Assume the same facts as in the example above, except that Company A concludes

that it assumed Company B’s debt. As a result, B’s net

assets recognized in accordance with ASC 805 are $3

million (i.e., $4 million less $1 million in debt).

Company A calculates the goodwill resulting from the

acquisition of B as follows:

Because A assumed B’s debt, the consideration transferred is $5 million in cash paid to the seller, and the $1 million to repay B’s debt is a liability assumed in the acquisition accounting. Therefore, A should present $5 million as an investing outflow and $1 million as a financing outflow in its statement of cash flows.

7.5.4 Contingent Consideration in a Business Combination

ASC 805 requires the acquirer to recognize the acquisition-date fair value of the contingent consideration arrangement as part of the consideration transferred in exchange for the acquiree. The contingent consideration arrangement is classified either as a liability or as equity in accordance with applicable U.S. GAAP.

7.5.4.1 Contingent Consideration Classified as a Liability

If the acquiring entity determines that the contingent consideration arrangement

should be classified as a liability, the initial fair value of the

contingent consideration as of the acquisition date should be reflected as a

noncash investing activity. In accordance with

ASC 230-10-50-3, this arrangement should be either disclosed narratively or

summarized in a schedule because no cash consideration is transferred on the

acquisition date. It should not be reflected in investing activities. In

subsequent periods, the contingent consideration liability must be

remeasured at fair value as of each reporting date until the contingency is

resolved, with the changes recognized as an expense in the determination of

earnings (unless the change is the result of a measurement-period adjustment

or the arrangement is a hedging instrument for which ASC 815 requires

changes to be recognized in OCI). Because the subsequent fair value

adjustment enters into the determination of the acquiring entity’s net

income and is a noncash item, it should be reflected as a reconciling item

between net income and cash flows from operating activities in the statement

of cash flows.

If the contingent consideration is satisfied in either cash or cash

equivalents upon resolution of the contingency, the classification of

payments made to settle the contingent consideration liability should be

determined on the basis of when such payments are made in relation to the

date of the business combination. Essentially, classification of the

payments depends on whether they are made soon after the acquisition in a

business combination transaction. While ASC 230 does not define the term

“soon after,” we generally believe that this term would apply to payments

made within three months or less of the acquisition date. This view is also

consistent with paragraph BC16 of ASU 2016-15, which states that “some Task

Force members believe that a payment for contingent consideration that was

made soon after a business combination is an extension of the cash paid for

the business acquisition (an investing activity), if that payment for

contingent consideration was made within a relatively short period of time

after the acquisition date (for example, three months or less).” Therefore,

because a payment made on or soon after the business combination date (to

settle the liability related to contingent consideration) is viewed as an

extension of the business combination, such payments made soon after the

date of the business combination are presented as investing activities in

the acquirer’s statement of cash flows in accordance with ASC

230-10-45-13(d).

Conversely, contingent consideration payments that are not made on the acquisition date or soon after the business combination are not viewed as an extension of the business combination. Therefore, such payments should be separated and presented as:

- Financing cash flows — The cash paid to settle the contingent consideration liability recognized at fair value as of the acquisition date (including measurement-period adjustments), less payments made soon after the business combination date, should be reflected as a cash outflow for financing activities in accordance with ASC 230-10-45-15(f).

- Operating cash flows — The cash payments not made soon after the business combination date that exceed those classified as financing activities should be reflected as a cash outflow for operating activities in accordance with ASC 230-10-45-17(ee).

As indicated in paragraph BC14 of ASU 2016-15, the separation of contingent consideration payments not made soon after the business combination date is consistent with the approach most entities used before the ASU was issued. Paragraph BC14 further notes that this approach is the one that is most closely aligned with certain principles in ASC 230.

These principles include:

- The cash paid to settle the contingent consideration liability recognized at fair value as of the acquisition date (including measurement-period adjustments) should be reflected as a cash outflow for financing activities in the statement of cash flows. Effectively, the acquiring entity financed the acquisition and the cash outflow therefore represents a subsequent payment of principal on the borrowing and should be reflected in accordance with ASC 230-10-45-15(f).

- The remaining portion of the amount received/paid (i.e., the changes in fair value of the contingent consideration liability after the acquisition date) should be reflected as a cash inflow/outflow from operating activities because the fair value adjustments were recognized in earnings. If the amount paid to settle the contingent consideration liability is less than the amount recorded on the acquisition date (i.e., the fair value of the contingent consideration decreased), the entity would only reflect the portion of the liability that was paid as a cash outflow for financing activities. The difference between the liability and the amount paid is a fair value adjustment. This adjustment enters into the determination of the acquiring entity’s net income and is a noncash item, so it should be reflected as a reconciling item between net income and cash flows from operating activities in the consolidated statement of cash flows.

Example 7-10

On December 1, 20X2, Company A (a calendar-year-end private company) acquires 100 percent of Company B for

$1 million. The purchase agreement includes a contingent consideration arrangement under which A agrees to pay additional cash consideration if the earnings of B (which will be operated as a separate subsidiary of A) exceed a specified target for the year ended December 31, 20X3. Company A classifies the contingent consideration arrangement as a liability and records the contingent consideration liability at its acquisition-date fair value amount, provisionally determined to be $500,000.

On April 15, 20X3, A finalizes its valuation of the contingent consideration liability. Therefore, A estimates the acquisition-date fair value of the contingent consideration liability to be $600,000 and records a measurement-period adjustment for $100,000 (the measurement-period adjustment related to facts and circumstances that existed as of the acquisition date), with an offsetting adjustment to goodwill.

Company B achieves the performance target for the year ended December 31, 20X3; accordingly, A determines that it must pay $750,000 to B’s former owners to settle the contingent consideration arrangement. For the year ended December 31, 20X3, A recognizes $150,000 ($750,000 – $600,000) in earnings to reflect the subsequent remeasurement of the contingent consideration liability to fair value. On January 31, 20X4, A settles the obligation.

No payments to settle the liability for contingent consideration were made soon after the business acquisition date.

Company A would present the following amounts in its statement of cash flows for the years ended:

- December 31, 20X2 — The provisional accrual of $500,000 would be reflected as a noncash investing activity and would be either disclosed narratively or summarized in a schedule.

- December 31, 20X3 — The adjustment to the provisional accrual of $100,000 would be reflected as a noncash investing activity and would be either disclosed narratively or summarized in a schedule. The subsequent remeasurement adjustment to the contingent consideration liability of $150,000 would be reflected as a reconciling item between net income and cash flows from operating activities.

- December 31, 20X4 — Of the $750,000 paid, $600,000 represents the amount to settle the contingent consideration liability recognized at fair value as of the acquisition date (including measurement-period adjustments) and should be reflected as a cash outflow for financing activities. The remaining portion of the $750,000 paid (i.e., the $150,000 change in fair value of the contingent consideration liability after the acquisition date) should be reflected as a cash outflow for operating activities because the fair value adjustments were recognized in earnings.

Example 7-11

Assume the same facts as in the example above except that when B achieves the

performance target for the year ended December 31,

20X3, A determines that it only needs to pay

$550,000 to B’s former owners to settle the

contingent consideration arrangement. For the year

ended December 31, 20X3, A recognizes a credit of

$50,000 ($550,000 – $600,000) in earnings to reflect

the subsequent remeasurement of the contingent

consideration liability to fair value.

Company A would present the same amounts as those in the example above in its

statement of cash flows for the year ended December

31, 20X2. Company A would then present the following

amounts for the years ended:

-

December 31, 20X3 — The adjustment to the provisional accrual of $100,000 would be reflected as a noncash investing activity and would be either disclosed narratively or summarized in a schedule. The subsequent remeasurement adjustment to the contingent consideration liability of $50,000 would be reflected as a reconciling item between net income and cash flows from operating activities.

-

December 31, 20X4 — The entire amount of the $550,000 paid represents the amount to settle the contingent consideration liability recognized at fair value as of the acquisition date (including measurement-period adjustments) and should be reflected as a cash outflow for financing activities.

7.5.4.2 Contingent Consideration Classified as Equity

If the acquiring entity determines that the contingent consideration arrangement

should be classified as equity, it is not required to remeasure the amount

recorded as of the acquisition date at fair value as of each reporting

period after the acquisition date. The initial recognition of the contingent

consideration arrangement as of the acquisition date (including

measurement-period adjustments), as well as the issuance of shares to settle

the contingent consideration arrangement on the date the contingency is

resolved, should be reflected as noncash investing and financing activities

and, in accordance with ASC 230-10-50-3, should be either disclosed

narratively or summarized in a schedule.

7.5.4.3 Unit-of-Account Considerations

Contingent consideration arrangements in a business

combination may contain multiple contingent payment triggers. With respect

to the statement of cash flows, neither ASC 230 nor ASC 805 provides

explicit guidance on the unit of account, including when multiple payments

are specified in a contingent consideration arrangement; that is, neither

contains authoritative guidance on whether such payment arrangements should

be viewed as a single unit of account or multiple units of account. This

determination could also affect whether the arrangement qualifies as equity

or a liability (in whole or in part) and, accordingly, the presentation in

the statement of cash flows (as discussed in Sections 7.5.4.1 and 7.5.4.2).

Given the lack of on-point guidance in ASC 230 and ASC 805, an entity may

need to use significant judgment in determining the unit of account. We

believe that for cash flow statement reporting, entities should use the same

unit-of-account determination as that used to determine the classification

of the contingent consideration arrangement as a liability or equity. This

determination is made on the basis of the following definition of a

freestanding financial instrument in the ASC master glossary:

A

financial instrument that meets either of the following conditions:

- It is entered into separately and apart from any of the entity’s other financial instruments or equity transactions.

- It is entered into in conjunction with some other transaction and is legally detachable and separately exercisable.

Note that in applying this definition to a contingent consideration

arrangement, an entity must use judgment and must consider both the form and

substance of the arrangement. The following matters may be relevant to consider:

-

Whether the counterparty to the arrangement has the ability to transfer its rights and, if so, whether these rights may be transferred in discrete denominations or the entire arrangement must be transferred in totality.

-

The interdependency of the risks and payment triggers — that is, whether there are shared or independent risks and triggers, which could include whether future triggers (and therefore payments of contingent consideration) may change prior payments in such a way that the acquirer can recover or “claw back” previous amounts paid.Connecting the DotsIn evaluating the interdependency of the risks and payment triggers, an entity should consider the duration of the measurement period for each contingent payment trigger to determine whether each measurement period represents a substantively discrete reporting period. Given the lack of other authoritative guidance defining what period would comprise a substantive discrete period, entities will need to carefully consider the relevant facts and circumstances. However, we believe that to have discrete periods, and therefore separate units of account, each discrete period needs to consist of a substantive period. For example, we believe that measurement periods of less than three months generally would not be substantive (on a basis consistent with interim reporting periods for an SEC registrant). Measurement periods of one year or more generally would be considered substantive. An entity must use judgment and consider the specific facts and circumstances in determining whether measurement periods between three months and one year are substantive.

-

Whether there is an economic need or a substantive business purpose for structuring payments of contingent consideration separately. Entities may find the guidance in ASC 815-10-15-8 and 15-9 useful in this evaluation.

Section

5.7.2.1 of Deloitte’s Roadmap Business Combinations provides

additional guidance on the unit of account for contingent consideration

arrangements and includes numerous examples. Because an entity may need to

use significant judgment in determining the unit of account when there is

more than one contingent payment trigger in a contingent consideration

arrangement, we encourage entities to consider consultation with their

accounting and financial advisers.

7.5.5 Acquired IPR&D Assets With No Alternative Future Use

In accordance with ASC 730, IPR&D assets acquired in an

asset acquisition rather than in a business combination should be expensed as of

the acquisition date unless such assets have an alternative future use, in which

case they should be capitalized. All IPR&D assets acquired in a business

combination should initially be capitalized regardless of whether they have an

alternative future use. For more information, see Chapter 4 of Deloitte’s

Life Sciences Industry Accounting Guide.

We have observed diversity in practice related to how cash

payments for IPR&D assets acquired in an asset acquisition are reported in

the statement of cash flows when such assets have no alternative future use.

While some entities classify the cash payments in operating activities, other

entities classify them in investing activities. Given the lack of authoritative

guidance on this matter and the diversity in practice, we believe that it is

acceptable for an entity to present cash payments related to the IPR&D

assets acquired in an asset acquisition that have no alternative use as either

operating or investing activities. This election is an accounting policy matter

that an entity should consistently apply to similar arrangements and disclose if

material.

Considerations related to the classification as operating or

investing activities include:

-

Operating activities — Classification in operating activities of cash outflows for IPR&D assets acquired in an asset acquisition that do not have an alternative future use is supported by the following:

-

ASC 230 does not specifically define such cash outflows as investing or financing activities.

-

Since such cash outflows are immediately expensed, they represent “the cash effects of transactions and other events that enter into the determination of net income” in a manner consistent with the definition of operating activities in the ASC master glossary.

-

-